Ticker Reports for September 3rd

Analysts Forecast Big Upside for Western Digital—Don't Miss Out

As a leading provider of data storage solutions, Western Digital Co. (NASDAQ: WDC) stands at the forefront as a key benefactor of the artificial intelligence (AI) data cycle. AI requires processing power from GPUs, low latency networking from optical controllers, and massive storage capacity and performance for processing, analyzing, generating, and storing oceans of data. The latter is where Western Digital thrives.

The computer and technology sector giant competes with Seagate Technology Holdings plc (NASDAQ: STX), Pure Storage Inc. (NYSE: PSTG), and Dell Technologies Inc. (NYSE: DELL).

Despite the AI boom boosting shares of AI benefactors, Western Digital's stock has fallen 19.5% off the 52-week highs. Its softer guidance for fiscal Q1 2025 is attributed to the sell-off after a solid fourth-quarter EPS beat on 41% YoY revenue growth. Here are four reasons to consider buying the pullback.

1) Western Digital Gains From the AI Data Cycle

It's no surprise that the AI boom is bolstering Western Digital's business. Revenues for its fiscal Q4 2024 surged 41% YoY to $3.76 billion, beating $3.75 billion consensus estimates. Western Digital produces both hard disk drives (HDD) and flash solid-state drives (SSDs). While AI applications require fast memory from flash arrays, they also require HDDs to store massive amounts of data. The two major segments of its business benefit:

- Flash storage is most useful for AI inference, training AI models, and running AI applications due to flash speed. Processing, analyzing, and generating new data is a continuous active cycle that relies on the speed of access to new data. Flash storage is more expensive, but not all the data needs to be quickly accessed all the time. This is why HDD storage is necessary.

- HDD storage is most useful for storing the massive ocean of data that AI models need for training. It's also critical to store the results of AI applications. HDDs provide much more bang for the buck with lots of storage capacity for a lower cost than flash. HDD also carries wider margins for Western Digital.

2) Western Digital’s Flash Business Spin-Off Enhances Shareholder Value

Western Digital has already announced plans to separate its businesses into two standalone public companies. Western Digital will keep the name for its HDD business. The flash NAND/SSD business will be spun off into a separate public company in late 2024. There is speculation of a merger with Japanese flash memory manufacturer Kioxia. Western Digital uses Kioxia fabs to manufacture NAND devices. However, South Korean giant SK Hynix opposes the merger. The rumors are the split of the newly merged company would be owned 43% by Kioxia and 37% by Western Digital, with the rest owned by existing shareholders of both companies.

3) Western Digital Stock is Cheap Trading at 7.51x Forward Earnings

Competing HDD giant Seagate Technology's stock trades at 14.81x forward earnings. Western Digital's stock trades at half at just 7.51x forward earnings. Western Digital's debt-to-equity ratio is 0.53, and the current ratio is 1.32. It's trading at just 1.65 price-to-sales (P/S), compared to Seagate trading at 3.19 P/S.

