Ticker Reports for June 5th

Ollie's Bargain Outlet Stock Won't be a Bargain Much Longer

Shares of Ollie’s Bargain Outlet (NASDAQ: OLLI) are heading higher following the Q1 release and will likely continue rallying this year because of its market-leading growth. The company is a growing opportunity in off-price retail, outpacing the industry trend. The latest report includes outperformance, increased guidance, and an improved long-term target that suggests the rally may go on for years.

The stock is not cheap, trading at 25X this year’s guidance, but the valuation is warranted given the growth outlook. Analysts already forecasting significant growth in 2025 are now underestimating the business. The company announced the purchase of eleven new stores in Texas, further cementing its foothold in that market. Industry trends led management to increase the long-term store count target by 25%, lifting the long-term outlook for the stock price.

Among the takeaways from the report are the company’s growing influence. In the words of CEO John Swygert, the company has become meaningful to its vendor partners, improving the deal flow and opportunities, as seen in the margin.

Ollie’s Bargain Outlet is a Growing and Gaining Share

Ollie’s strong quarter is highlighted by a 3% comp store growth and an 8.4% increase in the store count. The 3% growth aligns with industry trends and is compounded by accelerated store count growth. The company reported $508.8 million in net revenue for a gain of 10.8% compared to last year, outpacing off-price leaders like The TJX Companies (NYSE: TJX) by more than 400 basis points.

The growth and improved market position led to a significant increase in margin. Gross margin widened 220 basis points on supply chain costs and merchandise margin and was compounded by improved SG&A. SG&A increased by 9.3% to lag the top-line growth as scale provided leverage and aided a 270 basis point improvement in generally accepted accounting principles (GAAP) and a 280 basis point improvement in the adjusted operating margin. The net result is a 50% increase in GAAP and adjusted earnings, with margin strength expected to continue in Q2 and the remainder of the year.

Guidance is moving the market. The company raised its guidance for the year to above the analysts' consensus and may be cautious. The addition of new stores, improving relevancy in the marketplace, and market share gains set it up to outperform

Ollie’s is a Cash Flow Machine

Ollie’s cash flow was negative in the quarter due to investments and financing activities, but that is the worst that can be said for this business. Operations over the last quarter increased the company’s cash position by 23% while keeping it debt-free and unencumbered. The total liabilities are less than 0.35X the assets and 0.5X the equity, leaving it in a nimble condition to continue investing in growth. As it is, the company is self-funding the latest acquisitions, which are expected to close by summer.

The analysts have yet to issue revisions based on the updated guidance but are unlikely to alter the trend. The revision trend has raised the sentiment to Moderate Buy from Hold since the Q4 2023 report was released, and the price target is up 40% in the last twelve months. The consensus assumes fair value near current levels, but the latest targets are leading the market to the high end of the analysts' range. A move to the high-end target of $104 is worth 20% to investors.

Ollie’s Bargain Outlet Advances and Confirms a Reversal

Ollie’s Bargain Outlet is up nearly 10% following the release and is likely to increase. The price action confirms support at a critical level and breaks to a new high to align with a market reversal. In this scenario, shares of Ollie’s could advance to $100 within a few weeks and exceed $110 by the end of the year.

Petrodollar Death Sentence?

The death of the "petrodollar" seems imminent.

And the implications could not be worse for Americans.

Russia, China and India have decided to abandon the petrodollar.

For one main reason.

CrowdStrike's Earnings: Consolidation and AI-Driven Growth

CrowdStrike Holdings, Inc. (NASDAQ: CRWD) is among the top players in the cybersecurity sector, a tech industry subsector. CrowdStrike’s earnings were released for the first quarter of fiscal year 2025, highlighting the company’s strategic focus on platform consolidation and AI-powered solutions. These strategic initiatives are driving significant growth and solidifying CrowdStrike's position as a dominant force in the evolving cybersecurity landscape.

CrowdStrike's Earnings Reflect Strong Business Momentum

CrowdStrike's Q1 2025 earnings report underscored the company's continued financial performance, demonstrating sustained growth across key operational and financial metrics. The company achieved total revenue of $921.0 million for the quarter, representing a 33% year-over-year increase. This robust revenue growth was driven by strong performance in subscription revenue, which climbed to $872.2 million, representing a 34% year-over-year increase. Professional services revenue also saw a notable rise, growing 18% year-over-year to $48.9 million. The geographic distribution of revenue reflected a consistent pattern, with approximately 68% of total revenue originating from the United States and the remaining 32% from international markets.

