Ticker Reports for July 31st

Joby Aviation Stock: The Case for Upside Just Got Stronger

There is a bull case for Joby Aviation (NYSE: JOBY) that has nothing to do with the June CPI report, but that report made it stronger. The case is stronger because the CPI was cooler than expected, affirming the outlook for interest rate cuts. The outlook for interest rate cuts means an economic pivot will begin later this year, as early as September, which means better times lie ahead.

This means it is time for the market to rotate out of large-caps and mega-tech in favor of riskier assets, assets known to perform well in a falling-rate environment. That means small caps and the Russell 2000, of which Joby is a part. The takeaway is that Joby has a bull case for its stock price because of its business outlook, and now a secular tailwind begins to blow.

Joby Aviation Leads the Charge in eVTOL

Joby Aviation is an emerging technology company specializing in electric vertical take-off and landing (eVTOL) and air-taxi services. Its proven technology has undergone thousands of hours of test flights and is on track for FAA and other approvals in early 2025. Commercial operations are expected to begin soon after, including air taxi service in key U.S. cities such as New York and Los Angeles and services in Dubai and India. Joby also has contracts with the government that are expected to lead to sustained business. As it is, the government contracts provide a small revenue stream to help offset its development-related cash burn.

Three news updates have recently triggered Joby’s stock price. Two involve acquiring Xwing autonomous flight software technology and an in-house software suite that enables end-to-end, easy, scalable air taxi operations. Those developments go hand-in-hand and will facilitate operations moving forward. The addition of Xwing technology is expected to aid eVTOL operations today.

The third development is a successful test flight of Joby’s hydrogen fuel-cell eVTOL aircraft. The fuel-cell components were fitted to an existing JOBY airframe with minimal modifications, paving the way for expanded services to include regional operations. The fuel cell allowed Joby’s aircraft to fly 523 miles, far further than the electric model, using only 90% of the fuel capacity and leaving only water in its wake. Because the craft was built on an existing airframe, the path for regulatory approval is much easier and far less costly than developing an entirely new vehicle.

Joby Aviation is Well-Funded and Has Significant Industry Support

Joby Aviation is not advancing its technology alone. It has significant funding from partners, including Toyota Motors (NYSE: TM), Delta Airlines (NYSE: DAL), and Uber (NYSE: UBER), not including contracts with USAF and NASA or deals with foreign governments to introduce their services abroad. Unless there is some unknown development, it is unlikely that JOBY will fail.

The takeaway from the Q1 report is that cash burn declined, came in below $95 million, and there is still more than $900 million on the books. That is sufficient to sustain operations at the current rate of cash low for more than two years, long enough to see the company commence its commercial operations. Even so, there is some risk of dilution.

JOBY Stock Price Can Fly Much Higher

Only two analysts have issued ratings this year, but the news favors investors. The two are from JPMorgan Chase & Company (NYSE: JPM) and Cantor Fitzgerald, with a consensus of Moderate Buy and a price target of $8. The range of targets is $6 to $10, which implies the stock is fairly valued at current levels with a chance of 30% upside at consensus and 60% at the range’s high end.

The Q2 results due in early August are the next catalyst for price movement. Analysts expect revenue of $500,000 related to the government contracts and for the losses to narrow. While results are important, the market moving details will center around the certification process, production schedules, and the timing of commercial operations.

Nvidia's Quiet $1 Trillion Pivot

Nvidia recently added $277 billion in market cap …

IN ONE DAY.

