Ticker Reports for June 17th

Buffett Bails on BYD: What It Means for the Future of EV Stocks

Warren Buffett may not be that charged up about electric vehicles. On June 17, news broke that Buffett's Berkshire-Hathaway Inc. (NYSE: BRK.B) sold $1.3 million shares of BYD Company Limited (OTCMKTS: BYDDY). The move was reported in a filing with the Hong Kong Stock Exchange.

This was Berkshire's second sale of BYD stock in the last two years, and the company's stake in the company is now 6.9%. The hedge fund first bought the stock in 2008. At that time, it owned approximately 225 million company shares, valued at around $230 million.

The move has drawn attention since, in late 2023, BYD eclipsed Tesla Inc. (NASDAQ: TSLA) as the leading manufacturer of EVs in the world. However, BYD stock is down about 30% from its peak in 2022.

BYD vs. General Motors: Berkshire’s Investment Choices

Warren Buffett is known for being one of the leading advocates of buy-and-hold investing. The Oracle of Omaha has said his preferred length of time for owning a stock is forever. In fact, Buffett has said the investment advice that you never get broke taking a profit is foolish.

It's also important to put into context that Berkshire's 6.9% stake in BYD is nearly double its stake in one of its other prominent automotive stocks, General Motors Co. (NYSE: GM). And there's no indication that Buffett has increased his stake in GM.

That's not to say that Berkshire-Hathaway has never sold stock. But it's not a regular occurrence. And when it does happen, it's usually because Buffett sees better opportunities to deploy capital. That may be the case with electric vehicle stocks, which are under pressure on several fronts.

European Tariffs on Chinese EVs Begin

In response to China's ability to flood the global market with less-expensive EVs, the European Commission is going ahead with a plan to place a 38.1% tariff on imported Chinese EVs starting in July. For now, Chinese EV makers are saying it's business as usual, but there are concerns that this could start a more protracted trade war.

Buffett Reflects on Charlie Munger’s Influence on BYD Investment

Buffett noted in 2010 that his late partner, Charlie Munger, deserved all the credit for the investment in BYD stock. It's possible that Munger's passing, combined with all the noise around the EV industry, could have been a reason for the firm's recent decision to further trim its position in BYD.

At the hedge fund's annual meeting in May, Buffett alluded that the fund would continue to invest mainly in the United States. BYD is a notable exception, but it's possible that without Munger advocating for BYD, as Buffett notes he has done in the past, Buffett is taking a closer look at the company in light of the broader industry outlook.

How Significant is Buffett's Sale on the Future of EV Stocks?

As Buffett's decision to buy homebuilder stocks in 2023 showed, Buffett is known for looking ahead. That makes this decision more curious as it's more likely a case of Buffett reacting to what's already self-evident to investors.

Manufacturing EVs at scale is a capital-intensive business, and many EV companies not named Tesla are finding it hard to raise capital with interest rates significantly higher than when these companies went public. And even Tesla is finding that trying to pivot to meet changing consumer tastes is not fast nor cheap.

In short, many investors now believe the reward is no longer worth the risk that comes from EV stocks. It's not a leap to suggest that many of these start-up companies will go bankrupt. That's not likely to be the fate of BYD. However, as a Chinese company, investors must do more due diligence as its financials are more opaque to U.S. investors.

Prepare for a Recession Unlike Any Other

Dave Ramsey Is Dangerously Wrong And Here's Why>>

Asked whether we're on the cusp of a US Dollar crash, Dave Ramsey made a stunning miscalculation while live on air:

"Am I worried about this? Absolutely not."

Frankly, I've never seen someone so confident in being wrong…

Because what's happening to the US Dollar is not something you should "keep an eye on"…

But instead, is an imminent threat you should get ahead of right NOW.

Domino's vs. Papa John's: Stock Showdown of Pizza Giants

The pizza wars pit the 2 major pizza franchises against each other: Domino’s Pizza Inc. (NYSE: DPZ) versus Papa John’s International Inc. (NASDAQ: PZZA). While both brands operate in the retail/wholesale sector and have their fans and critics, one stock is clearly winning this war: Domino's.

Market Divergence: Domino's Surges While Papa John's Struggles

In fact, the trajectory between the 2 stocks couldn't be any more opposite. Domino's stock is trading up 26.5% year-to-date (YTD), while Papa John's is trading down nearly 39% YTD near 52-week lows when the S&P 500 index is trading near all-time highs.

With such a divergence, investors question whether it will continue and which stock presents a better investment opportunity moving forward. Let's examine each stock.