Further indicative of CrowdStrike's strong business momentum was the company's Annual Recurring Revenue (ARR) performance. Ending ARR for the quarter reached $3.65 billion, representing a 33% year-over-year increase. This growth was fueled by the addition of $212 million in net new ARR, signifying a 22% year-over-year increase.

CrowdStrike's commitment to profitability and operational efficiency was evident in its margin performance. Generally accepted accounting principles (GAAP) subscription gross margin remained at 78% for Q1 2025 and Q1 2024. Similarly, the gross margin of non-GAAP subscriptions held steady at 80% for both quarters. Total GAAP gross margin also remained at 76% for the same period. Total Non-GAAP gross margin followed suit, staying at 78% for Q1 2025 and Q1 2024. This consistent margin performance further highlights CrowdStrike's ability to manage costs effectively while driving growth.

Moreover, CrowdStrike achieved a non-GAAP operating margin of 22% in Q1 2025, exceeding the 17% achieved in Q1 2024. This improvement demonstrates the company's continued focus on operational leverage and profitability.

CrowdStrike’s financial performance translated into robust profitability. GAAP income from operations reached $6.9 million in Q1 2025, a significant improvement compared to the loss of $19.5 million experienced in Q1 2024. Non-GAAP income from operations also saw a marked increase, reaching $198.7 million, compared to $115.9 million in Q1 2024. GAAP net income attributable to CrowdStrike for the quarter climbed to $42.8 million, a substantial improvement from $0.5 million in Q1 2024. Non-GAAP net income attributable to CrowdStrike reached $231.7 million, a notable increase from $136.4 million in Q1 2024.

The company's earnings per share (EPS) also reflected this strong performance. GAAP net income per share attributable to CrowdStrike, diluted, was $0.17 for the quarter, compared to $0.00 in Q1 2024. Non-GAAP net income per share attributable to CrowdStrike, diluted, came in at $0.93 for the quarter, exceeding the $0.57 achieved in Q1 2024.

CrowdStrike's strong financial performance was further solidified by its robust cash flow generation. Net cash generated from operations reached $383.2 million in Q1 2025, exceeding the $300.9 million generated in Q1 2024. Free cash flow also experienced a significant year-over-year increase, reaching $322.5 million for the quarter, compared to $227.4 million in Q1 2024. As of April 30, 2024, CrowdStrike held $3.70 billion in cash and cash equivalents.

CrowdStrike's Platform Consolidation Strategy: A Foundation for Success

CrowdStrike's success hinges on its strategic focus on platform consolidation. The company's Falcon platform, a unified cybersecurity suite, addresses the industry's demand for comprehensive, cost-effective security solutions. Customers are increasingly choosing to consolidate their security needs on a single platform to streamline operations, enhance efficiency, and reduce the overall cost of security.

The Falcon platform delivers several tangible benefits for customers, including:

- Faster Detection and Response: Thanks to the platform's unified approach, customers report significantly reduced alert to resolution times, moving from days and hours to seconds and real-time.

- Extreme Cost Savings: The platform eliminates the need for multiple-point solutions, reducing operational complexity and delivering cost savings. CrowdStrike's customers have reported recognizing $6 of cost savings for every dollar invested in Falcon solutions.

The Falcon Flex subscription model further enhances CrowdStrike's platform consolidation strategy. This program allows customers to subscribe to the specific Falcon modules they need, providing flexibility and control over their security investments. Since its inception, Falcon Flex has proven successful, driving broader platform adoption and representing over $500 million in deal value.

CrowdStrike's partner ecosystem is also instrumental in the company's platform consolidation strategy. Strategic partnerships with Managed Security Service Providers (MSSPs) and other technology providers expand the platform's reach and facilitate seamless customer transitions. The company is witnessing a shift towards a more consolidated approach to security solutions, with partners prioritizing CrowdStrike on their product line cards.

Hypergrowth Solution Areas: Driving Innovation and Expansion

CrowdStrike's Q1 2025 earnings report highlighted the rapid growth of several key solution areas within the Falcon platform:

- Cloud Security: The demand for cloud security solutions is accelerating as organizations shift workloads to the cloud. CrowdStrike's Falcon Cloud Security Suite provides a comprehensive approach to cloud security, offering runtime-centric detection and response capabilities that safeguard cloud workloads and data.

- Identity Protection: CrowdStrike is a pioneer in the Identity Detection and Response (ITDR) category, offering a single-agent solution that provides comprehensive protection against identity-based attacks.

