Ticker Reports for January 10th

3 EV Stocks Offering Unique Alternatives to Tesla

Tesla Inc. (NASDAQ: TSLA) has had an incredible stock run, climbing by more than 68% in the last year and an incredible 1,139% in the last five years as of January 9, 2025. The electric car giant remains the largest auto manufacturer worldwide by market cap—at $1.24 trillion, it is about five times as large as the next-biggest automotive company.

Despite this massive success, there are plenty of reasons investors may have recently soured on Tesla. A growing number of Wall Street analysts are rating TSLA either Sell or Hold on the calculation that shares have become overvalued; the consensus price target of around $293 is more than 25% below current levels as of January 9. 2024 deliveries of Tesla vehicles fell by more than 2% year-over-year, the first time this figure has dropped in that timeframe and a significant concern for a company that has previously aimed for a 50% annual deliveries growth rate. And high-profile incidents related to the company—a New Year's Day explosion of a Cybertruck in Las Vegas in a possible act of terrorism and the increasingly polarizing political behavior of CEO Elon Musk—may also be driving investors elsewhere.

Fortunately, EV alternatives, including Li Auto Inc. (NASDAQ: LI), Rivian Automotive Inc. (NASDAQ: RIVN), and NIO Inc. (NYSE: NIO), give investors looking beyond Tesla many good options.

Li Auto: Targeting the Budget-Friendly EV Market

While Tesla shares have skyrocketed in recent months, Chinese EV maker Li Auto has headed the opposite direction—shares of LI are down nearly 30% in the year leading to January 9, 2025. The EV market in China more broadly struggled in 2024 in the face of numerous headwinds, including lagging demand, a high-intensity price war, and concern about the impact of regulations on the industry.

On the other hand, Li has also moved in the opposite direction of Tesla when it comes to vehicle deliveries, with a new record of more than half a million vehicles sold in 2024 and a 16.2% year-over-year increase in vehicles delivered in December. Li made moves to target the budget-friendly end of the EV market with its L6 model, the most affordable of its vehicles. The firm also improved its autonomous driving system to include highway and city driving capabilities, helping it stand out in a crowded space.

While LI shares remain a Hold based on analyst ratings, the consensus price target for the stock comes in at $33.94, more than 46% ahead of where shares currently trade.

Rivian Automotive: Impressive Fourth Quarter, Shortage Resolved

Shares of American EV firm Rivian are down about 26% in the last year, but they spiked by about 15% in early January 2025 after the company announced better-than-expected fourth-quarter delivery figures. The 14,183 vehicles Rivian delivered in the last quarter of 2024 was more than 5% above consensus estimates across Wall Street and a 42% improvement over the prior quarter.

Two other important factors signal that Rivian may be off to a good start in 2025: first, the impressive delivery figure came during a time of year that is typically lower than usual in terms of EV deliveries, making it even more notable; and second, Rivian announced at the same time that its component shortage that began in October has been resolved. This should free the company up to produce all of its models at a regular pace heading into 2025 and should allow its partnership with Volkswagen—Rivian will provide software for upcoming Volkswagen EVs—to continue uninterrupted as well.

Analysts are cautiously optimistic about Rivian shares, with 10 out of 25 across Wall Street rating the firm a Buy.

NIO: Notable End-of-Year Deliveries

Like Li and Rivian, NIO shares have also been down in the last year—a plunge of nearly 43% sent the stock well below $5. However, NIO's more than 31,000 vehicles delivered in December, an increase of 73% year-over-year, are a bright spot for the company.

While Li may be focusing on the budget end of the EV market, NIO has plans to expand across the spectrum. Its budget-friendly Onvo line saw sales roughly double from November to December, and production is expected to continue to scale up going forward. NIO is also launching new SUVs this year and making headway in the compact EV market with its Firefly line, which analysts expect to boost the company's position in Europe. It's no surprise, then, that analysts see more than 32% of upside potential for NIO shares.

"Fed Proof" Your Bank Account with THESE 4 Simple Steps

Starting as soon as a few months from now, the United States government will make a sweeping change to bank accounts nationwide.

It will give them unprecedented powers to control your bank account.

3 Stocks Leveraging NVIDIA's Strength for Profits

NVIDIA (NASDAQ: NVDA) is the most important stock in the market but not the only one benefiting from AI or its advances. Peripheral businesses like Micron Technology (NASDAQ: MU) and collaborators like Logitech International (NASDAQ: LOGI) and Uber Technologies (NYSE: UBER) are well-positioned. They are positioned to benefit from demand in the first case and advancement of AI in the other, and more importantly, able to capitalize on it.

