You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here.

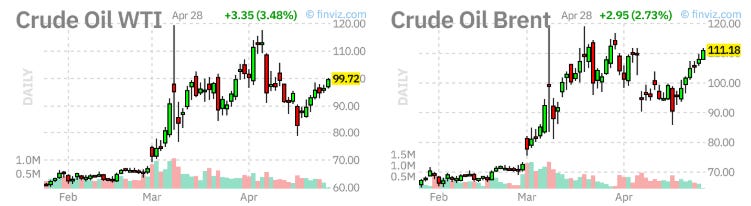

Good morning: We would love to wake up one morning without a fresh slew of Iran headlines. But it is our job to look past the noise and find the opportunity while staying protected. Brent ripped above $110 overnight, gold slipped to a three-week low, and futures are pulling back from yesterday’s records. Trump expressed skepticism about Iran’s latest proposal, and Iran’s Foreign Ministry says no meetings are scheduled between Washington and Tehran at the moment. Try not to look so surprised…

The OILU is now back above its 20-day. That is a real concern. A break back above this level says oil will continue higher in the short term.

The Bank of Japan held at 0.75% overnight in a split 6-3 vote, with three members pushing for a hike given war-driven inflation. They raised their core inflation forecast to 2.8%. No hike in wartime is what you would expect, but the longer energy prices stay elevated, the more dollar support the US has to extend to its allies, which gets costly and feeds back into inflation. It is day one of the FOMC’s two-day meeting. The problem this week is the heavy slate of mega cap earnings hitting at 4 PM tomorrow. Whatever happens between 2:30 and 4 will likely get reset after hours. It will be active and busy, and we will be live to walk you through it. With oil pushing higher and futures pulling back ahead of the Fed, you would expect volatility to be picking up. It is not. The VIX is staying subdued and the channel we have been tracking keeps breaking down. If it breaks back above the levels we identified, the dynamic changes. That is when you take profits on what has been working and move to a cash-heavy position.

If cutting positions is not your style, an inexpensive hedge does the job. The Russell has been the big winner, but it just hit a wall. A TZA call works, or you can buy TZA shares at $5 with a tight stop-loss around 5%. The MACD on TZA looks like it wants to turn. If oil sustains here and the Middle East falls apart, we will be right back in the mess. None of our numbers are pointing that way yet. Volatility is falling and volatility of volatility is falling with it.

The FNGD continues to drift lower, which tells you collateral quality in the Mag 7 is fine. If something shifts in these earnings, we will see it there first. The FAZ started to curl higher last week and looked like it might be getting hairy, with the Warsh nomination uncertain. With that clearing, FAZ is back below its 100-day and looks ready to break down further. The only real concern is rising oil prices, which make the dollar more desirable and put pressure on metals and commodities.

This is Scott Bessent’s market now. Warsh was step one for him. Will they one day write about Bessent the way they write about Volcker or Burns? Time will tell. To suggest anyone else is at the helm right now would be a stretch. This is his strategy, and it represents a major shift in how the world is going to operate. And in how much tolerance the US is willing to allow for those skirting international rules to move energy, fund wars, and make money in the shadows. Today brings consumer confidence, JOLTS, and a heavy slate of pre-market earnings. Coca-Cola, GM, UPS, Visa, Starbucks. Tomorrow is the Fed plus the four mega caps. Thursday brings GDP, PCE, ECB, and Apple. It’s a lot. Our momentum signal remains positive and the instruments are holding up, but this is not a week to get overly aggressive. Market outlook

Momentum - Concentrated Climb Russell has been confirmed bullish for nearly three weeks running. That is a long stretch for the small-cap signal. It is happening alongside a chip rally where Intel is up 75% on the month and several other semis are running 50% gains. The cap-weight read on the S&P ripped overnight while equal-weight barely moved. These are the kinds of single-name moves that pull performance chasers in late and force everyone else to reposition into the leadership.

The lower half of the market is doing the opposite. Defense and healthcare names have been on the crasher list for a week. Software and consumer names joined more recently. The dispersion is the widest of this rally so far. Money is rotating into a small group of names and out of a much wider group at the same time. The leadership is real but stretched. Chips this hot rarely add another 50% in three weeks. Russell cannot extend its streak forever on its own. Either the underlying market firms up to support the leaders, or the leaders take a breather. BOJ delivered a hawkish hold this morning. Fed and mega-cap earnings stack Wednesday. Those events tell us whether the chip rally translates into the rest of the index priced for it. This is the week the rally either earns its records or starts giving them back. Insider Buying: Still Slow… (Blackouts)

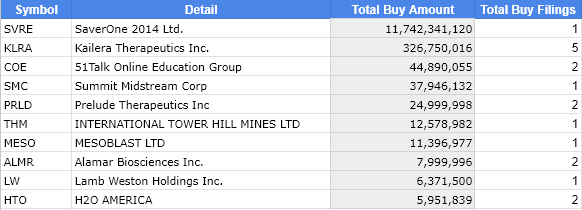

Top Insider Buys of Last 10 Days - Form 4 Documents

Market Liquidity The Federal Reserve changes hands on Wednesday. The Senate Banking Committee votes on Kevin Warsh at ten in the morning. Powell delivers his last policy decision and press conference at two. By the close, the rate-cut bets that jumped to 40% on Friday will have a fresh read on whether the next Fed chair will do the easing markets are now pricing. The handoff is happening at what may be the worst possible moment. Oil is sitting near $108 and the dollar is rallying against most G10 currencies, while Gulf and Asian allies are still asking Bessent for swap lines. PCE inflation lands on Thursday into all of it. Bessent has been doing the actual policy work in the background. The TGA is past its tax-season peak and starting to draw down again. Treasury auctioned 2-year and 5-year notes yesterday with another 7-year today. The indirect bidder demand on those auctions is the closest thing we have to a real-time vote on whether foreign capital is still willing to fund our debt at these yields. Powell can leave the Fed in a quieter spot than he found it, but he cannot leave the next chair a quiet picture. The conditions Warsh is about to inherit are tighter than the inflation prints suggest and looser than the Fed’s stated stance implies. That is the spread he starts with. Stay positive. Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "Money Printer Pro - 4/28"

Post a Comment