- LogScale Next-Gen SIEM: CrowdStrike is disrupting the traditional SIEM market with its AI-powered LogScale Next-Gen SIEM solution. This solution is natively integrated within the Falcon platform, leveraging the company's data gravity to deliver superior incident detection and response capabilities.

These hypergrowth solution areas demonstrate CrowdStrike's commitment to addressing the evolving needs of the cybersecurity market, driving substantial revenue growth and solidifying its market position.

CrowdStrike's strong Q1 2025 earnings and strategic approach to platform consolidation, innovation, and market expansion highlight its continued dominance in the cybersecurity industry. The company is strategically positioned to capitalize on the growing demand for AI-powered and cloud security solutions. At the same time, its commitment to innovation ensures its continued adaptation to the evolving threat landscape. CrowdStrike is well-positioned to remain a critical partner for organizations seeking to protect digital assets in an increasingly complex and interconnected world.

One trade. One ticker. One week.

Do you want to target weekly income of up to $2k or more…

Starting with just $500...

With just one trade per week?

3 Options Strategies to Protect Your Stocks in a Falling Market

While the stock market is near all-time highs again, not all stocks are experiencing the same bullish sentiment. You have probably noticed that a portion of your portfolio underperforming the benchmark indexes. Stocks that underperform when the market rises tend to sell off harder when the markets fall. Even the strongest stocks will eventually sell off either from profit-taking or a trend reversal. If you want to protect your stocks in a falling market, you can use stock options for that purpose. Here are 3 options strategies to protect your stocks in a falling market.

There’s (Almost) No Such Thing as a Perfect Hedge

You've probably heard that there's really no such thing as a perfect hedge. This is mostly true. The only way to perfectly hedge a stock position is to short-sell the position in another account. Even then, you're paying margin interest on the short position.

Our Guinea Pig Applied Micro Devices Stock

For each strategy, we’ll use a computer and technology sector stock, semiconductor giant Applied Micro Devices Inc. (NASDAQ: AMD), as an example.

