Ticker Reports for November 11th

Monday.com's Manic Price Pullback Is a Signal to Buy

Monday.com’s (NASDAQ: MNDY) guidance is tepid relative to the consensus outlook, but no reason to sell the stock and certainly no reason for the market to drop 10%. As tepid as the guidance may be, it is still a strong guide for the business, and it is likely to be cautious, given the trends. Some takeaways from the Q3 report are outperformance, scaling, expansion, and deepening penetration of clients - takeaways that add up to strengthening business leverage for the leading work management platform. The stock price pulled back following the release but will likely not stay down long.

Monday.com Builds Leverage With Workplace Automation

Monday.com’s Q3 results are good. The company grew revenue to $251 million, up 32.7% compared to last year, beating the consensus estimate by 190 basis points. The strength was driven by deepening penetration and a growing client count that shows Monday.com growing alongside the businesses it serves while capturing new, larger clients.

The number of clients contributing more than $50K and $100K in annual recurring revenue increased by more than 40%, putting total ARR above $1 billion. The net retention rate or revenue from existing customers as a percentage of last year’s contribution is 111%, accelerating from the previous month as the rate of penetration increases.

Margin news is also good. The company’s adjusted operating margin held steady at 13%, driving a 30% increase in net cash from operations and a 26% increase in free cash flow. The free cash flow is a significant driver for this investment, as the margin ran at 32% for the quarter and is expected to sustain a 30% pace for the full year. The cash flow allows the company to reinvest to expand offerings and scale operations while maintaining a fortress balance sheet. The balance sheet highlights include a cash build and increased assets that more than offset the increased liability. The net result is a 20% increase in equity, with most assets in cash. Total leverage is less than 0.5x cash and less than 1x equity.

Monday.com Guides for Sustained Growth and Robust Cash Flow

Monday.com’s guidance is mixed. The full-year targets are better than the consensus reported by MarketBeat.com ahead of the release due to the Q3 strengths, but Q4 will be tepid, only aligning with the forecasts quarterly. The risk is that growth is slowing to below 30%, but the 28% forecasted by the company is still solid and likely to be cautious. Regardless, analysts are unlikely to alter their positions because of the guide, and they support the market.

The analysts' trends in 2024 include increased coverage and a growing conviction that the stock is undervalued. The number of analysts covering the stock increased by nearly 50% to 15, while the consensus price target trended higher. The consensus target puts the market near $306, but the most recent revisions run in the $320 to $340 range, a gain of 15% to 20% from support targets near $280.

Institutions also support the stock and are likely to buy with the price at a discount. They have bought the stock on balance for 3 consecutive quarters, aligning with the market bottom in early 2024 and the updraft since summer.

