Ticker Reports for January 6th

Build-Your-Bowl Battle: CAVA, Chipotle, and Sweetgreen Face Off

Fast food and dine-in restaurants struggled in 2024 as inflationary pressure caused consumers to tighten their spending habits in 2024. However, “build-your-bowl” (BYB) format fast casual restaurants in the retail/wholesale sector had a stellar year. These types of restaurants had an almost elastic halo around them, as their higher prices didn't stop consumers from spending. The addition of steak and beef to their menus also bolstered revenues. Heading into 2025, investors are curious to see if the spending trend continues for the top three BYB fast-casual restaurants. Here's how they performed in their recent results and what it bodes for their future results. Is there a clear winner that is outpacing the rest? Yes.

CAVA: The Mediterranean Chipotle Continues to Break Records

With shares rising 189% in 2024, CAVA Group Inc. (NYSE: CAVA) made a huge splash with investors and consumers. The restaurant offers a healthier option for its bowls with proteins ranging from grilled chicken, lamb meatballs, falafels to steak, along with 38 fresh Mediterranean toppings like pickled cabbage slaw, roasted eggplant, feta cheese, hummus and sauces like tzatziki, spicy mayo, harissa, and lemon herb tahini. There are 17 billion potential combinations. Customers can also order their meals in pita sandwiches. The company has grown to over 350 locations, with plans to open 56 to 58 new locations in 2024.

Firing on All Pistons to Take the Crown With 18.1% YoY Comps Growth

CAVA reported Q3 2024 EPS of 15 cents, beating analyst estimates by 4 cents. Revenues surged 39% year-over-year (YoY) to $243.82 million, beating consensus estimates for $233.05 million. Its same restaurant sales comps rose 18.1% YoY as guest traffic surged 12.9% YoY. While around a 5.2% increase came from menu pricing and product mix, the surge in guest traffic is a solid sign of organic growth. Restaurant-level profit margin rose to 25.6%. Average unit volume (AUV) rose to $2.8 million. The company seeks to enter the South Florida and Midwest markets in 2025. The Mediterranean could be the next major cultural cuisine category.

CAVA Issues In-Line 2024 Revenue But Raises Comps and Margin Guidance

Incidentally, CAVA appears to have taken a conservative approach to forecasts, with full-year revenue expected between $675 million and $680 million versus $678.56 million consensus estimates. CAVA raised its guidance for sales-store sales comps to between 12% and 13%, up from 8.5% to 9.5%. CAVA raised its restaurant-level profit margin forecast to 24.5% to 25%, up from 24.2% to 24.7%.

Sidestepping the FOMO

While the results were spectacular, it's important not to rush in head first on the stock. FOMO investors found that out the hard way after earnings. Shares shot up as high as $172.43 the following morning from $145.03, only to "sell the news" after the price gap fell to a low of $133.00 several days later.

Was the profit-taking justified on a 200% run-up? Insiders thought so, as top executives unloaded shares shortly afterward. The stock still trades around the $115.08 level with a P/E of 250 but near its $110.00 pre-earnings support level, which is much cheaper than the $172.43 peak that someone bought the day after earnings.

Chipotle: The Incumbent Grinds Along While Comps Slow Down

The incumbent and trailblazer of the BYB-style fast casual restaurant model Chipotle Mexican Grill Inc. (NYSE: CMG) made big headlines when its iconic CEO Brian Niccol was poached by Starbucks Co. (NYSE: SBUX) for over $100 million in total compensation.

The company scored double-digit comps in its previous quarter with the limited-time Chicken Pastor. However, that momentum has slowed as the company reported Q3 2024 revenue growth of 13% YoY to $2.79 billion, falling short of the $2.82 billion consensus estimates. Comp restaurant sales growth also fell by nearly half sequentially to just 6%. The company says Smoked brisket drove another quarter of strong results.

Chipotle Reaffirms Guidance and Gains More Chipotlanes

Chipotle reaffirmed full 2024 comp guidance of mid to high-single digits. It reaffirmed the outlook for full-year 2024 company-operated restaurant openings of 285 to 315 units. For 2025, Chipotle expected 315 to 345 new company-operated restaurant openings, with over 80% having drive-thru Chipotlanes.

Sweetgreen: Sweet Growth But Sour Profits

Health-conscious BYB newcomer Sweetgreen Inc. (NYSE: SG) had a stellar 2024, with shares rising 220%. The addition of caramelized garlic steak was a game changer as it widened its audience beyond vegetarians. Its caramelized garlic steak quickly grew in popularity as it was selected in one out of every five dinner orders. After coming off a stellar Q2 2024, momentum has slowed down.