Conviction Firms for Microsoft's Double-Digit Stock Upside

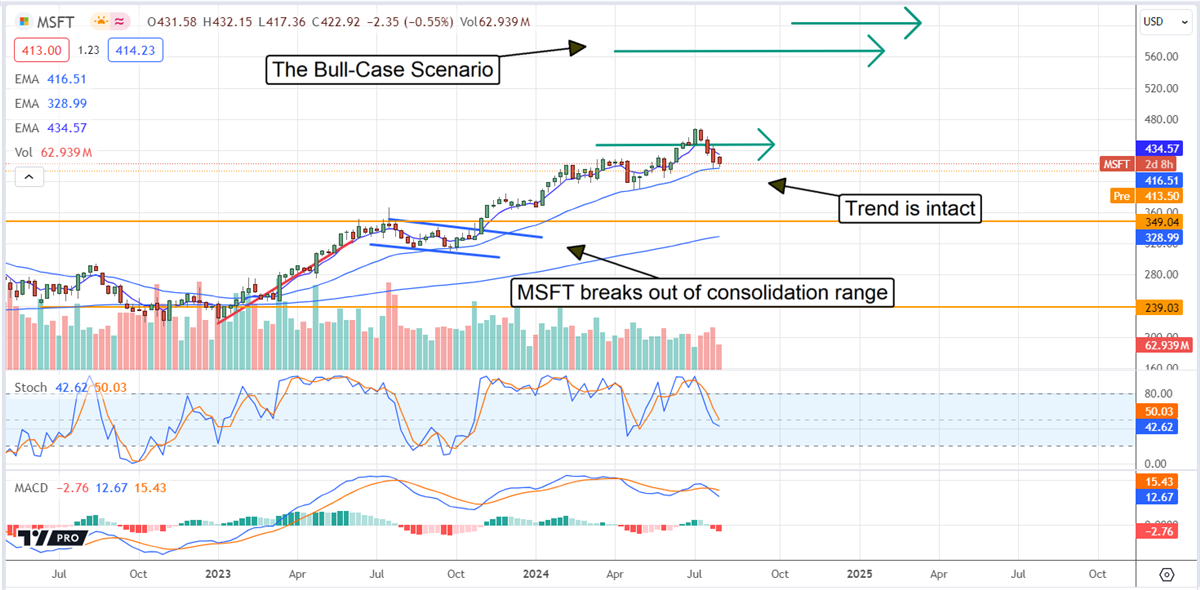

Microsoft (NASDAQ: MSFT) shares are falling, and this is a buy-the-dip opportunity. The Q4 results failed to spark a rebound in share prices but give no reason to shed a position and every reason to believe a double-digit upside will come soon. The biggest concern from the report is that growth just isn’t as hot as it could be. It’s hot, supported by all segments and AI, guidance is decent, and we’re still in the early stages of a secular tech upcycle, so the long-term rally in share prices will likely continue.

The analysts' activity following the release is mixed, and most revisions are reduced price targets but don’t read too much into that. Price targets are coming down but narrowing into a range above the current consensus estimate. The range of new targets runs from $475 to $550, with the $550 target a re-affirmed target from Wedbush. The average and median of these new targets are near $500, which are significant targets for technicians.

A move to the $500 level would set a new all-time high, confirming a major uptrend in the stock price. However, this is a low estimate compared to the longer-term target. The stock price broke out of a multi-year consolidation late in 2023, and a move to new highs would bring the bull-case scenario of MSFT near $600 closer to reality.

Microsoft Outperforms, Guidance is Good; Buy the Dip

Microsoft’s shares fell following the Q4 release and guidance because analysts got what they wanted and nothing more. The takeaway is that Q4 revenue grew by 15.1% YoY and outperformed the consensus target reported by MarketBeat by 40 basis points. Growth was seen in all segments, with Intelligent Cloud up 19%, followed by a 14% gain in More Personal Computing and an 11% increase in Productivity and Business Processes.

Digging deeper, all subsegments but one produced growth; the single outlier is devices, which should see a rebound soon. The sub-segment that disappointed the market is Microsoft Cloud, specifically Azure, which grew by only 29%, slightly below company forecasts but strong nonetheless.

Margin is another area of strength. The company maintained its system-wide gross and operating margin to deliver a 15% operating income gain. That was cut to 10% after spending, which was still better than expected, leaving GAAP EPS at $2.95, up 10% and 68 basis points above consensus. Similarly, guidance is strong but provides no catalyst to rally. Expecting double-digit top and bottom growth in fiscal 2025, it is a hair shy of consensus.

Microsoft is Building Value for Investors

Microsoft had a negative cash flow quarter, which is the worst that can be said. The offsetting details are that cash burn was minimal, and the balance sheet was greatly improved. Highlights include reduced cash offset by increased receivables, investments, goodwill, and intangibles. Current and total liabilities are up but less than the increase in assets, leaving equity up by 30% compared to last year. Because leverage remains low at .16x equity, .08 assets, and roughly 3x cash plus receivables, it is in a strong financial position to continue capital returns and business investments.