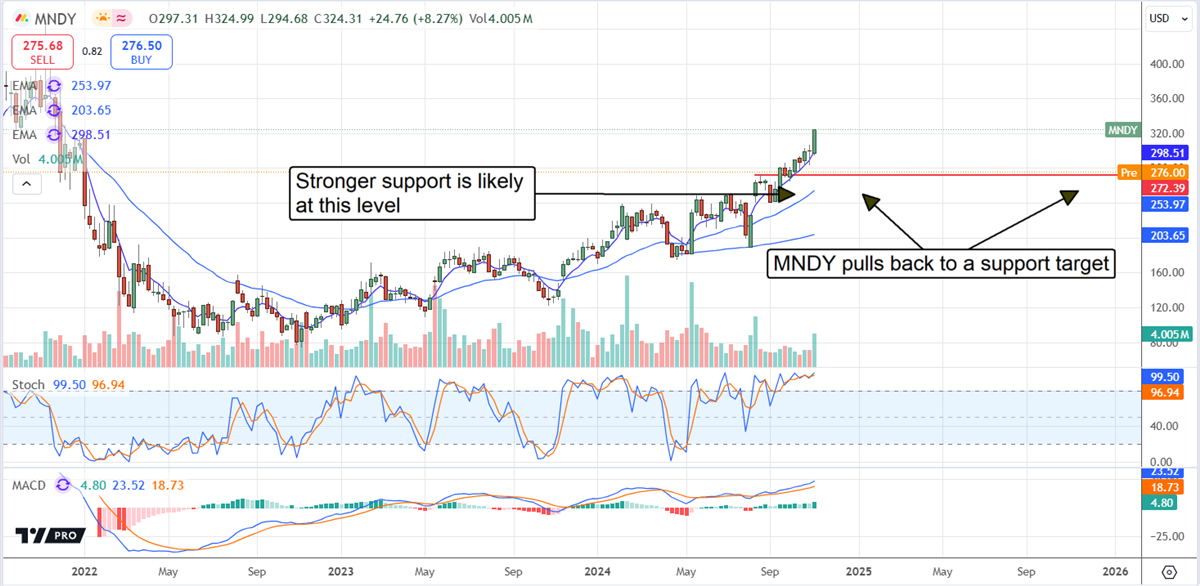

Monday.com Price Pulls Back: Wait for the Market to Signal

Monday.com's price pulled back to a potential buying point, but the market hasn’t confirmed the bottom in the pullback yet. While a rebound is expected, the market may move as low as $250 before it begins. The $275 level is a possible support target but weak compared to the firmer support provided by the 150-day EMA. A move below that level would be bad for the market and could lead to an even larger decline. Assuming the market confirms support near $250 or higher, new highs are likely before mid-year 2025.

Bill Gates's Next Big AI Bet: Stargate

In February 2016… when almost nobody was talking about artificial intelligence….

I picked Nvidia as one of my favorite stocks.

Shares have jumped by more than 20,000% since then.

3 "Made in America" Stocks to Benefit From the Trump Presidency

The return of the Trump administration to the White House in 2025 has caused many U.S. stocks to surge pre-emptively on positive sentiment, while Chinese stocks collapsed on fears of more trade tensions and tariffs to come. During his reelection campaign, Trump suggested imposing a 60% tariff on goods produced in China and 20% on everything else. Trump even threatened farming machinery giant Deere & Co. (NYSE: DE) with 200% tariffs on anything they produce in Mexico to force them to keep its production in the U.S.

As the markets try to anticipate his actions based on his previous administration’s policies, stocks that fit certain themes are already seeing the early money flow. The core theme of the Trump administration has been and will continue to be "Made in America," which focuses on bolstering U.S. manufacturing and creating jobs. Here are three stocks spread across the auto/tires/trucks, computer and technology, and basic materials sectors that are already benefiting from the Trump presidency.

General Motors: Automobiles Made in the U.S.A. and Protected By Tariffs

The country's largest car manufacturer, General Motors Inc. (NYSE: GM), saw its stock surge 7% to 52-week highs after a Trump victory was called. Trump has had a firm stance on protecting U.S. automakers from foreign competition, especially cheaper foreign-made vehicles from China, which already face a 100% tariff on electric vehicle (EV) exports.

Import tariffs on vehicles and auto parts end up making non-American vehicles more expensive for consumers, creating a more favorable market for General Motors's products and its top four American brands: Chevrolet, Buick, GMC, and Cadillac.

General Motors is outperforming U.S. competitors like Ford Motor Co. (NYSE: F), who are just starting to regain some footing after finally beating its Q3 EPS estimates by 2 cents. General Motors crushed its latest third quarter of 2024, reporting EPS of $2.96, beating analyst estimates by 58 cents. This marks the third consecutive quarter of 35 cents+ EPS beats. Revenues grew 10.5% YoY to $48.76 billion, crushing analyst estimates for $44.67 billion by an eye-watering $4.09 billion.

General Motors raised the lower end of its full-year 2025 EPS estimates to a range of $10.00 to $10.50, up from $9.50 to $10.50 versus $9.97 consensus estimates. Automotive free cash flow was raised to the $12.5 billion to $13.5 billion range, up from $9.5 billion to $11.5 billion.