Sweet Green posted a Q3 2024 EPS loss of 18 cents, missing estimates by 5 cents. Revenues rose 13% YoY to $173.43 million, missing the consensus estimates of $175.46 million. Same-store sales comps rose 6% YoY, up from 4% the prior year. Restaurant-level profit was $34.9 million, and restaurant-level profit margin was 20.2%, which was an improvement from the prior quarter of $29.1 million and 19%, respectively.

Sweetgreen Issues In-Line Guidance

The company expects full-year 2024 revenues of $675 million to $680 million versus $678.56 million. Same-store sales growth is expected to be between 6% and 7%. Restaurant-level profit margin is expected to be between 19.5% and 20%.

Sweetgreen Co-CEO Johnathan Newman commented, "Our expanded menu, together with the performance of our 2024 class of new restaurant openings, growth in emerging markets and our successful deployment of the Infinite Kitchen, gives us confidence in the reacceleration of our 2025 unit growth."

"Fed Proof" Your Bank Account with THESE 4 Simple Steps

Starting as soon as a few months from now, the United States government will make a sweeping change to bank accounts nationwide.

It will give them unprecedented powers to control your bank account.

Insiders Are Loading Up: 3 Key Stock Picks for Investors

This is where today’s list of insider buying activity comes into play, as investors can reverse engineer the reasoning behind these bigger firms buying into a stock and, if justifiable enough, get some for themselves. This might ensure that their portfolios kick off the new year with a bang, leaving plenty of room to keep up the momentum for the remainder of the year.

Stocks like Nike Inc. (NYSE: NKE), FedEx Co. (NYSE: FDX), and even Occidental Petroleum Co. (NYSE: OXY) have all caught the attention of institutional buyers and investors recently. It looks like Wall Street analysts are aligned with the fundamental stories behind these companies, which are strong enough to justify double-digit upside in the coming months.

Nike Stock’s Dip: A Rare Opportunity

It isn’t often that blue-chip stocks like Nike come to trade at such low levels, even if the stock is in the highly cyclical consumer discretionary sector. After a few controversial quarters, showing some weakness in their Chinese branches, Nike stock has sold off to a low of 68% of its 52-week high.

The slowing overseas numbers may have partly justified this discount. Still, at this point, most in the market can agree that it has been largely overdone. Leading this school of thought is billionaire value investor Bill Ackman, who has accumulated a stake of up to 3 million shares in Nike stock.

With a multi-million dollar position, Ackman is betting that the company’s international exposure and brand recognition will not only help the stock get back on its feet and command a premium for its presence but also mitigate most—if not all—risks associated with a potential downturn in the economy.

Wall Street analysts, particularly those from Robert W. Baird, decided to share the optimism for Nike stock as of December 2024. With an outperformed rating on the stock, their new $105 a share price target shows a net upside potential of as much as 43.2% from where the stock trades today.

Business Activity, Delivered by FedEx Stock

Though FedEx stock doesn’t offer as much discount as Nike, at 87% of its 52-week high, it still carries enough upside to attract insider buying activity lately. Leading the pack in buying, those from State Street decided to accumulate up to $2.6 billion worth of FedEx stock, or 3.8% ownership in the company.

Knowing that, as the Federal Reserve (the Fed) cuts interest rates, business activity will likely begin to pick up again. Amongst the many industries that can benefit from this shift, the transportation sector is at the heart of most businesses and their needs when it comes to transportation. This is where the appeal in FedEx stock comes in.

Wall Street analysts would agree with this theme, as those from J.P. Morgan Chase decided to reiterate their overweight rating on the stock, this time keeping a $370 valuation on it. To prove these new targets right, FedEx stock would have to stage a rally of up to 35% from today’s prices, justifying the recent purchases by these institutions.

Warren Buffett Is Back at It Again With OXY

Following the increased business activity theme, investors shouldn’t be surprised to see renewed optimism around the energy sector. This time, however, the confirmation couldn’t be stronger. Warren Buffett has decided to buy up to 29% of Occidental Petroleum stock, and these metrics would back his decision.

First, the stock trades at a significant discount on a price-to-book (P/B) basis today. Compared to the energy sector’s average 3.6x valuation, Occidental Petroleum stock’s 2.0x multiple gives Buffett just the sort of discount he’s famous for going after and one that investors shouldn’t ignore today.

