Ticker Reports for August 1st

First Solar Stock: The Dawn of a New Rally in Share Prices

First Solar's (NASDAQ: FSLR) stock price was corrected to lower levels in early summer because of mounting concerns centered on political risk, but its operational quality continues to shine. The upcoming election threatens the solar market in several ways but nothing to offset the growing demand for solar power generation and the secular tailwind that has begun to blow. That tailwind is derived from the inflation data and outlook for interest rates expected to fall soon. The takeaway is that easing economic conditions will help boost demand for an in-demand product and drive results for this profitable business.

First Solar Has a Robust Quarter, but Bookings Slow

First Solar had a solid quarter, with demand driven by the data center segment. Data centers are turning to solar power generation to help offset the enormous cost of powering AI. The company reported $1 billion in net revenue, outpacing the consensus estimate by 60 basis points as growth surged 23% YoY and 25% sequentially. The gains were made on increased volume, compounded by higher realized prices, which leveraged strength on the bottom line.

The margin news is impressive and includes improved gross margin and operating costs. The gross margin improved by 1000 basis points, compounded by reduced costs. The net result is that operating and net income more than doubled, driving a 75% increase in GAAP earnings. The GAAP earnings were impacted by mild dilution, with the diluted share count up about 20 bps compared to last year. Dilution is related to share-based compensation and is not a red flag for investors today.

Among the attractions of a First Solar investment are its profitability, cash flow, and financial strength. The company had a cash flow-negative quarter. However, one-offs, including start-up costs at new facilities and the repayment of short-term operating capital loans in India, offset that detail. The salient details include a net cash position of $1.2 billion, low leverage, and an 8.4% increase in shareholder equity. Regarding leverage, the company’s total liabilities are about 0.5x equity and long-term debt about 0.05x equity, leaving it in a robust position to reinvest in the business as needed, and capital return is a growing possibility.

Among the hurdles for First Solar’s stock price is bookings. Booking growth slowed in Q2, attributed to political uncertainty and economic conditions, leaving the backlog down 2.4 GW sequentially or 3%. The 3% contraction is not large but sufficient to offset quarterly strength, leading management to reiterate guidance despite those strengths.

Analysts Look Past Elections to First Solar’s Bright Future

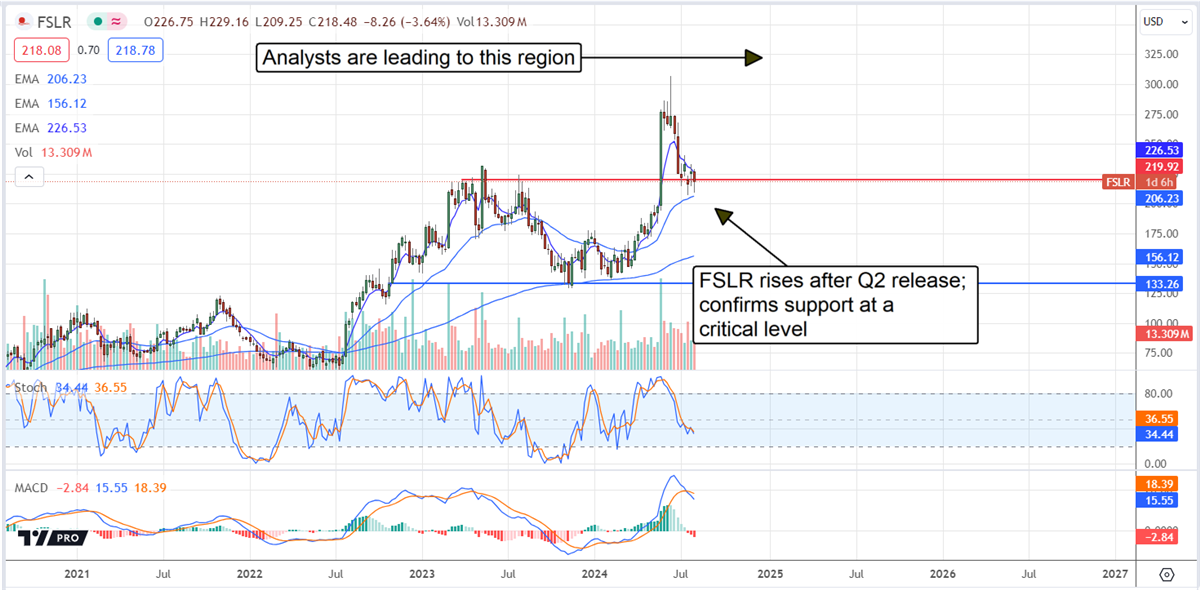

The analysts' response to the Q2 results is positive, including numerous upward price target revisions. The talk on the street is that bookings slowdown and policy risk are a concern but offset by secular growth drivers, including data center demand and pricing power. Potential catalysts for outperformance and higher share prices include technological advances and increased efficiency for First Solar’s industry-leading products. The takeaway is that analysts' revisions are leading to a range above the consensus target, implying at least a 30% upside and the probability new highs will be set. The $273 consensus target aligns with the current all-time high, but the freshest targets range from $300 to $350, well above it.