Domino’s: The World's Largest Pizza Company

Domino’s is the world's largest pizza company, operating in over 90 international markets serviced by over 20,500 restaurants. Over 95% of its stores are franchised, which makes Domino’s an asset-light operation. The company caters to budget-conscious consumers, offering numerous promotions, coupons, and a loyalty program accessible through its mobile app. The company is highly technology-oriented, with heavy investments in the mobile app, online ordering, and delivery tracking.

Domino's Q1 2024 EPS Beats Estimates

On April 24, 2024, Domino's reported Q1 2024 EPS of $3.58, beating analyst estimates by 18 cents. Revenues grew 5.9% YoY to $1.08 billion, matching consensus estimates. Global retail sales grew 7.3% YoY. U.S. same-store sales (SSS) grew 5.6% YoY. International sales rose 0.9%. Global net store growth was 164. Its recent partnership with Uber Technologies Inc. (NYSE: UBER) Uber Eats partnership will result in an extra 3% more sales through the channel.

Domino’s Reaffirms Strong 2024 Forecasts

Domino's expects 7% annual global retail sales growth and 8% annual income growth from operations. The company expects to grow its store count by over 1,100 in 2024. U.S. comps are expected to stay above 3% each quarter. Uber Eats sales are expected to increase throughout the year as marketing spend and awareness rise.

Domino’s CEO Russell Weiner commented, "The renowned value we created through our new and improved Domino's Rewards loyalty program drove outsized comp performance, which flowed through to the bottom line with double-digit profit growth. Importantly, our growth in the U.S. came through positive order counts in both our carryout and delivery businesses for the second quarter in a row. Further, this order growth was across all income cohorts.”

DPZ Stock Continues its Daily Ascending Channel

The daily candlestick chart on DPZ displays an ascending channel comprised of higher highs and higher lows. Shares are trading near the lower trendline as the daily RSI falls to the 55-band. Pullback support levels are at $500.82, $469.17, $440.37, and $416.36.

Domino's Pizza analyst ratings and price targets are on MarketBeat.

Papa John's: Navigating Recovery and Growth Challenges

Papa John's is the fourth-largest pizza operator in the nation. It is still recovering from the many controversies surrounding its founder, John Schnatter, ranging from racial slurs and political comments to sexual harassment allegations and the poison pill adopted by the Board of Directors to prevent Schnatter from ever regaining control of the company. Approximately 91% of its U.S. stores and around 41% of its international stores are franchised. Papa John's focuses on fresh and premium ingredients. The stock is trading near its 52-week lows.

Papa John's Revenues Continue to Fall in Q1 2024

Papa John's reported Q1 2024 EPS of 67 cents, beating analyst estimates by 10 cents. Revenues fell 2.5% YoY to $513.9 million, missing the consensus estimates of $544.46 million. North American comparable sales fell 2% YoY. Domestic company-owned restaurant sales fell 3% YoY. North American franchised restaurant sales fell by 2%. International comparable sales fell 3% YoY. The number of new units in North America rose by 8, and the company expects to open 100 to 140 new restaurants in 2024. Papa John's expects North American comps to remain flat to down low single digits in the full year 2024.

Papa John’s CEO Ravi Thanawala commented, “Our teams are taking a disciplined approach to running the business, improving restaurant-level margins, and increasing operating profits despite a challenging environment in the first quarter.”

Thanawala concluded, “More importantly, we’re making meaningful progress on our Back to Better 2.0 and International Transformation initiatives. The foundational improvements we are implementing in our restaurant operations, digital solutions, and marketing platforms are designed to drive sustainable, profitable growth around the globe.”

PZZA Stock is in a Descending Triangle Breakdown Pattern

The daily candlestick chart on PZZA illustrates a bearish descending triangle pattern. The descending triangle formed on the lower highs that formed following the $64.67 peak down to the flat-bottom lower trendline support at $46.68. The daily RSI is falling back to the 30-band, indicating a potential breakdown. Pullback support levels are at $46.22, $41.60, $38.29, and $31.50.

Papa John's analyst ratings and price targets are on MarketBeat.

The ONE AI Stock to own now. (It's not Nvidia.)

Don't panic — you haven't missed the boat on AI.

In fact, it has barely launched.

