Ticker Reports for November 12th

Home Depot Stock: Targeting 12% in 2024 and 25% More in 2025

Home Depot (NYSE: HD) is moving higher on the combined forces of outperformance and an expectation for tailwinds to develop in 2025. Better-than-expected consumer trends, acquisitions, and the pro-business drive outperformance in 2024, leading the company to improve guidance against a backdrop of negative sentiment. Tailwinds will form in 2025 as policy headwinds ease and Trump’s business and consumer-friendly policies spur activity, specifically in the housing market.

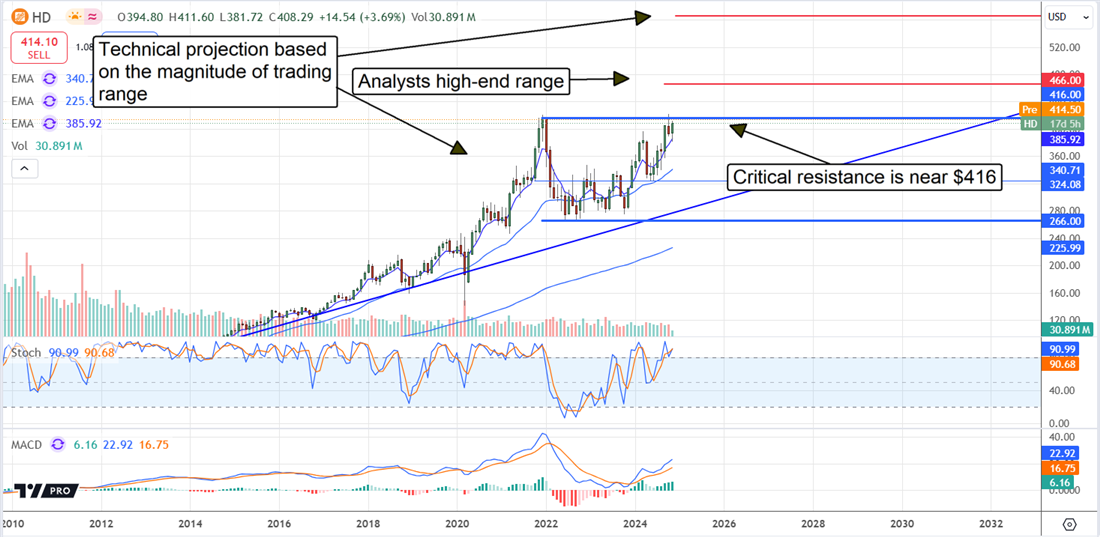

The forecast for interest rate cuts has eased from its peaks set a few months ago but remains favorable, with the base rate expected to fall another 50 basis points or more by the end of the year. The takeaway for investors is that Home Depot outperforms and builds leverage through acquisitions ahead of an expected shift in economic fundamentals. It raised guidance for 2024, and the forecasts for 2025 are likely cautious because of tailwinds expected to develop. That means the stock is positioned for the analysts' upgrade cycle to continue, and with the stock already near record highs, a new high is likely. The technical indications suggest an additional 12% advance once the critical resistance is broken, and a larger 35% gain is possible over the next four quarters.

Home Depot Grows With Acquisition of SRS

Home Depot struggled in Q3, with comp sales declining, but the weakness was far less than anticipated. All the analysts tracked by MarketBeat had lowered their estimates during the quarter, setting the bar very low. The company’s $40.2 billion net revenue is up 6.6% primarily because of the acquisition of SRS, which is expected to add about $10 billion in annualized revenue, worth about 6% of the 2025 consensus estimate. Comps are down 1.3% across the network and 1.2% in the core U.S. market.

Margin news is also favorable, with margin contraction being less than expected. Acquisition and growth-related impairments impacted the company’s cash flow and margin, but the 70 basis point decline allowed for leveraged performance on the bottom line. The company’s $3.78 in adjusted EPS fell $0.07 compared to last year or 180 basis points, outpacing the consensus by 350 bps and the top-line strength by 100. The salient point is that an adjusted operating margin of 13.8% allowed for income growth despite the contraction, helping to sustain the company’s robust financial outlook.

Guidance was raised, helping to lift market sentiment. The company raised its full-year revenue guidance to up 4%, including the addition of SRS and the extra 53rd week, nearly 100 basis points above the consensus estimate. Earnings guidance is also favorable, with operating margin expected to hold steady sequentially and adjusted earnings expected to fall only 1% for the year.

Home Depot Builds Value With SRS Acquisition

The worst that can be said about the SRS acquisition is that it increased the company’s debt and leverage, but the impact will be short-lived. The company is a solid cash-flow producing machine and can tackle the debt, running at 10X equity in late 2024. The offsetting factor is the positive impacts of the acquisition on the balance sheet, which include increased current and total assets, with total assets up nearly 28% and lagged by a 23% increase in liability.

