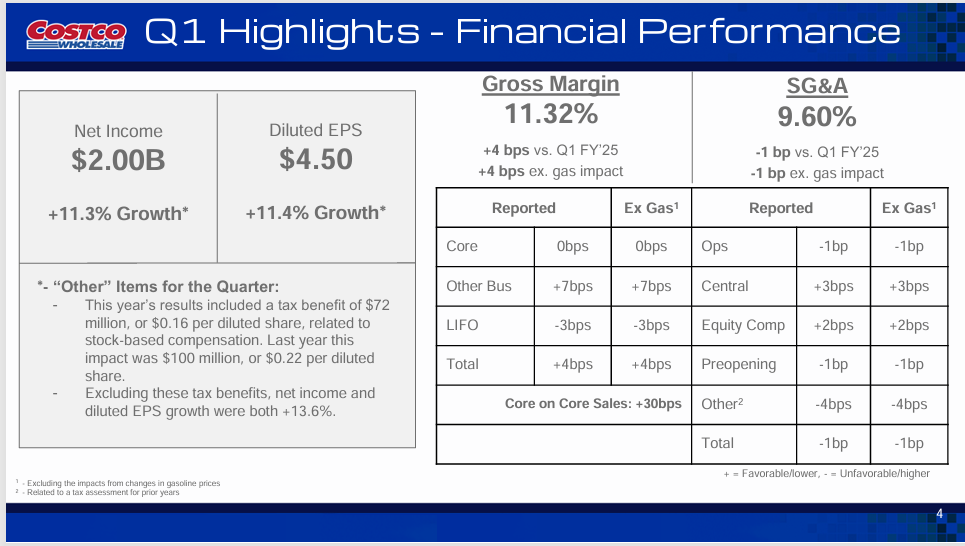

| Nvidia's Networking Chief just revealed where he is convinced the next AI fortune could be made. And here's the best part… You don't need to be a PhD, a Silicon Valley insider, or have millions of dollars in seed capital. Gilad Shainer, Senior Vice President of Networking at NVIDIA, says: "A growing portion of the billions spent on AI [will land here]." Jensen Huang, the CEO of Nvidia, agrees, calling it: "foundational to scaling AI." Yet, these tech titans aren't talking about AI chips, chatbots, or anything like that. It's a hidden AI play few are noticing, one that's quietly becoming one of the fastest-growing cash streams in America today. We just recorded a video on exactly where Nvidia's Networking Chief says billions could flow next… Warning: if you're only focusing on chips and chatbot stocks, you will miss this entirely. Sincerely, P.S. Nvidia just announced it will spend $500 billion over the next 4 years…But a massive chunk of that cash is headed somewhere surprising. It's not AI chips, chatbots, or anything similar. Yet Nvidia's own Networking Chief says fortunes could be made here. Click here to watch the full story now. Today's editorial pick for you Is COST Stock a Buy or a Canary in an Economic Coal Mine?Posted On Dec 22, 2025 by Chris Markoch  As of the market close on December 19, Costo Wholesale Corp. (NASDAQ: COST) stock is down 6.6% in 2025 and over 10% in the last 12 months. This is despite the company's continued pattern of reporting revenue and earnings per share (EPS) that are growing on a year-over-year (YoY) basis. Table of ContentsThe issue is that growth is slowing. The same is true of membership growth, although that's a trickier issue. In Costo's first quarter 2026 earnings report, the company announced a 400,000 sequential increase in membership. However, that’s down sharply from the last few years in which Costco has delivered quarterly membership growth of over one million in several quarters. Of perhaps greater concern was a 10 basis points (0.10%) decrease in the company's renewal rate, which still came in at 92.2% in the United States and Canada and 89.7% worldwide. In response to that metric, Costco said the decline was largely due to a greater prevalence of new members signing up online, who renew at a slightly lower rate than those who sign up at a warehouse location. This creates an interesting question for investors. Is COST stock a buy-the-dip opportunity, or are investors beginning to see evidence that the economy is putting a strain on the company's loyal customer base. History is On the Side of the BullsIt's safe to say that 2025 is an outlier for COST stock. Over any meaningful time period, the stock has delivered a total return that exceeds the broader market. In fact, over the last 15 years, COST stock has delivered a total return of over 1,800%. There's also the company's balance sheet. At the end of the quarter, Costco was sitting on a cash balance of $16.2 billion. That's an increase of over 15% YoY. That kind of cash pile means investors shouldn't be concerned about Costco's financial health. Costco's sound financials are also evident in its growth in both net income and gross margin.  Analyst Sentiment is Better Than it SeemsSince Costco's earnings report, analyst sentiment has been mixed. Many analysts have reiterated a Buy rating (or the equivalent). However, a significant number of analysts have lowered their price targets. The most bearish call came from Roth Capital, which gave COST stock a rare Sell rating with a price target of $769, down from $906. The firm cited the weaker membership trends noted above and steeper competition as two reasons for its opinion. More interestingly, it cited the greater caution around starting a family. I'll admit that could be a longer-term threat. However, it would also be an issue for Walmart (NYSE: WMT) and BJ's Wholesale (NYSE: BJ) both of which are committing to building out more stores. These are legitimate concerns. But they don't account for the fact that although many analysts are lowering their targets for COST stock, the new targets are significantly above the stock's current price. Not to mention, the consensus stock price is about 15% above the stock's closing price on December 19. Two Other Reasons to Buy COST StockFirst, investors get a solid dividend that needs to be put into context. At first glance, some investors might scoff at the 0.67% dividend yield. But the proof is in the payout and the growth of that payout. Costco stock pays out $5.20 per share on an annual basis. The company has increased that dividend for 22 consecutive years, and it has a payout ratio of 27.85%, which means the dividend is safe and well supported given the company's massive cash position. Plus, investors may get a special dividend. One reason that COST stock dropped after its earnings report was that the company declined to confirm if a special dividend would be forthcoming. However, many analysts believe that Costco will announce one before the end of the year as they did in both 2020 and 2023. Second, although the stock has dropped from the $1,000 price it made earlier this year, it still has to be considered a candidate for a stock split. The company hasn't split its stock since 2000 and has indicated that it has no intention of a split at this time. But opinions change. If Costco management believes that the stock price is prohibitive for retail investors, it could take the step to spark demand. The Bottom Line: Know What You OwnLet's look at a "worst-case" scenario. If you believe the report from Roth Capital, then COST stock could have another 10% to fall. However, over the long term, I'd say so what? If you're looking at Costco as a long-term position in your portfolio, then the stock is giving you a buying opportunity today, and it could be an even better buying opportunity at a lower price. Keep in mind that even at 42x earnings, the stock still trades at a discount to its historical average. COST stock has earned the right to have a high valuation. The biggest issues facing Costco are macroeconomic in nature. That's not to say they're not significant. However, until there's evidence that the company's membership is declining as opposed to slower growth, it's hard to bet against the stock's history. This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe. StockEarnings, Inc

|

0 Response to "Nvidia Chief: Where the Next AI Fortune Lands"

Post a Comment