Intel: Semiconductors Made in the U.S.A. Supported by the CHIPS Act

American semiconductor giant Intel Co. (NASDAQ: INTC) has been suffering for several years now as competitors like NVIDIA Co. (NASDAQ: NVDA) dominate the artificial intelligence (AI) chip market. While major chip makers like NVIDIA, American Micro Devices Inc. (NASDAQ: AMD), Marvell Technology Inc. (NASDAQ: MRVL) and Broadcom Inc. (NASDAQ: AVGO) outsource their chip production overseas to Taiwan Semiconductor Manufacturing Co. (NYSE: TSM), Intel continues to produce them in their domestic fabrication (fabs) foundries.

The CHIPS and Science Act of 2022 seeks to bolster the domestic semiconductor supply chain to reduce reliance on foreign suppliers for national security and economic competitiveness. It includes $52 billion in subsidies and incentives for chip makers to build and expand fabs in the U.S.

Intel was awarded up to an additional $3 billion under the CHIPS Act to construct four foundries in the United States. This was in addition to the $8.5 billion awarded in March of 2024.

Payments are expected to start at the end of the year. Intel needs all the help it can get as it continues to struggle. The company lost 46 cents per share in its third quarter of 2024. Revenues continued to contract as they fell 6.3% YoY to $13.3 billion. Gross margin fell 27.8 points to 18%. The company is undergoing a $10 billion cost reduction plan, which includes reducing headcount by over 15% of its workforce or 15,000 jobs. However, the company did provide some upside guidance for Q4 as it expects a positive EPS of 12 cents versus 8 cents, consensus estimates, and a non-GAAP gross margin improvement of 39.5%. Shareholders are looking forward to the spin-off of its foundry business in 2025.

Nucor: Galvanizing the American-Made Steel Supply Chain

As one of the largest domestic steel producers, Nucor Co. (NYSE: NUE) was a major benefactor of Trump’s previous administration policies. The imposition of 25% tariffs on imported steel was a boon to the company as it made foreign steel more expensive, reducing competition.

Critics argue that this enabled U.S. steel manufacturers to bump their prices without competition. This fanned the flames of inflation, driving up higher prices for the U.S. consumer, from construction to appliances and vehicles. While major trading partners like Mexico were able to gain exemptions, their status may face more scrutiny with the new Trump administration.

Nucor is also a direct beneficiary of domestic infrastructure spending, which has bipartisan support for rebuilding America’s infrastructure. Bridges, highways, and construction projects all bolster the demand for steel. Not all domestic steelmakers will benefit from Trump's return to the White House. The proposed acquisition of United States Steel Co. (NYSE: X) by Japan’s Nippon Steel Co. would almost certainly be blocked by Trump. Trump wants to ensure a 100% American supply chain for all essential goods.

917 Trades… Zero Losses?

If you want to learn how A Group of traders Made 917 Trades Without A Single Loss! And How You Could Have Consistently Beat the Market by following them...

Just click this link and follow along

DuPont Is the Unexpected Benefactor of the AI Boom

The name DuPont is often associated with specialty chemical and materials products. DuPont pioneered the creation of cellophane in the 1920s and Teflon, Neoprene and nylon in the 1930s. Through the years, the company continued to develop and evolve many familiar chemicals, including freon, polyethylene, silicone, plastics and genetically modified organisms (GMOs) in the 1980s.

Evolution From Chemicals to Technology Materials

In 2015, Dupont merged with Dow Chemical to form DowDuPont, the largest chemical conglomerate in the world. In 2019, DowDuPont split into three public companies. Dow Inc. (NYSE: DOW) focuses on materials sciences for packaging, infrastructure, and consumer care. Corteva Inc. (NYSE: CTVA) operates in agriculture, focusing on seeds and crop protection. DuPont de Nemours Inc. (NYSE: DD), also referred to as simply DuPont focuses on technology-based materials and solutions. DuPont provides materials essential to semiconductor fabrication, solar panels, LEDs, and electric vehicles (EVs) encompassing the computer and technology, aerospace, auto/tires/trucks, and industrial sectors.