Shareholder equity is up 300% and will likely grow as debt is reduced. Regardless, the cash flow outlook and balance sheet are sufficient to sustain the capital return program, including the dividends and buybacks. The dividend is worth $9.00 and yields more than 2.10%, with shares near record highs and the distribution is expected to grow in 2025. Buybacks reduced the share count by 0.5% at the end of the quarter and are also expected to continue in 2025.

Home Depot Tracking for New Highs

The trend in analysts' sentiment ahead of the release is unlikely to end now that guidance for Q4 is in. The trend includes improving sentiment and price expectations with fresh coverage entering the picture, sentiment firming, and the price target increasing. The consensus target is near $466 and is up 25% over the last year, 500 basis points in the month leading into the release. The consensus implies fair value near the all-time high, but the revision trends suggest a move to the high-end range near $466 is likely. A move to $466 could happen quickly once the all-time high is surpassed.

Buy these "two-bagger" stocks

We've put together something special for our subscribers — a free report on 5 stocks we believe could double in 2024. It's straightforward, easy to understand, and most importantly, actionable.

Download your free report today!

Is Tesla's Valuation a Bubble or Backed by Real Growth?

Once the United States presidential elections were over, there seemed to be an everything rally for the financial markets, or, as Warren Buffett likes to say, a rising tide lifts all boats. However, he also likes to add that when the tide goes out, that’s when everyone knows who’s been swimming fully clothed or not. Today, some call for shares of Tesla Inc. (NASDAQ: TSLA) to be in the latter group, considering its valuation today.

These bears would be wrong, though. Sure, the stock trades at a high price-to-earnings (P/E) ratio of up to 95.1x today, which is exorbitantly higher than the auto sector’s average valuation of only 18x. Investors would fail to realize, however, that Tesla is not just any other automotive stock. Therefore, it shouldn’t trade like one. Tesla behaves more like a technology stock and an artificial intelligence one for a reason.

That’s because Tesla is one. Wall Streeters fail to realize that Tesla owns all the software behind the industry's self-driving breakthroughs, not to mention additional ownership in other tech ventures like social and generative artificial intelligence through OpenAI and X (formerly Twitter), both businesses that aren’t reflected in Tesla’s current valuation.

Breaking Down Tesla’s Valuation: Why Bulls Are Holding Strong

Now that the “It’s just a car company” argument is somewhat out of the way, here’s what investors should focus on. Tesla’s market capitalization is $1.1 trillion today, which by all measures would be an exaggeration were Tesla only a car manufacturer. Now that investors know this isn’t the case, here’s how Tesla pares against others in AI and technology.

Semiconductor and artificial intelligence supporter Nvidia Co. (NASDAQ: NVDA) has reached a valuation high of $3.6 trillion, representing over 15% of the United States Gross Domestic Product (GDP). Then there is Alphabet Inc. (NASDAQ: GOOGL) and Meta Platforms Inc. (NASDAQ: META), who trade at valuations of $2.2 and $1.4 trillion, respectively.

Putting it this way, Tesla’s valuation today wouldn’t seem that far from the norm. Of course, in order to lean on this view, investors have to wholeheartedly believe that Tesla is far more than just a car company. Now, here’s an interesting point of view on social platform X.

Elon Musk, Tesla’s CEO, took the company private in 2022. While today it is reportedly worth 80% less than what he paid for it, Musk saw fit to allocate up to $44 billion to buy out the company formerly known as Twitter. Why would Musk pay such a high ticket for this platform, and what are his plans?

This might be on the more speculative side. Still, there are trends suggesting that Musk wants to turn X into a super application, exactly the way China has done with Tencent Holdings Ltd. (OTCMKTS: TCEHY) and Alibaba Group (NYSE: BABA), which operate the WeChat and Alipay platforms in the nation, respectively.

Looking at Musk’s resume, as the founder of payments platform PayPal Holdings Inc. (NASDAQ: PYPL), it wouldn’t be too far-fetched to see his former expertise turn X into a similar platform to the ones already discussed.

Then there’s the OpenAI aspect, the creators of ChatGPT who are also owned and backed by Musk. Three tailwinds—electric vehicles, artificial intelligence, and decentralization—are behind Tesla's stock price today.

Here’s What Wall Street Sees: Aligning Reality and Investor Expectations

While trying to value Tesla under all these assumptions will be beyond Wall Street analysts' reach, a few were willing to put their necks—and reputations—on the line to give Main Street a broader look into Tesla stock's future.

Wedbush recently reiterated its "Overweight" target on Tesla while also boosting its price targets to a high of $400 a share, up from its previous view of $300. This new valuation would call for a net upside of as much as 14.3% from where it trades today.