First Solar’s stock price is rising following the Q2 release and showing support at a critical level. That level aligns with the 2023 highs broken earlier this year. The pullback to $220 and show of support at that level confirms the breakout, setting the market up to continue the rally. The next price movement is likely upward and may reach $250 to $275 before the next quarterly release. If the company continues showing strength, new highs are likely before the end of the year.

A Silent Invasion of America

The 'invasion' I've discovered has nothing to do with the border crisis. What's happening at our southern border is a travesty, but the 'invasion' I've found will have 10 times greater effects on our economy, and ultimately our way of life.

Go here to see why.

Mastercard Stock's Q2 Financial Results Outshine Competitors

Mastercard (NYSE: MA) is the third largest company in the United States financial services industry, with a market capitalization of $431 billion. The firm released Q2 2024 financial results on July 31, 2024. We will review key points from the earnings release and explain the company's diverse revenue streams. We'll conclude by highlighting critical factors to monitor around the firm and share updates on Wall Street analysts' price targets.

Mastercard operates as one reportable segment, known as Payment Solutions. In 2023, 30% of the company’s revenue came from the United States, and no one customer contributed more than 10% of the revenue.

Mastercard Beats Adjusted EPS and Revenue Estimates, Impressing Over Visa

Mastercard beat adjusted earnings-per-share estimates, coming in at $3.59, for an earnings surprise of 2.3%. The figure increased by 24% from the previous year. Revenue also beat estimates by $110 million, coming in at $6.96 billion. This was an increase of 11% and represents a revenue surprise of 1.6%.

The company reiterated its full-year revenue guidance of low double-digit growth. Mastercard attributed its rising revenue to growth in its payment network and value-added services and solutions.

Payment network revenues were up 7%, driven by a 9% increase in gross dollar volume, a 17% increase in cross-border volume, and an 11% increase in switching transactions. Gross dollar volume is the dollar amount of transactions the company’s payment network facilitates.

Cross-border volume refers to the value of transactions made between parties in different countries. These transactions often generate higher fee revenue. When a sale is made, transactions are switched to transfer money from the purchaser's bank to the merchant's bank.

Value-added services and solutions include cybersecurity solutions that help detect, prevent, and respond to fraudulent activity or cyberattacks. The company also provides data and insights. They help firms understand market trends, increase value, and reach customers. Revenue in this division was up 18% from last year. On the day of the release, shares were up 3.6%.

This was a positive earnings report, especially when comparing results to Visa (NYSE: V), which released earnings last week. Mastercard beat Visa’s 7% increase in gross dollar volume and its 14% increase in cross-border transactions. Visa’s shares fell 3% on the day of its release.

What to Watch For: Merchant Lawsuit, Consumer Spending Readings

One issue to watch around Mastercard is developments in the lawsuit the company is currently in. Merchants using their payment systems are currently suing Mastercard and Visa. The merchants accuse Visa and Mastercard of being a cartel. A cartel is when two powerful firms collude to fix prices. This helps attract business for themselves and shut out competitors.

Merchants believe that Visa and Mastercard use their cartel to charge excessive interchange fees when processing transactions. They argue this has unfairly hurt their businesses.

Visa and Mastercard arranged a settlement for the case in March 2024 with several avenues to relieve the merchants. First, the companies offered to pay the merchants a collective $30 billion. They also agreed to lower fees by at least 4 to 7 basis points for the next three to five years. The current fee range is approximately 1.5% to 3.5% of transactions.

In June, a judge rejected the settlement deal; the case will now go to trial. When it comes to class action lawsuits, companies typically end up paying less when they can settle out of court. Now that the case is going to trial, Mastercard’s eventual bill and changes in agreements with merchants could be much harsher. Investors should watch for news of a revised settlement that would help keep Mastercard’s liability more reasonable.

Updated Analyst Price Targets

Investors should also watch for the next consumer spending reading, which will be released on August 31st. This number is indirectly tied to the revenue that firms like Mastercard will bring in, as more spending means the company can charge more transaction fees.

Since the earnings release, five Wall Street analysts have updated their price targets on Mastercard. All of them increased their estimates. The average price target among those analysts is $532, implying an upside of 13%.