Sure, the early stages of this boom were big …

But I believe the real wealth in AI has yet to be made …

Williams-Sonoma Makes Stock More Accessible with a Stock Split

Upscale specialty retailer Williams-Sonoma Inc. (NYSE: WSM) has seen its stock price climb nearly 400% in the past 5 years. Like its expensive products, its share price has gotten out of reach for many investors. For this reason, the company announced a 2-for-1 stock split on June 13, 2024, to make its stock more accessible to investors and employees. The news initially caused shares to rise 3% on the day of the announcement, but the stock fell 6% the following day as it couldn’t seem to break out of its daily rectangle channel.

Williams-Sonoma operates in the consumer discretionary sector with upscale retailers like RH (NYSE: RH), formerly known as Restoration Hardware, Haverty Furniture Co. (NYSE: HVT), and Arhaus Inc. (NASDAQ: ARHS).

Williams-Sonoma Has a Portfolio of Upscale Store Brands

Williams-Sonoma is known for its namesake, upscale, and elegant kitchen and cookware stores, which are often found in shopping malls and strip centers. It also owns additional luxury brand stores specializing in different design and style preferences of furniture and housewares. Pottery Barn and Pottery Barn Kids provide furniture and bedding décor focusing on colorful and classic styles. West Elm offers upscale modern and contemporary furniture, rugs, bath and bedding. Rejuvenation offers vintage and industrial-style furnishings, light fixtures, décor, and hardware.

Catering to the Upper Middle Income and Affluent Consumers

Williams-Sonoma is known for its high-quality wares and exemplary customer service, fostering brand loyalty among affluent consumers. They offered curated collections, establishing their stores as premium destinations for families, with a significant portion of customers in the 45 to 65 age range with disposable income for discretionary home improvement spending. Its stores are located in major cities and affluent suburban communities, targeting higher household incomes. This demographic is often considered bulletproof and recession-resistant.

The company has been able to bolster margins and lower inventories thanks to its strong in-house design capabilities, robust first-party data that enables it to run more effective digital marketing campaigns and extraordinary customer service.