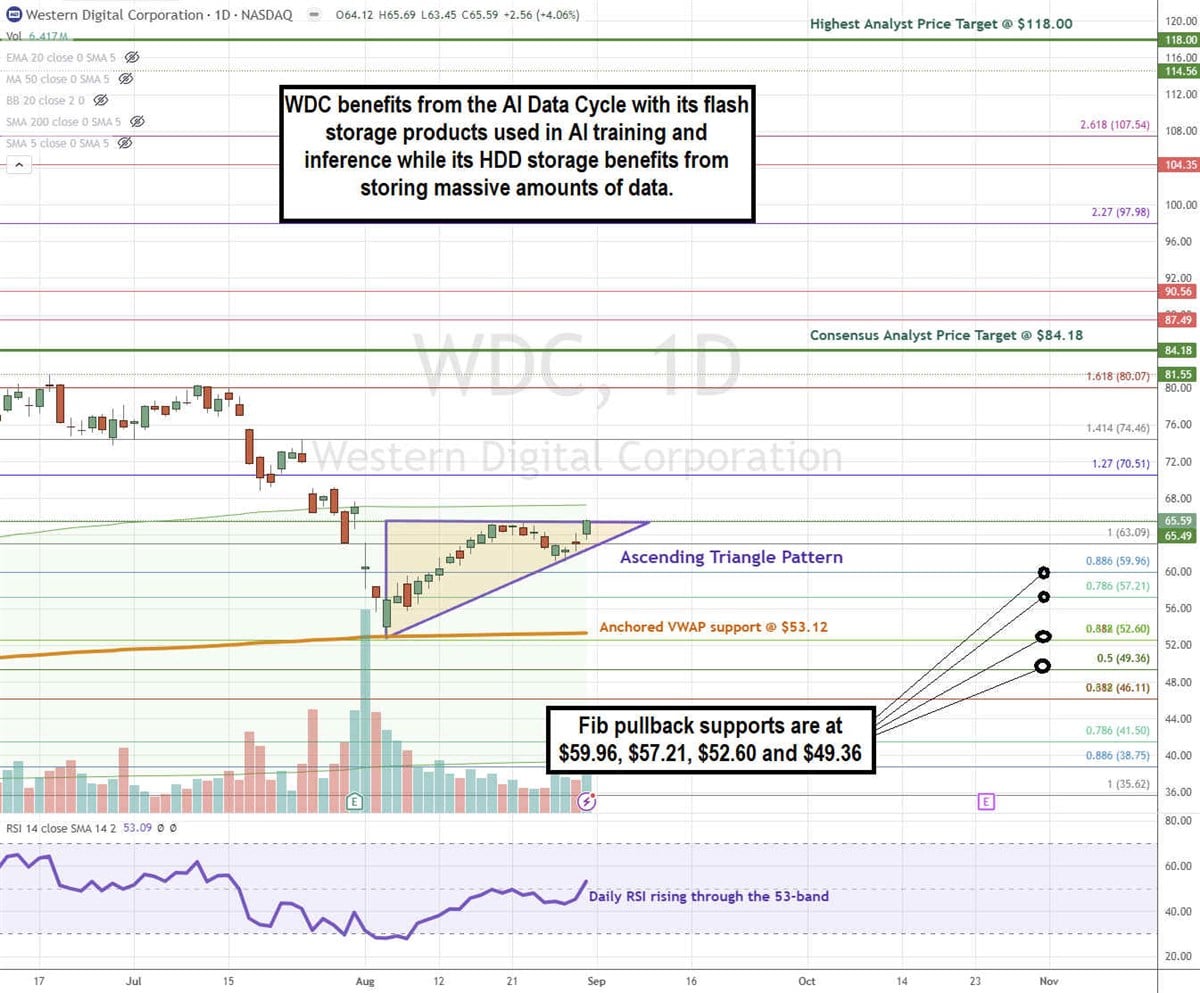

4) WDC stock is Attempting an Ascending Triangle Breakout

An ascending triangle pattern consists of a flat-top upper trendline resistance connected at the apex to the ascending lower trendline, indicating higher lows.

WDC commenced its ascending trendline off the $52.60 swing low, which was also a Fibonacci (fib) support overlapping with the anchored VWAP support. Shares rose to the flat-top upper trendline resistance at $65.59. The ascending lower trendline continues to rise as it nears the apex point. WDC will break through the upper or lower trendline as it nears the apex point. The daily RSI is rising through the 53-band. Fib pullback support levels are at $59.96, $57.21, $52.60 and $49.36.

Western Digital’s average consensus price target is $84.16, and its highest analyst price target sits at $118.00. The daily anchored VWAP support sits at $53.12.

Actionable Options Strategies

WDC bulls can enter on pullbacks using cash-secured puts with trail stops under the anchored VWAP. A wheel strategy can be implemented upon being assigned shares and writing covered calls to generate income.

![⭕ [URGENT] Buy Alert just triggered](https://www.marketbeat.com/images/webpush/files/thumb_2059push_Picture6.png)

⭕ [URGENT] Buy Alert just triggered

My absolute favorite stock just hit a critical "buy now" trigger price.

Click here for the ticker >>>

3 Must-Own Stocks for Bullish Investors in Today's Market

Bears will always have a reason to bet against the market, even a roaring one like today’s S&P 500 making high after high. Not even the so-called carry trade sell-off triggered by the Japanese yen and U.S. dollar could keep the market down, as it swiftly recovered a couple of days later. Not even NVIDIA Co. (NASDAQ: NVDA) saw lower price action after earnings, which gave bears a break. Never bet against the trend or fight the Federal Reserve (the Fed).