Goodbye to Cash: The Era of the Digital Dollar Revolution Begins

Something critical just happened... In June the BRICS nations — Brazil, Russia, India, China, and South Africa — met. They weren't just chatting about trade. No, they were plotting to dismantle the dominance of the U.S. dollar in global trade. A new trade system, free from the dollar. What does that spell for the dollar's future? Trouble.

Download Your FREE Guide Now >>

Tobacco Giant's Shares Fall on EPS Miss, Lackluster Pouch Gains

Altria Group (NYSE: MO) is one of the world’s “Big Three” tobacco companies and is in the consumer staples sector. Let's examine the firm’s business segments and the state of the cigarette market. We'll then review its Q2 2024 earnings report and examine the company’s growth areas.

Altria's Segments: Smokeable Products Dominate

Altria divides its revenue into smokeable products, oral tobacco products, and “all other." Smokable products include cigarettes and cigars. Altria’s main brands are Marlboro, the best-selling cigarette in the US, and Black and Mild. It made up 92% of operating income in 2023.

Oral products include chewing tobacco and nicotine pouches. The company’s brands include Copenhagen and Skoal chewing tobacco and On! nicotine pouches. These products made up 8% of operating income. The “all other” segment includes the firm’s NJOY e-vapor product. It accounted for less than half a percent of total revenue and lost money, subtracting from operating revenue by 3% in Q2 2024.

To understand Altria's business model and performance, it's essential to focus on cigarette usage trends and how the company has navigated them, as cigarettes are still Altria's biggest product category.

The Decline of the Cigarette Industry and How Altria is Fighting Back

Demand for cigarettes has fallen considerably over the last 25 years. In 2000, 25% of U.S. adults surveyed said they had smoked cigarettes in the past week. In 2023, the number sat at 12%. Data also shows that those who smoke consume fewer cigarettes a day. As a result, the number of cigarettes sold per year in 2021 was half of what it was in 2000.

However, Altria Group has continued to grow its profits and has only seen modestly decreasing revenues over the past two fiscal years, down 2% and 0.9% in 2022 and 2023, respectively. Over the past three years, operating income has grown by a compound annual rate of 2%. Altria has been able to achieve this by substantially increasing its margins. Operating margin, gross margin, and adjusted net income margin have all expanded by 400 to 500 basis points since 2020.

Much of this has been achieved through cigarette price increases; Altria hiked prices four times in 2023 and has already done so once in 2024. Due to nicotine's addictive properties, Altria has the power to increase its prices and not substantially lower volumes. Additionally, brand loyalty for cigarettes is extremely high, estimated at 85% to 90% annually. This makes it even more unlikely that consumers will switch products due to price increases.

If smoking rates continue to decline as expected, then those who remain smoking will have to continually pay higher prices so that companies can increase their bottom line. This will be offset by new products that firms hope will attract new generations of nicotine users. Ultimately, growth will have to come from new products.

Altria's EPS and Revenue Miss

Altria Group’s adjusted earnings per share (EPS) came in at $1.31, which is three cents below estimates and flat from the previous year. Revenue also came in $120 million below estimates at $5.28 billion. Net revenues declined 4.6% from the previous year. The company also narrowed the range of its full-year adjusted EPS guidance slightly but maintained the same midpoint of $5.11.

Overall, smokable product volume decreased by 13%, but revenue only fell by 5.6%, showing the disproportionate ability to raise prices.

Analyzing Altria's Growth Areas

Altria is touting the expansion of its NJOY vapor product. Its share of the vapor device market increased by 14%, up to 25%. “All other” segment revenues grew 144%, but they are so small, at $22 million, that they make no difference to the bottom line.

A more encouraging avenue is in Altria’s On! nicotine pouches. It increased volume by 37% from Q2 2023, drastically higher than the volume growth in the oral tobacco industry. On! also increased its market share by 1.2% since Q2 2023.

Key competitor ZYN, made by Philip Morris (NYSE: PM), is losing market share due to its inability to keep up with demand. In April 2024, ZYN controlled an estimated 26.8% of U.S. smokeless tobacco sales. Considering the massive shortage in its biggest competitor, it feels disappointing that Altria was barely able to increase its market share.

Shares were down 3% on the day of the release. The glaring negatives regarding EPS, revenue, and guidance were the 2.2% misses on EPS and revenue. This, combined with On!'s disappointing performance, makes the reaction feel justified. Investors should continue to see if On! and NJOY products can gain further market share. However, these product lines have an extremely long way to go, and results so far are not great.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Tobacco Giant's Shares Fall on EPS Miss, Lackluster Pouch Gains"

Post a Comment