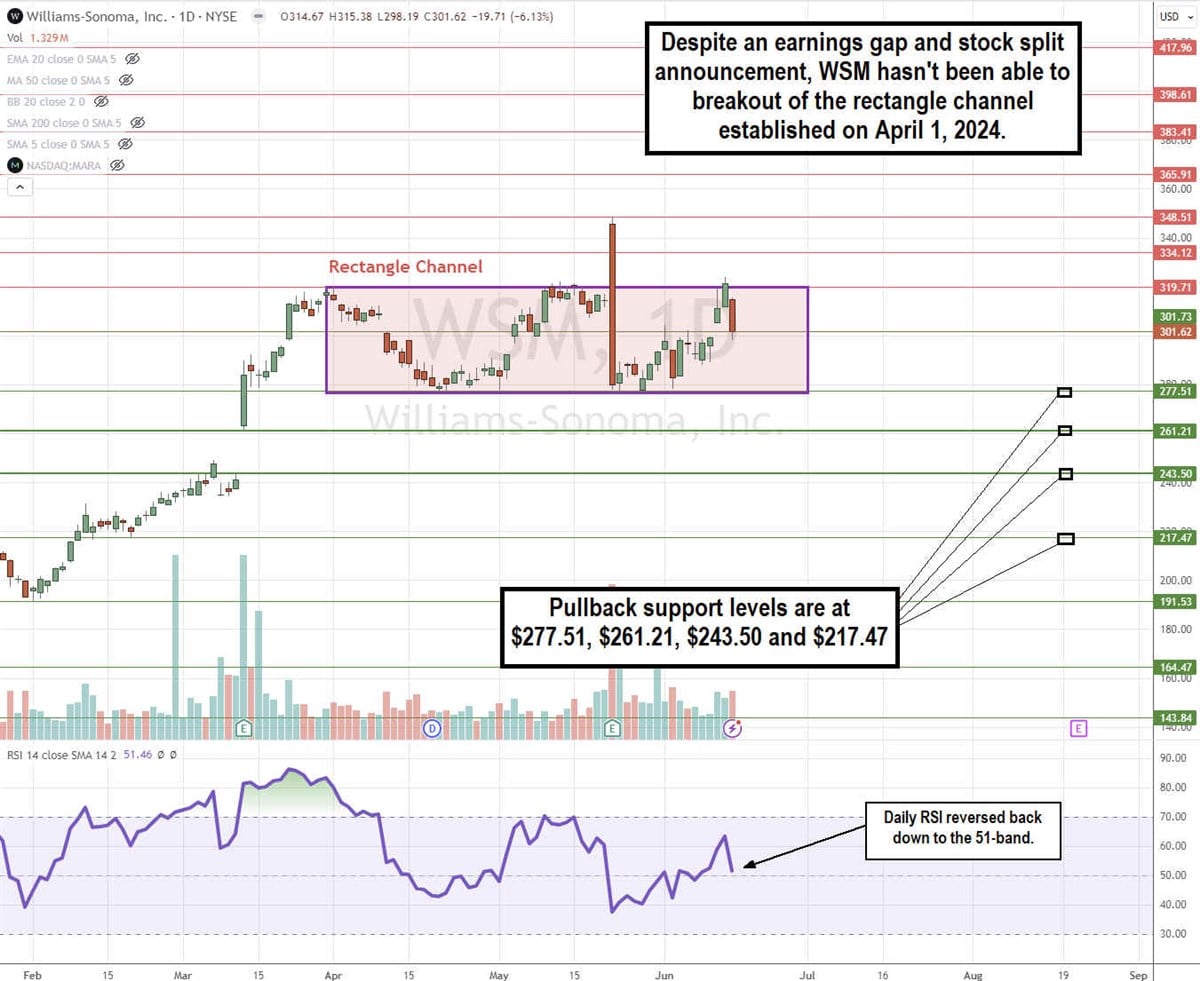

WSM Stock Continues to Trade in a Rectangle Channel

The daily candlestick chart for WSM illustrates the prevalence of its rectangle channel. The upper trendline resistance at $319.71 and lower trendline support at $277.51 have held their range since establishing themselves on April 1, 2024. Each breakout or breakdown attempt has been contained multiple times.

Most recently, the large earnings price gap to $349.51 on May 22, 2024, appeared to finally break out of the range, but WSM fell right back into the rectangle and even tested the lower trendline. The stock split announcement was another failed attempt at a breakout, which lasted a single day. The daily relative strength index has turned back down to the 51-band. Pullback support levels are at $277.51, $261.21, $243.50, and $217.51.

Blowout Q1 2024 Earnings But Revenue Softens

Williams-Sonoma reported EPS of $3.48 for Q1 2024, crushing the $2.74 consensus estimates by 74 cents. Revenue grew 5.4% YoY to $1.66 billion, which still beat the $1.65 billion consensus analyst estimates. Comparable (comp) brand revenue fell 4.9%, with a 2-year comp falling 10.9% and a 3-year comp down 1.4% YoY. Liquidity was strong, with $1.3 billion in cash and $227 million in operating cash flow.

Robust Kitchenware Sales Offset by Weak Furnishings

Williams-Sonoma continued to experience robust sales in its kitchen business, posting positive comps for 4 consecutive quarters, with its banner brand delivering 0.9% and 1.6% in Q1 2024 and Q4 2023. Unfortunately, furnishings continued its weakness driven by the slow housing market and sluggish consumer spending trends on large ticket items like furniture. This was reflected by the -10.8% comp in Q1 2024 and -9.6% comp in its previous Q4 2023 for Pottery Barn.

Solid Gross Margin Improvement Driven by 13.1% YoY Lower Merchandise Inventories

Gross margin rose 690 bps to 45.4%, driven by higher merchandise margins of 480 bps coupled with supply chain efficiencies of 240 bps, which were partially offset by 30 bps of occupancy deleveraging. The company's merchandise inventories fell 13.1% YoY. The company has also gained market share and remains committed to not running extensive promotional campaigns to protect margins further.

Without backing out 290 bps of out-of-period adjustment, the gross margin was 48.3%. The out-of-period adjustment was for a cumulative amount of $49 million attributed to over-recognized freight expenses in fiscal 2021, 2022, and 2023.

The Company Reiterated 2024 Guidance, Market Was Not Impressed

Williams-Sonoma reiterated its 2024 outlook of -3% to +3% annual net revenue growth, or $7.52 billion to $7.98 billion versus $7.72 billion, and comps in the range of -4.5% to +1.5%. Operating margin guidance was raised from 17.6% to 18%, which includes the 60 bps out-of-period adjustment. The company expects an operating margin between 17% and 17.4% after the adjustment. The company expects mid-to-high single-digit yearly net revenue growth with a mid-to-high teen operating margin.

The market gapped and sold off WSM shares, not only giving back its gains but losing nearly 11% on the day as it expected the company to raise rather than reaffirm its guidance.

Williams-Sonoma analyst ratings and price targets are at MarketBeat.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Williams-Sonoma Makes Stock More Accessible with a Stock Split"

Post a Comment