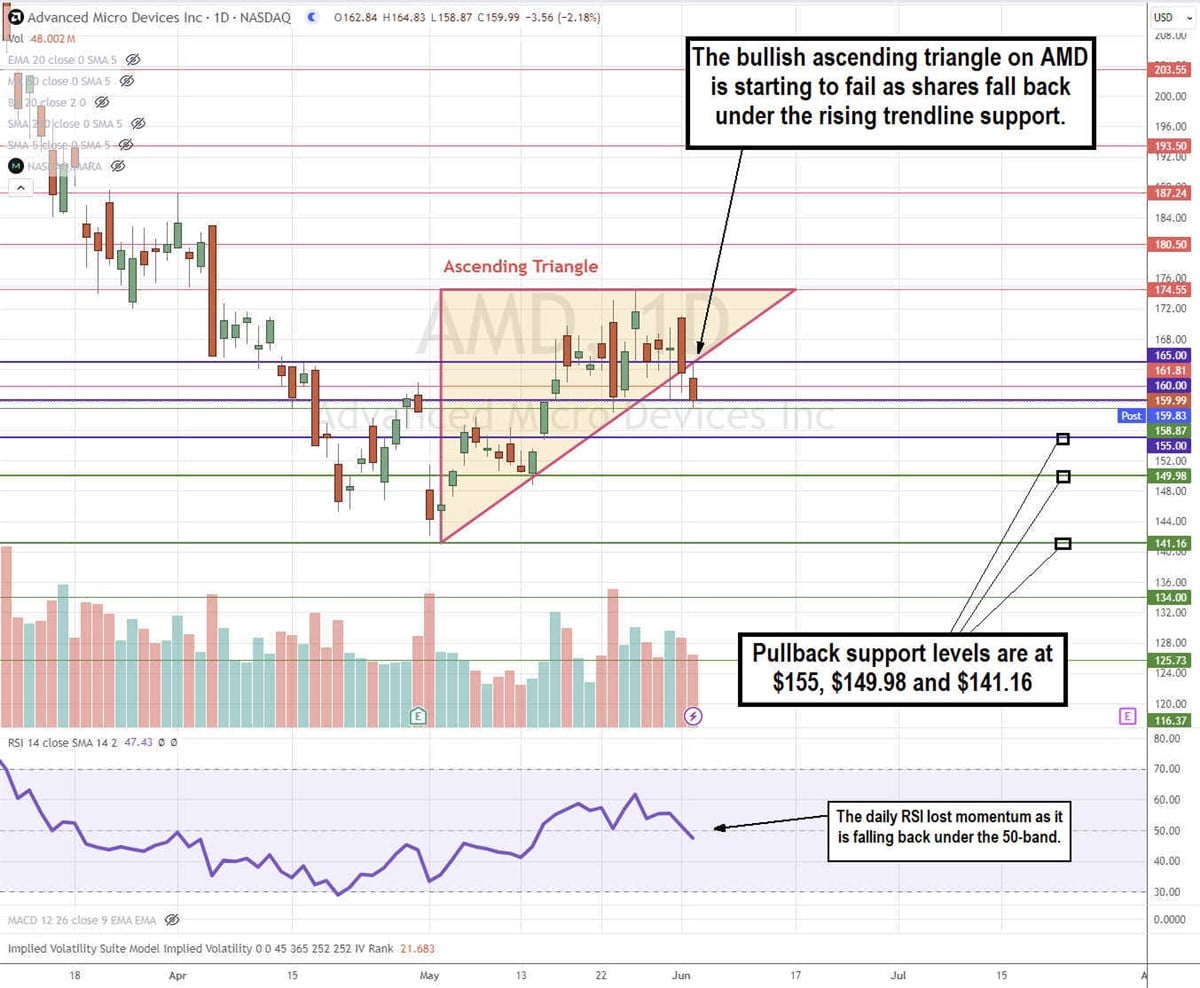

AMD is trading at $160 on June 4, 2024. The daily candlestick chart appeared to form a bullish ascending triangle but is starting to break down as shares fell under the ascending trendline. The daily relative strength index (RSI) has also turned down through the 50-band.

Let’s assume you own 100 shares of AMD stock long-term but want to protect yourself from a sell-off in the event that AMD breaks down. We'll use the July 3, 2024, expiration 31 days out.

Here are 3 options and strategies to consider.

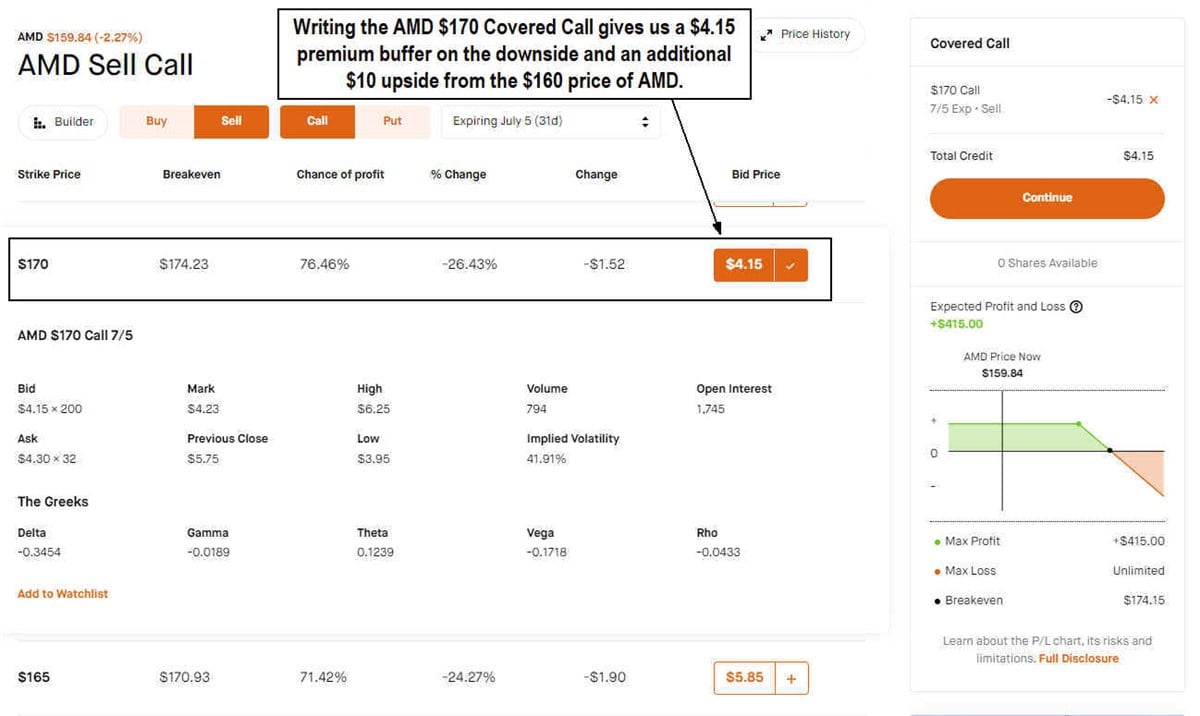

Strategy #1: Write a Covered Call

Writing a covered call is also referred to as selling a covered call. It's not selling a call but selling/writing a covered call, which means you already own the stock in the event it gets assigned. This strategy is similar to collecting rent on your stocks. A covered call strategy protects a portion of the downside since you collect a premium upfront. However, there is a risk of having to sell your position at the selected strike price if the underlying shares surge above it on expiration.