Why Micron’s HBM3E Technology Leads the Industry

Micron’s HBM3E technology is the best and would be in high demand with or without NVIDIA. HBM3E provides the capacity to run the most advanced cloud applications with better performance and lower power usage than its competitors. It just so happens that NVIDIA’s GPUs and CPUs are central to the rise in AI and driving the demand today. That and normalization in legacy markets have Micron’s revenue growing at a hyper pace in 2025 and forecasted to remain robust in the subsequent year. Among the critical details is the margin, which is widening due to strength in the higher-margin next-gen end-markets and revenue leverage.

The consensus estimates for 2025 and 2026 rose at the end of 2024 but are likely low due to the demand and ramping capacity. The company is expanding its HBM footprint with a $7 billion facility expected to commence operations in early 2026, and other links in the AI supply chain are doing likewise. Taiwan Semiconductor is ramping capacity in several locations, increasing its capacity outlook while paving a path to onshoring production of NVIDIA’s most advanced technology. Regarding the price targets, analysts' consensus reported by MarketBeat forecasts this stock to trade near $135 or 35% upside from early January trading levels.

Uber and NVIDIA Aim to Disrupt the Autonomous Vehicle Industry

Uber and NVIDIA are collaborating on a program harnessing Uber’s data generation capability and NVIDIA’s AI computing power to advance autonomous driving. While still a future event, the move to autonomous driving will open new revenue opportunities for this company, allowing it to evolve with technology, and the outlook is bright.

The analysts forecast double-digit growth for Uber over the next few years, with improved earnings quality. The company has already significantly improved its earnings quality, as seen in the 2024 report, and begun aggressive capital returns because of it. Capital returns are expected to continue and possibly strengthen, providing market support at crucial times through buybacks while improving shareholder value.

Analysts like Uber. Not only is coverage rising, but sentiment is firm at Moderate Buy, and the price target is trending higher. The activity is mixed; there were some downgrades and price target reductions in 2024, but the positive outweighs the bad, leaving the consensus target up nearly 60% for the year and 40% above the early January price action.

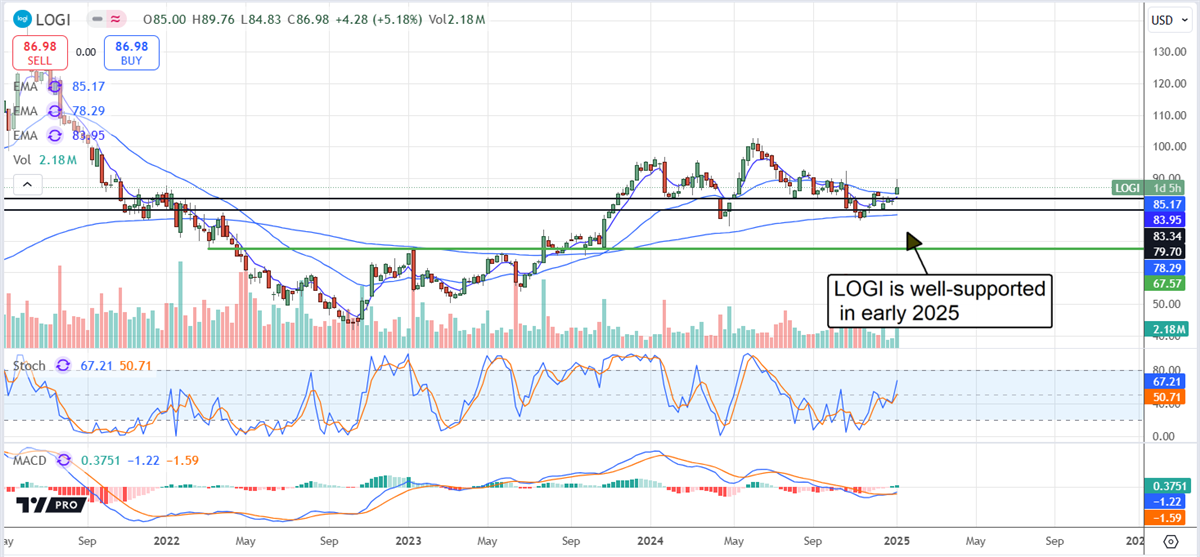

Logitech Advances Streaming Capability: NVIDIA Expands AI Use-Cases

Logitech, NVIDIA, and Inworld AI collaborated on an AI agent for streamers. The tool on G’s Streamworld provides a 3-D assistant that can co-host while automating production. While having a small impact on revenue, the assistant is yet another feature that sets Logitech apart from competitors. Logitech is the leading manufacturer of peripheral devices for computers and services to support them; integrating AI agents into its ecosystem is a natural progression.

