Artificial intelligence is rapidly transforming the way banks, governments, and institutions manage financial systems.

AI is now being used to monitor transactions, evaluate risk, and even help determine who gets access to credit, loans, and essential services. While these tools promise speed and efficiency, they also raise critical questions about personal control and financial freedom.

That’s why we’ve created a new report designed to help you understand what’s changing, what’s coming next, and how to stay one step ahead.

[Click here to access the full report now]

Inside, you'll learn how emerging AI systems could affect:

-

Your access to traditional banking services

-

The way financial decisions are made—often without human input

-

What you can do now to stay resilient and protect your financial flexibility

These changes aren’t coming someday—they’re already underway.

Make sure you’re informed, prepared, and positioned to adapt.

[Get the report here: How AI Is Changing Finance]

Best regards,

The Wealthiest Investor Team

By following the link above or using any of the links provided below, you're choosing to opt in to receive insightful updates from The Wealthiest Investor plus 2 free bonus subscriptions! Your privacy is important to us. You can unsubscribe anytime. See our privacy policy for details.

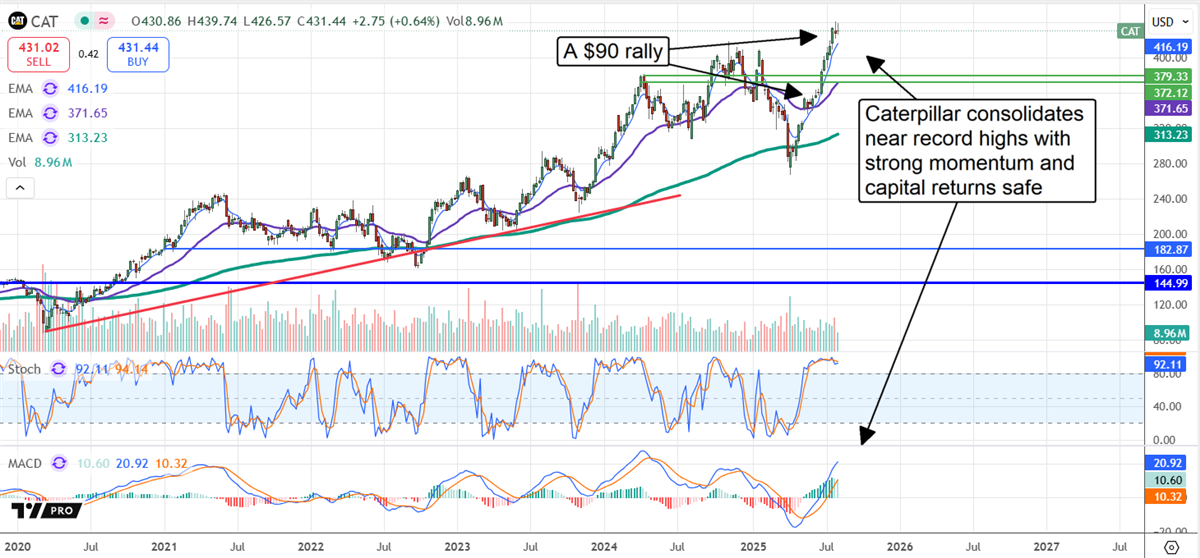

Caterpillar Can (and Will) Crawl Higher: Buy It on the Dip

Written by Thomas Hughes. Published 8/6/2025.

Key Points

- Caterpillar has headwinds in 2025 but is on the cusp of returning to growth.

- The capital return is safe, including the dividend, distribution growth, and aggressive stock buybacks.

- Analyst trends support this market and lead it to another 20% increase.

Caterpillar (NYSE: CAT) faces headwinds like any multinational business today, but its Q2 results highlight why its stock price can, and will, crawl higher over time. While macroeconomic headwinds, including lower realized prices, cut into revenue and earnings, the business is on the cusp of returning to growth, and its capital return is safe.

The capital return is critical for Caterpillar investors and includes dividends, distribution growth, and share buybacks.

The dividend alone is solid. The stock yields about 1.4% while trading near the early August highs, and it is a safe and reliable payment. Caterpillar is a Dividend Aristocrat with a payout ratio below 30%, a level suggesting sustainable annual increases can continue for years and may accelerate in size with growth back on the table.

The company is increasing at a moderate single-digit CAGR in 2025, more than sufficient to offset the impact of inflation. And the share buybacks are more substantial.

The buybacks are aggressive and expected to continue aggressively into the future. Buyback activity reduced the count by 3.6% year-over-year (YOY) on average for the quarter and will likely continue robustly because of the cash flow and balance sheet health.

The total capital return was less than 50% of cash flow in Q2, leaving the balance sheet in a healthy condition. Quarter-end highlights include a slight reduction in cash, an increase in liability, and a reduction in equity.

Still, they are offset by increased assets, low leverage, and the increase in treasury stock or reacquired shares. Treasury stock increased by more than 4x the reduction in equity.

Caterpillar Struggles With Headwinds: Guides for Growth

Caterpillar had a tough time in Q2 with realized pricing more than offsetting the increased volume. However, the increased volume sustains a healthy business and outlook that includes the resumption of revenue growth.

Until then, the $16.6 billion net revenue was down only 1% compared to the prior year, with significant sequential growth reported in all major segments. Segmentally, construction was the weakest with a 7.5% decline compared to last year, while Energy was the strongest at +7%.

Regionally, emerging markets were the strongest, growing by 6% year over year, while North America, Latin America, and Asia all posted low single-digit contractions.

The margin news is a sticking point for the market that could limit stock price gains in calendar Q3. The company reported a wider-than-expected decline in operating results due to tariff impacts and price realization, leaving the $4.72 adjusted EPS well below MarketBeat’s reported consensus.

However, as mentioned, the earnings and cash flow are sufficient to sustain the company’s financial health, growth outlook, and capital return, and the guidance is favorable. The company is forecasting revenue to be “slightly higher” than the previous year, which is an improvement from the prior guidance.

Analysts and Institutional Trends Provide Support for Caterpillar Stock

The analysts' trends suggest significant support for this industrial stock, including increased coverage, upgrades, and price target increases that lead to the high-end range. The net result is an increase in sentiment from last year’s Hold to this year’s Moderate Buy and an expectation for higher share prices.

The high-end range puts this market near $500 or another 20% increase from the early August trading levels.

The stock price action was mixed following the release, with selling offset by buying. The takeaway is that Caterpillar stock is consolidating near record highs and may extend its rally later this year.

In that scenario, it could easily level rise to the $500, potentially topping out near $520 sometime in 2026.

This email is a sponsored message sent on behalf of Darwin, a third-party advertiser of DividendStocks.com and MarketBeat.

If you have questions about your subscription, please don't hesitate to email our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

© 2006-2025 MarketBeat Media, LLC. All rights protected.

345 N Reid Pl. #620, Sioux Falls, S.D. 57103-7078. United States..

0 Response to "How AI Is Reshaping Banking—and What It Means for You"

Post a Comment