Let's select the 70-strike price. This would give us a $4.15 premium, which covers our downside on AMD to $155.85, which is just above the $155 support level. It also enables us to profit an additional $10 if AMD rises to $170 or higher by the July 5, 2024, expiration.

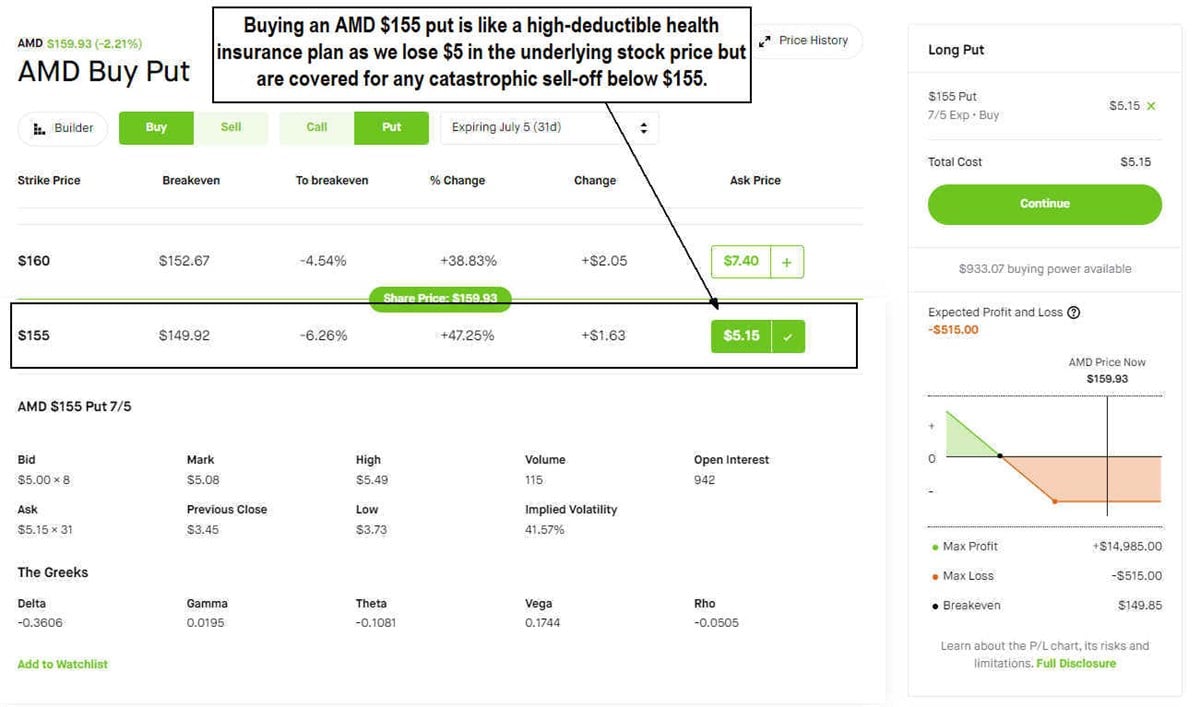

Strategy #2: Buy a Protective Put

If AMD could get into a serious breakdown, we can take on an insurance policy by buying a protective put. A long put will cost us money out of pocket, like an insurance policy. If AMD doesn't fall, then we lose that money. However, our upside isn't limited like a covered call in the case that AMD surges higher.

The put option rises in value as AMD falls under the strike price. We can select that strike price level since $155 is the next support. Since it's an out-of-the-money (OTM) option, our premium will be cheaper, as a $160 put would cost us $7.40. Remember, AMD is a long-term hold in the portfolio, so we want to get some protection in the near term.

We would buy the AMD for $155 Put for $5.15. This provides us protection if AMD falls below the $155 support level. Technically, AMD could fall to zero, and we would be protected from $155 down. AMD would need to fall to $149.55 for the put option to reach breakeven. We would still be down the $5 we are willing to stomach on the long-term hold. It's like a high-deductible health insurance plan where the $5 is the deductible, but we are covered for anything after that.