The price action in MSFT stock is down in early trading, near the recent lows, but has not broken the trend. There is a risk that the market could fall below the $415 level and continue lower, but that is not expected. The likely scenario is that investors will buy the dip in this stock and create a trend-following signal. In that scenario, MSFT will likely retest the all-time highs later this year and may set a new high by the year’s end.

BITCOIN

Did you miss out on the 1000%+ gains of Bitcoin over the past 5 years?

If so, you don't want to miss this...

5 Aggressive Growth Stocks for Long-Term Investors

What Are Aggressive Growth Stocks?

Aggressive growth stocks are shares of companies that are expected to grow at an above-average rate compared to other companies. They tend to be concentrated in the tech, biotechnology and consumer discretionary industries, which leave more room for growth and opportunities on average. Growth stocks are typically characterized by:

- Greater Volatility: Due to their high growth potential, these companies may have less stable earnings and higher price fluctuations.

- Reinvestment of Earnings: Instead of paying dividends, aggressive growth companies usually put that money into research and development, marketing, and expansion efforts to fuel further growth. As a result, the most aggressive growth stocks may have a very small dividend yield percentage or no dividend payment at all.

- Higher Price-to-Earnings (P/E) Ratios: Aggressive growth stocks often trade at higher P/E ratios than more mature companies because investors are willing to pay a premium for the expected future growth.

- Innovative and Disruptive Business Models: Aggressive growth companies often focus on innovative products, services, or technologies that can disrupt existing markets and create new opportunities.

What Are the Top 5 Aggressive Growth Stocks?

Let's take a look five aggressive growth stocks that stand out in the current market due to their impressive growth potential and strategic initiatives.

1. NVIDIA

Seeing huge increases in demand due to its dominance in the computer processing sphere, NVIDIA (NASDAQ: NVDA) is renowned for its pioneering work in graphics processing units. Since last year, the company has seen a 179% increase in its share price, with its total market capitalization reaching $2.88 trillion in June of 2024. This dominance has solidified its space within the tech sphere while also leaving opportunities for new developments.

NVIDIA has seamlessly expanded its influence into burgeoning fields like artificial intelligence and automated vehicles, which has led to revenues that compound alongside investor interest. Despite its high valuation, the market remains optimistic about NVIDIA's ability to sustain its growth, which is driven by continuous innovation and strategic acquisitions of companies like data center giant Mellanox. The ongoing demand for AI combined with worldwide data storage needs is likely to position NVIDIA as an option for continued growth.

2. Shopify

Shopify (NYSE: SHOP) stands out as a quintessential growth stock, especially in the rapidly expanding e-commerce era. Shopify is notable for its compatibility with web service providers like WordPress, a relationship that provides small businesses access to online customers without hiring a private web developer. It also offers physical hardware that allows small business owners to accept credit card and virtual wallet payments in-person.

Like most aggressive growth stocks, Shopify is a more volatile stock option, with a beta rating of 2.3. However, for inventors with a higher risk tolerance, it can provide a potential opportunity sparked by its surge in revenue that began in 2023. Since March of 2023, Shopify had a total revenue of $1.86 billion — an increase of 23.41% over the last year. In July of 2024, it also had a total market capitalization of $77.24 billion, with a large percentage of its revenue re-diverted back into growth rather than distributed in dividend payments.

3. Meta Platforms

Meta Platforms (META) – the parent company of Facebook, Instagram, and Whats App – has been making significant investments in artificial intelligence, virtual reality, and augmented reality to diversify its revenue streams beyond advertising. The company has been focusing on developing the metaverse, a virtual shared space integrating digital and physical realities, which promises substantial future growth potential.

The company’s social networks continue to see significant user growth and engagement, driving revenue expansion, with a 7% year-over-year increase in daily active users. Additionally, Meta has been enhancing its operational efficiency, which is reflected in its robust $58.12 billion cash position. This substantial cash reserve will enable Meta to fund its ambitious projects and better withstand market volatility.

4. CAVA Group

Cava Group (NYSE: CAVA) may not be as large as its direct competitor Chipotle, but the southeastern fast-casual restaurant has been on a steady valuation rise since 2023. Known for its Mediterranean-inspired menu, Cava has tapped into the growing consumer preference for healthy and convenient dining options. Its impressive same-store sales growth and robust revenue increases reflect its ability to attract and retain a loyal customer base.