DuPont’s Role in the Semiconductor Industry

Some of the key materials that DuPont manufactures for the semiconductor industry include photomasks, which are the light-sensitive materials used in photolithography to transfer circuit patterns onto silicon wafers, dielectrics, conductive materials for interconnects on chips and chemical mechanical planarization (CMP) slurries used for polishing silicon wafers for a smooth and flat surface. Their materials are crucial for semiconductor manufacturing equipment (SME) makers like Lam Research Co. (NASDAQ: LRCX) and ASML Holding N.V. (NASDAQ: ASML).

The AI Boom Directly Benefits DuPont Materials in the Chip Industry

DuPont also supplies the materials necessary for advanced packaging, including encapsulation materials to protect semiconductor devices and thermal interface materials for heat dissipation. The artificial intelligence revolution, which has led to the surge in GPUs, NAND flash, high-bandwidth memory (HBM), and application-specific integrated circuits (ASICs), has a direct impact on DuPont's business.

Over 35% of its total revenue comes from its Electronics segment, which includes semiconductor solutions and advanced electronic products. This is where the connection between AI and DuPont makes a material impact on its business. The AI boom enabled DuPont to post a second consecutive quarter of revenue growth after 10 straight quarters of YoY revenue decline.

The AI Boom Helps Drive DuPont’s Q3 Earnings Beat

DuPont's growth engine is driven by its Electronics and Industrial segment. While organic sales rose 10% YoY, its Semiconductor Technologies segment saw a 20% YoY jump in revenues. This segment produces the materials used during the semiconductor fabrication, assembly, and advanced packaging process. The 20% growth was a result of rising demand for AI technologies, recovery in consumer electronics, and rebounding demand in China. DuPont posted stronger operating leverage with a 150 bps improvement in operating EBITDA margin to 26.8%, which led to a 15-cent EPS beat over consensus estimates. DuPont also raised its full-year 2024 revenue guidance up to $12.50 billion from a previously forecast range of $12.365 billion to $12.40 billion versus $12.44 billion consensus estimates.

DuPont CEO Lori Koch expressed plainly in the conference call, “From an end market view, the electronic and industrial segment saw another quarter of double-digit sales growth in both the semi and interconnect solutions lines of business, which continued to benefit from strong demand for advanced node chips and AI-enabling technologies.”

Splitting Again Into 3 Companies

History will repeat itself as DuPont plans to split into three separate companies once again: New DuPont, Electronics, and Water. The New Dupont will focus on automotive, healthcare, and safety and protection products. The Electronics and Water divisions will be divided into separate public companies in a tax-free separation in 2025.

DD Triggers a Descending Ascending Triangle Breakout

A descending triangle is normally a bearish chart pattern indicator of lower highs on the bounce against flat-bottom support. At the apex point, the descending upper trendline converges with the flat-bottom horizontal lower trendline support. A breakdown triggers if the stock falls below the lower trendline support. A breakout triggers if the stock surges above the upper trendline resistance.

DD formed the descending trendline at the $90.06 swing high as it capped all bounce attempts at lower lows to converge with the flat-bottom support trendline at $81.35. The daily anchored VWAP sits at $85.08 still acting as a resistance. The daily RSI is slipping to the 49-band. Fibonacci (Fib) pullback support levels are at $83.67, $81.35, $77.27, and $75.14.

DD’s average consensus price target is $95.42 implying a 13% upside, and its highest analyst price target sits at $107.00. It has nine analysts' Buy ratings, two Holds, and two Sell ratings. The stock has a 1.81% annual dividend yield.

Actionable Options Strategies: Bullish options investors can enter DD on a pullback using cash-secured puts at the Fib pullback support levels or take a bullish call debit spread for an uptrend continuation using less capital than owning the stock while minimizing the downside for capped upside gains.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 3 "Made in America" Stocks to Benefit From the Trump Presidency"

Post a Comment