Regarding Logitech’s revenue and earnings outlook, the company is expected to sustain growth in 2025 and accelerate it over the next few years. Earnings are forecasted to grow more than 50% by 2030, putting this stock at a 14x valuation and deep-value territory.

Logitech’s dividend is part of its appeal. The stock isn’t a high-yield, but it is competitive, with the S&P 500 running near 1.5% and reliable. The company pays only 25% of its current year earnings outlook and has a solid record of increases. The company has increased its payment at a double-digit CAGR for over a decade and should sustain long-term growth at this pace due to balance sheet health, improving cash flow, and the earnings growth outlook.

He's without a doubt the best stock picker we've ever met.

There are very few people in this world who are considered "the best" in their field.

There are guys like Michael Jordan who is considered the best basketball player of all time…

Or Warren Buffet who is considered the best Investor of all time…

But we've just met a man who might be the best stock picker of all time…

Right now, as we speak, he is currently ranked the #1 stock picker in North America.

Is Domino's Recent Dip a Recipe for Long-Term Gains?

Markets are very rarely efficient, and most hedge fund managers and investors throughout history have proven this. If markets were efficient, then no trader or investor would be able to outperform the market unless they had insane amounts of leverage or access to illegal insider information.

That being said, there is a clear inefficiency in the consumer discretionary sector today, specifically in food and restaurant stocks. Investors should take a deeper look at this inefficiency today and consider closing it down for their own portfolios in 2025 because these sorts of gaps don’t usually last long once the rest of the market—and Wall Street—gets a handle on them.

The price action in shares of Domino’s Pizza Inc. (NASDAQ: DPZ) relative to other pizza chain brands like Papa John’s International Inc. (NASDAQ: PZZA) will bring the prospect of a misprice to investors, one that Wall Street analysts will indeed become aware of in the coming months. Taking a look at the performance of Chipotle Mexican Grill Inc. (NYSE: CMG) can also bring additional evidence of this mispricing opportunity in the affordable food chains space.

Wall Street’s Favorite Metric Has Failed

When analysts and portfolio managers at big banks and hedge funds manage their positions and ideas, they usually weigh the potential outcome in terms of beta. Beta is a measure that determines how volatile a stock is today compared to the S&P 500 index, so a higher beta (above 1.0) means a stock that is more volatile than the market.

The opposite can be said for a beta measure below 1.0, meaning the stock is less volatile and safer than the broader market. With this in mind, investors can see how the differing price actions in these three stocks have failed the basic premise of professional money managers.

With a low beta of 0.90, Domino’s Pizza stock has underperformed Chipotle Mexican Grill stock over the past 12 months by as much as 27%. Yet, considering that Chipotle has a significantly higher beta of 1.3, recent pullbacks in the S&P 500 shouldn’t have been harsher on Domino’s Pizza stock.

While Chipotle stock trades at 85% of its 52-week high, which is considered bullish territory, Domino’s Pizza stock has fallen to only 72% of its 52-week high, which is conversely bearish territory for the company. It almost seems like the heavy underperformance in Papa John’s stock might have dragged Domino’s Pizza down by association, and if that’s the case, then investors should get excited.

The Difference Maker for Domino’s Pizza Stock

Of course, it is a correlation selloff because neither the beta nor the fundamentals between Domino’s Pizza stock and Papa John’s would suggest that Domino’s should be trading this low compared to its 52-week high price. There is one main difference maker in the stock, a financial metric, that investors should be aware of in Domino’s Pizza stock today.

That metric is the return on invested capital (ROIC) rate, which is responsible for compounding itself and creating the sort of “I wish I had bought " reaction when investors look at a stock's long-term price chart. With an ROIC of over 61%, Domino’s Pizza sock fits that description perfectly.

Compared to Papa John’s ROIC of roughly 31%, it would seem that a correlation selloff might not be justified after all. Recently, some on Wall Street have become aware of this inefficiency and decided to take matters into their own hands, such as those from FMR LLC, who boosted their positions in the company by 16.3% as of November 2024.

This new allocation would net their position at a high of $941.9 million today, or 6.3% ownership in the company. Acting as another bullish gauge for investors to consider Domino’s Pizza a potential buy in this recent pullback, there’s also much more evidence to keep track of.

Analysts from Loop Capital also held a Buy rating on the company as of November 2024, this time boosting their valuations to a high of $559 a share to call for a net upside of 35.4% from where the stock trades today. This bold call is not only born out of the inefficiencies pointed out above but also from the stock’s outstanding discount.

Compared to the retail sector’s average 98.4x price-to-earnings (P/E) valuation, Domino’s Pizza offers a significant discount through its 25.4x multiple today, which is also severely compressed compared to its long-term average valuation of 35.0x.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 3 Stocks Leveraging NVIDIA’s Strength for Profits"

Post a Comment