As interest rate cuts could be around the corner, which the CME’s FedWatch tool now predicts will be here by September 2024, there are a few stocks that investors should watch closely to match a bullish bias on today’s market. Some of these have to do with the consumer staples sector, and another is a vital player in the technology sector, but one thing they do have in common is that they are likely to do well no matter what the market does next.

Making this list of upside potential with lower risk profiles is Boeing Co. (NYSE: BA), healthcare provider UnitedHealth Group Inc. (NYSE: UNH), overlaid with software and cloud giant Microsoft Co. (NASDAQ: MSFT). Keeping a bullish bias on the market, here’s why these companies could be likely to shake off any volatility that may come up during the next few quarters and bring investors additional growth and upside.

Travel Growth Fueled by Rate Cuts: Boeing Analysts Take Notice

Despite the recent drama regarding Boeing airplanes, Wall Street analysts still have one big fact to face. Boeing’s demand won’t be coming down any time soon, even though the company is in the middle of fixing its manufacturing process to avoid further incidents and malfunctions.

With interest rates coming in the near term, consumers are probably going to push up pent-up demand for travel. According to the Transportation Security Administration (TSA), the United States has seen a recent surge in travelers, reporting record after record of daily travel volume.

Even as most consumers are choked by inflation, travel is still alive, and as long as that is the case, demand for Boeing aircraft will be okay. This is why Wall Street analysts still forecast earnings per share (EPS) to go from a loss of $4.26 to a net profit of $3.42 in 12 months,

This fast growth and swing into profitability made it easier for those at the UBS Group to place a price target of up to $240 a share for this stock, daring it to rally by as much as 38.2% from where it trades today. However, these analysts weren’t the only ones on Wall Street who showed a bullish bias against Boeing.

Of the $8.9 billion of institutional capital that made its way into Boeing stock over the past 12 months, those at Newport Trust Company boosted their stake by 1.2% as of August 2024, bringing their net investment up to $5.8 billion today.

With Government Medicare Entitlements Rising, UnitedHealth Has Room to Grow

According to USA Facts, the federal government spent about $848.2 billion on Medicare programs, which was roughly 14% of total federal spending. Another $839 billion went into Medicaid, bringing the healthcare entitlement spending over $1.6 trillion for last year alone.

This means good news for stocks like UnitedHealth. As more and more people qualify for these programs, their revenues and fees for connecting entitlements to services rise as well. Being a health insurance company has a double benefit.

With interest rate cuts potentially comes another period of inflation, which insurance companies profit from as they can freely raise prices to keep up and outpace overall inflation.

Warren Buffett hopped on this trend as he recently bought into Chubb Ltd. (NYSE: CB).

Wall Street analysts expect UnitedHealth to grow its earnings by up to 12.8% during the next 12 months, which is optimistic for an insurance company. The UBS Group took the lead on this one as well, seeing a valuation of up to $680 a share and calling for a net upside of 15.2%.

Rising Inflation and Costs Drive Demand for Microsoft’s Cloud Services to Boost Margins

As inflation continues to run and rate cuts could bring back another inflationary cycle higher than today’s, businesses understand the importance of achieving economies of scale at little to no cost. This is where the cloud and artificial intelligence come into play.

Microsoft offers these services through its flagship office products. Still, there is also a new wave of development in cloud applications for businesses of every kind. Microsoft Azure enables businesses to streamline their operations with little additional cost; in fact, it lets them cut unnecessary costs through innovation.

Seeing the writing on the wall, analysts now forecast up to 15.2% EPS growth for the software giant. Those at Wedbush see a valuation of $550 a share for Microsoft stock, calling for it to rally by 31.8% from where it trades today. More than that, bears have also started to retreat ahead of the new business wave.

Microsoft stock’s short interest declined by as much as 5.2% in the past month, showing bearish capitulation.

This leaves room for both institutional and retail investors to pick up where they left off.

Exposed: 3 CENT Crypto to Explode September 23rd?

Chris Rowe – the man who recommended Amazon in 1998… Bitcoin and Ethereum in 2017…

And has spotted 44 different coins that have returned over 100%...