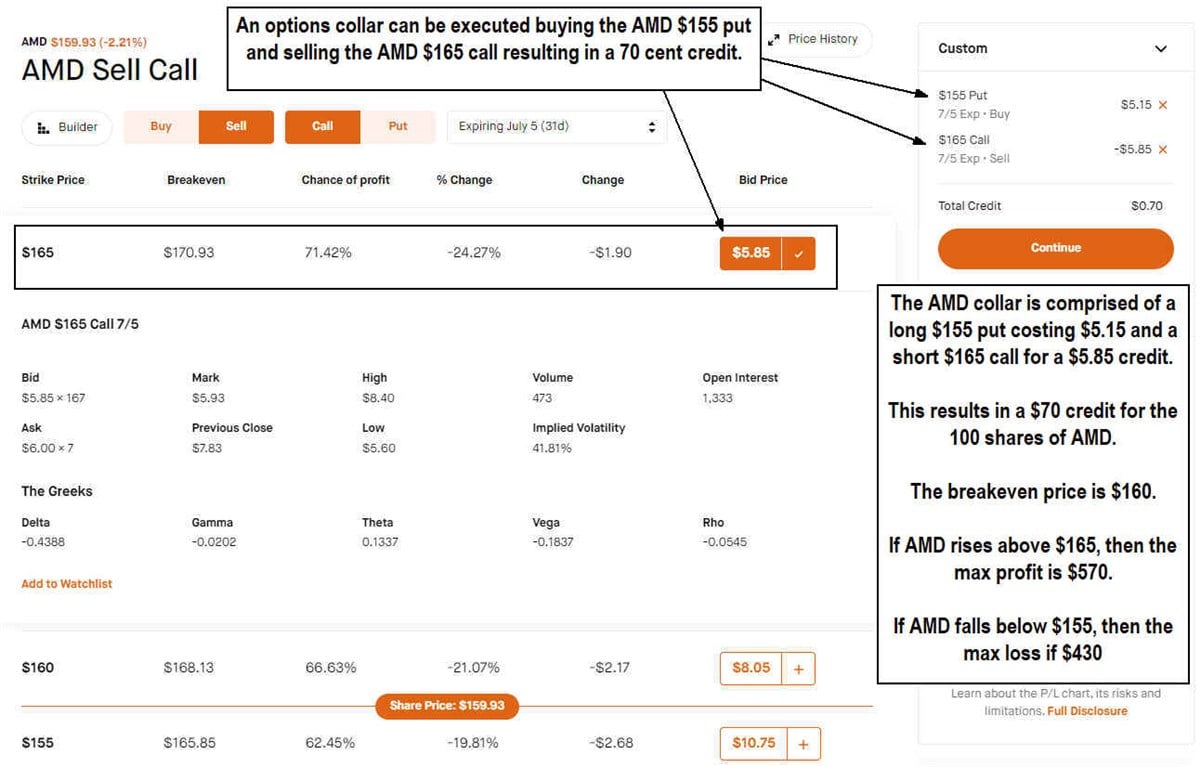

Strategy #3: Implement an Options Collar

An options collar is a way to lower the cost of the insurance. Rather than pay $5.15 for a $155 put, we can add one more leg (trade) by selling a higher strike call to collect a premium and lower the trade cost. The flip side is that we can get called out at $165, so we would have to sell the shares at $165 for a $5 upside in addition to whatever credit we may receive on the collar.

To execute a collar, we would buy the AMD $155 Put for $5.15 like we did for the protective put but also sell/short the AMD $165 call for $5.85. This results in a 70-cent credit, which is paid to us upfront. The cost of the trade is not only free but results in a $70 credit.

If AMD falls to $155 or below, then we are protected, and the max loss is $430, comprised of $500 minus the $70 credit. If AMD rises to $165 or higher, our max profit is $570, comprised of $500 plus the $70 credit.

Options Provide You with Options on Your Hedge

There is no perfect hedge; however, options can help buffer your downside. If you're holding stocks in a portfolio long or medium-term, these 3 strategies can help smoothen the ride when it gets bumpy. As with all options trades, holding the positions is not required until expiration. You can cut the cord anytime before expiration when you feel the coast is clear or if you don’t want to have your shares assigned. You can also roll your positions to extend the protection. We’ll go into those strategies in future articles.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Ollie’s Bargain Outlet Stock Won’t be a Bargain Much Longer"

Post a Comment