Despite a 48% rally in the past month alone, there are plenty of reasons to justify the possibility of Tesla giving investors another such run shortly, especially as more participants realize that the company has all of the already mentioned tailwinds working in its favor.

These analysts are not alone in their high expectations for Tesla stock. As of November 2024, institutional buyers from Jennison Associates decided to boost their Tesla holdings by as much as 11.9%, bringing their net position to a high of $3.2 billion today.

All told, investors now must see Tesla for what it really is: a stock that trades at a massive premium to its peers; however, there are reasons to believe that the peer group needs to be correctly selected. More than that, any stock that trades at higher valuations for prolonged periods of time usually has a good reason to do so, and Tesla checks all the boxes.

BITCOIN

Did you miss out on the 1000%+ gains of Bitcoin over the past 5 years?

If so, you don't want to miss this...

Trucking Stocks Led the Pack Last Week: Can They Keep Rolling?

Price action can be one of the best indicators for investors to keep track of when figuring out where the market is trying to go in the coming quarters. As it turns out, most – if not all – asset classes rose tremendously the morning after the United States presidential elections, and as Warren Buffett says, all boats will do well on a rising tide.

Buffett also likes to say that when the tide goes out, investors will know who was swimming fully clothed or not. As it relates to price action, this concept is the key to figuring out what might be headed for the U.S. economy in the coming quarters. All roads lead to a single common trend. By spotting and riding with it, investors have a better-than-average chance of beating the market.

The trend has been spotted in transportation stocks, particularly those involved in trucking. Shares of SAIA Inc. (NASDAQ: SAIA), J.B. Hunt Transportation Services Inc. (NASDAQ: JBHT), and even XPO Inc. (NYSE: XPO) are the subject of discussion after the industry delivered one of the top-performing rallies during the week of the election. The implications point to a trend investors should not only be aware of today but also consider following for their own gain.

Will Analysts Revise SAIA Stock Targets Amid Surging Demand?

The answer is they likely will, as the stock blew past the consensus price target of $492. Wall Street analysts might go into the new week under pressure to update their valuations and price targets on SAIA stock. However, the technical price action is not the only reason they should consider this; there are other fundamental factors at play in this view.

By outperforming all the other industrial niches of the economy for the week, trucking stocks have sent a very strong message for every investor to consider: that business activity within the United States might take on a new uptrend.

After contracting by as many as 24 months consecutively, the manufacturing PMI index now poses as a potential underwater volleyball ready to shoot out of the water, blowing past any other peers and industries for those willing to get behind the message markets just sent.

This might be why Allspring Global Investments Holdings decided to allocate up to 64.6% more of their capital into SAIA stock as of October 2024, bringing their net institutional positioning to a high of $109.6 million today. At the same time, this action amplifies the bullish evidence for the company today.

Then, there is the 12.5% collapse in short interest for SAIA stock over the past month, signaling a significant amount of bearish capitulation and opening the way for a new potential rally in the stock.

Why XPO Stock Justifies Its Premium Valuation Among Peers

While the rest of the transportation sector trades at an average price-to-earnings ratio of only 14.8x today, XPO stock calls for a significant premium by trading at a much higher valuation of 48.7x today.

While some may call this expensive, investors must remember that stocks with a better-perceived future will always trade at premium valuations.

XPO is no exception to this trend. Like its close peer SAIA, XPO stock saw an up to 10.8% decline in its short interest over the past month, opening some room for bulls to replace the bears who were forced to ditch their short positions in the face of the accumulating bullish evidence in XPO.

Investors can see this happening by the 11.3% boost in holdings coming from those at Clearbridge Investments LLC, who now hold up to $264.1 million worth of XPO stock, representing an ownership rate of as much as 2.1% today. After the stock rallied by over 15.6% in a single week, the message is that the ceiling for this stock might be much higher, considering the fundamental tailwinds at play here.

Institutional Investors Dive Into J.B. Hunt Stock After U.S. Election Results

Only a few days after the election results were out, and the price action made it clear that trucking stocks would be a potential favorite for the market in the coming quarters, those at Parnassus Investments LLC decided to increase their exposure to J.B. Hunt stock by as much as 14.1%.

This new allocation brought their net holdings to a high of $129.8 million today, adding to the wave of institutional buying sprees surrounding these stocks. These buying sprees reflect a bullish future view for the industry.

While not by much, daily trading volume increased for J.B. Hunt stock the morning after the election; up to 1.5 million shares were traded for the day, nearly double the average volume of only 880,000. Institutional buyers looking to get a piece of the action in trucking stocks might have aided the renewed trading interest for the coming months.

Now that the landscape has been made clear, there are more pros than cons for investors to consider putting on long positions in these names ahead of what’s coming to them.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Is Tesla's Valuation a Bubble or Backed by Real Growth?"

Post a Comment