Today, he is now making the biggest crypto call of his ENTIRE career…

3 Undervalued Stocks That Are Surprisingly Cheap Right Now

When investors face the current volatility and uncertainty in the stock market, it might be hard to keep a cool head and stay away from the sell button. However, this is precisely when they should scour the market for better opportunities and deals. Keeping the fundamentals front and center will always help performance, especially when everyone gets scared.

Three stocks stand out to reassure investors of good discounts on companies with solid fundamentals, even after the nontraditional leader, NVIDIA Co. (NASDAQ: NVDA), failed to reach a new all-time high and give the S&P 500 another leg higher. Making this list is consumer discretionary, arguably more of a staples play, stock Advance Auto Parts Inc. (NYSE: AAP). Along with this name is a payments platform play in the technology sector set to deliver upside, PayPal Holdings Inc. (NASDAQ: PYPL).

To finish this list, value investors can only go with a healthy amount of contrarianism. Most of the market is against investing in Chinese stocks, quoting risks that existed long before stock prices came down, making them an unjustified way to view this emerging market. Backed by some of the U.S.'s best mega investors, Alibaba Group (NYSE: BABA) is a cheap stock that shouldn't be.

Vehicle Market Cycle Could Propel Advance Auto Parts to New Highs

As of July 2024, a report by The Drive shows that vehicle repossessions in the United States have increased by up to 23% from the same period in 2023. As the consumer begins to feel the thinning effects of inflation, nonemergency items like car payments start being replaced by everyday necessities like food and shelter.

This is why the new car market might be in trouble in the coming quarters, but that also spells good news for the used car market. If people cannot trade their used car for a new one, then there is still a constant that will happen with their current vehicles, and that is parts and maintenance.

That’s where Advance Auto Parts comes into play and why Wall Street analysts expect to see up to 53.5% earnings per share (EPS) growth for the stock in the next 12 months.

More than that, those at Evercore have leaned on this momentum to place a price target of up to $60 a share on the stock.

Advance Auto Parts would have to rally by as much as 32.4% from where it trades today to prove these valuations right. The company’s financials show a gross margin of over 39%, which speaks volumes of where the upside in the stock could come from, as management can retain more capital on hand to reinvest into further growth.

Interest Rate Cuts Could Drive PayPal Stock Growth Beyond Expectations

The Fed has started to print money again, as the M2 money supply in the United States is expanding again on an annual basis. Its balance sheet is also beginning to grow as assets are bought. This is English for more liquidity hitting the market in the coming quarters.

This is good for stocks like PayPal, as more money flows through the economy and lower interest rates boost small business activity, which is one of PayPal’s main user bases. Knowing that all of this upside and tailwinds are blowing behind the company, management did the unthinkable.

Projecting up to $5 billion in free cash flow (operating cash flow minus capital expenditures) is one thing, but promising to use 100% of this free cash flow for stock buybacks is another optimistic case entirely.

This buyback is more aggressive today than ever, representing roughly 7% of the company’s market capitalization.

This has helped Wall Street analysts land on a forecast for 10.6% EPS growth in the next 12 months for PayPal stock and giving those at Mizuho the confidence to place a $90 price target on PayPal stock, calling for up to 24.3% upside from where the stock trades today.

A Contrarian Bet on Alibaba: Could It Be the Best Play in China?

Michael Burry is only one of the mega investors betting on China’s recovery. Ray Dalio, manager of the world’s largest hedge fund, has also been allocating capital into the iShares MSCI China ETF (NASDAQ: MCHI) since the fourth quarter of 2023.

Realizing that Alibaba has tapped into the data centers of the world’s fastest-growing middle classes is one bull case. Still, the main case lies in its ownership of the Chinese retail and wholesale market, which is starting to show signs of recovery after the government's repeated waves of stimulus measures.

Positive – and rising – inflation in China for every month of 2024 helps build the case for management to approve a buyback program as big as $25 billion.

Looking to buy back up to 13% of the company’s market capitalization is as bullish a view as it gets.

This is why analysts at Susquehanna see the stock trading as high as $130 for their initial price target, calling for up to 56% upside from where it trades today. Considering the stock made an all-time high of over $300 a share during the low interest rate cycle of 2020-2021, investors could believe there is much more to have over these current price targets.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 3 Must-Own Stocks for Bullish Investors in Today's Market"

Post a Comment