Cava began an aggressive expansion strategy in late 2023 that continues into mid-2024, opening 14 stores in the first half of 2024 alone. The company's strategic use of technology for operations and customer engagement enhances its scalability and efficiency, driving further growth potential. In July 2024, it had a total market capitalization of $9.1 billion. The company's successful initial public offering (IPO) has provided it with substantial capital to fuel further growth and expansion.

5. Tesla

No list of aggressive growth stocks is complete without mentioning electric vehicles (EV) and renewable energy giant Tesla (NASDAQ: TSLA). Tesla has demonstrated a consistent rise in both valuation and revenue, up almost 20% in the last six months. While its total market capitalization remains at $702.1 billion, Tesla has seen a rough recent quarter, with weak sales of EVs contributing to a 45% decline in profit year-over-year. Despite this, the company's focus on cutting-edge technologies, such as autonomous driving and battery advancements, positions it at the forefront of automotive and energy innovation and presents unique opportunities for investors.

Tesla's aggressive expansion includes building new Gigafactories worldwide to increase production capacity and meet growing demand. The company's ventures into energy storage solutions and solar products further diversify its revenue streams and enhance growth potential. Tesla's strong brand, loyal customer base, and significant market share in the EV industry contribute to its high valuation and growth expectations.

Why You Should Consider Investing in Aggressive Growth Stocks

If you have a higher risk capacity, meaning you are willing to take on more risk in exchange for more potential returns, introducing aggressive growth stocks to your portfolio can provide a healthy level of volatility. Consider investing in aggressive stocks if you’re looking for:

- High Growth Potential: Aggressive growth stocks are usually issued by companies that have the potential for rapid and substantial increases in revenue or market share. This can lead to significant capital appreciation over time, with investors able to profit from the difference in share price.

- Exposure to Innovative Industries: Most growth stocks are found in the biotechnology or technology sectors, which are known for exceptional innovation. Investing in these sectors early can provide you with access to groundbreaking developments and future trends, which may further drive capital appreciation.

- Market Leadership: Many aggressive growth companies are early movers in their respective industries, allowing you to capitalize on the company's market leadership and competitive advantages as the industry matures.

- Compounding Growth: Since companies often reinvest their profits into further growth, the potential for compounded returns over time increases.

Risks and Considerations of Investing in Aggressive Growth Stocks

Investing in aggressive growth stocks can be highly rewarding, but it also involves considerable risks that investors should carefully consider before committing their capital, such as:

- More Volatility: Aggressive growth stocks often experience more market volatility, with drastic potential price changes based on market sentiment, quarterly earnings, and changes in growth prospects.

- Valuation Concerns: Growth stocks often trade at high P/E and price-to-sales (P/S) ratios, reflecting high expectations for future growth. Companies that fail to meet these expectations may see sharp, sudden price decreases. High valuations can also lead to overvaluation and potential price corrections.

- Economic Cycle Sensitivity: During periods of economic stress, consumer and business spending may decrease, affecting growth companies disproportionately.

- Industry Risk: Operating in emerging or rapidly changing industries can expose companies to sector-specific risks, such as regulatory changes or technological obsolescence.

- Significant Competition: High-growth sectors often experience intense competition, which can impact a company’s market share and profitability.

Should You Invest in Aggressive Growth Stocks?

Investing in aggressive growth stocks can add a unique level of potential for capital appreciation. As with most investments, whether or not you should add them to your portfolio depends on your personal investment goals and risk tolerance. Aggressive growth stocks stocks fit best with investing strategies that operate on a longer timeframe, which gives them more flexibility in refining their growth strategy. It’s important to remember that these stocks come with more risk than more stable, blue-chip stocks and can be especially sensitive to economic cycles.

If you’re interested in investing in aggressive growth stocks but are looking for a more general way to take advantage of these companies’ bold strategies, consider a growth mutual fund. These aggressive growth stock mutual funds spread your risk between multiple companies by investing in a series of shares rather than stock in one company.

Start Your Research with MarketBeat

To invest in aggressive growth stocks, you need a higher level of risk tolerance than investing in total market funds or blue chips. Keeping up-to-date with how the markets are moving each day is an essential step in successful growth investing. Subscribe to MarketBeat’s free and premium research reports to have breaking news delivered straight to your inbox, and stay ahead of the movements making the market.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 5 Aggressive Growth Stocks for Long-Term Investors"

Post a Comment