As the stock now sits at 71% of its 52-week high, price targets become more valuable than ever before; for example, Mizuho analysts now see a fair valuation for the stock at a high of $70 a share. This view would dare the stock to rally by as much as 38.6% from where it trades today, another home run for investors to score this year.

Why we call THIS the "60-Second Trade"

Ever heard of the "60-Second Trade"?

It's a unique cash flow strategy that lets regular traders target anywhere from $100 to a couple of thousand in extra cash flow in as little as 7 days…

In on Monday, out on Friday!

How Cigna Remains at the Top of the Health Insurance Food Chain

The health insurance industry has received a lot of backlash over its managed care practices that bog down providers with pre-authorizations and rampant medical claim denials. The rise in medical benefits ratios (MBRs) driven by Medicare Advantage plans have squeezed margins for major health insurance providers like Humana Inc. (NYSE: HUM), UnitedHealth Group Inc. (NYSE: UNH), and CVS Health Co. (NYSE: CVS). However, one major insurer saw the writing on the wall early on and divested its Medicare Advantage business to protect its margins.

The Cigna Group Inc. (NYSE: CI) is at the top of the health insurer food chain. The company has demonstrated its foresight and agility to quickly navigate the changing landscape of the healthcare industry within the medical sector.

How Cigna Masterfully Navigates the Trends in Healthcare

Cigna has skillfully bobbed and weaved its way around the healthcare landscape, jumping on trends ahead of time and sidestepping potholes along the way. They jump-started their Medicare Advantage (MA) gravy train in 2011, acquiring HealthSpring Inc. for $3.8 billion to pump up its MA membership from 46,000 to 400,000 members.

For over a decade, Cigna scored billions from MA until their spider senses kicked in. They saw the writing on the wall and exited when the inpatient utilization rates started climbing, selling its Medicare Advantage business (along with its Medicare Part D and Cigna Supplemental Benefits business) for $3.3 billion to Health Care Service Corporation (a major non-profit health insurer offering Blue Cross Blue Shield plans) in January of 2024. This is why the rumors of Cigna acquiring Humana made no sense, as they would be reentering the MA market, which it had just exited.

Cigna entered the lucrative pharmacy benefits management (PBM) business with its $67 billion acquisition of Express Scripts in December 2018. By doing so, it also acquired EviCore, a third-party medical benefits management (MBM) and utilization firm. EviCore is often outsourced by insurance carriers to use data analytics and artificial intelligence (AI) powered intellipath solutions to handle pre-authorization and claims management services, ensuring that treatments are medically necessary. Critics suggest EviCore is more of a way to outsource claim denials and shift responsibility onto a "neutral" third party. They are allegedly hired to automate claim denials and prolong the pre-authorization process in order to boost margins for their health insurance clients.

U.S. Healthcare Spending Surges 7.5% in 2023

According to the Centers for Medicare & Medicaid Services, its national health expenditure (NHE) data indicates healthcare spending in the United States grew 7.5% YoY in 2023 to $4.9 trillion or $14,570 per person, accounting for 17.6% of gross domestic product (GDP). Private health insurance spending rose 11.5% YoY. For 2023 to 2032, NHE is forecast to grow 5.6%, outpacing average GDP growth of 4.3%. Spending on healthcare will continue to outpace inflation.

This ensures healthcare is a growth industry, and metaphorically speaking, Cigna may be the nicest house in a rough neighborhood.

Evernorth’s 50% Revenue Growth Drives Cigna’s 30% YoY Revenue Growth in Q3 2024

Cigna operates in two divisions: Evernorth Health Services and Cigna Healthcare. Evernorth operates PBM, specialty pharmacy, and care delivery and management (EviCore) business. Cigna Healthcare is an insurance business offering traditional health insurance plans. Cigna reported Q3 EPS of $7.51, beating analyst estimates by 28 cents. Revenues rose a whopping 30% YoY to $63.7 billion, crushing the $59.58 billion consensus estimates by over $4 billion.

Cigna’s Medical Care Ratio is Still One of the Highest in the Industry Compared to Peers

The medical care ratio (MCR) is the percentage of insurance premiums that are actually spent on medical care for its members. The higher the MCR, the less money the insurer makes. Cigna’s medical MCR was 82.8%, up from 80.5% in the prior year, but hugely better than competitor CVS’s MCR, which rose to 95.2% in its Q3 2024. Again, this illustrates how Cigna protected its MCR by selling its MA business while CVS's MCR surged to 95.2% (up from 85.7% the year before) by keeping its MA business, further demonstrating skillful agility by Cigna.

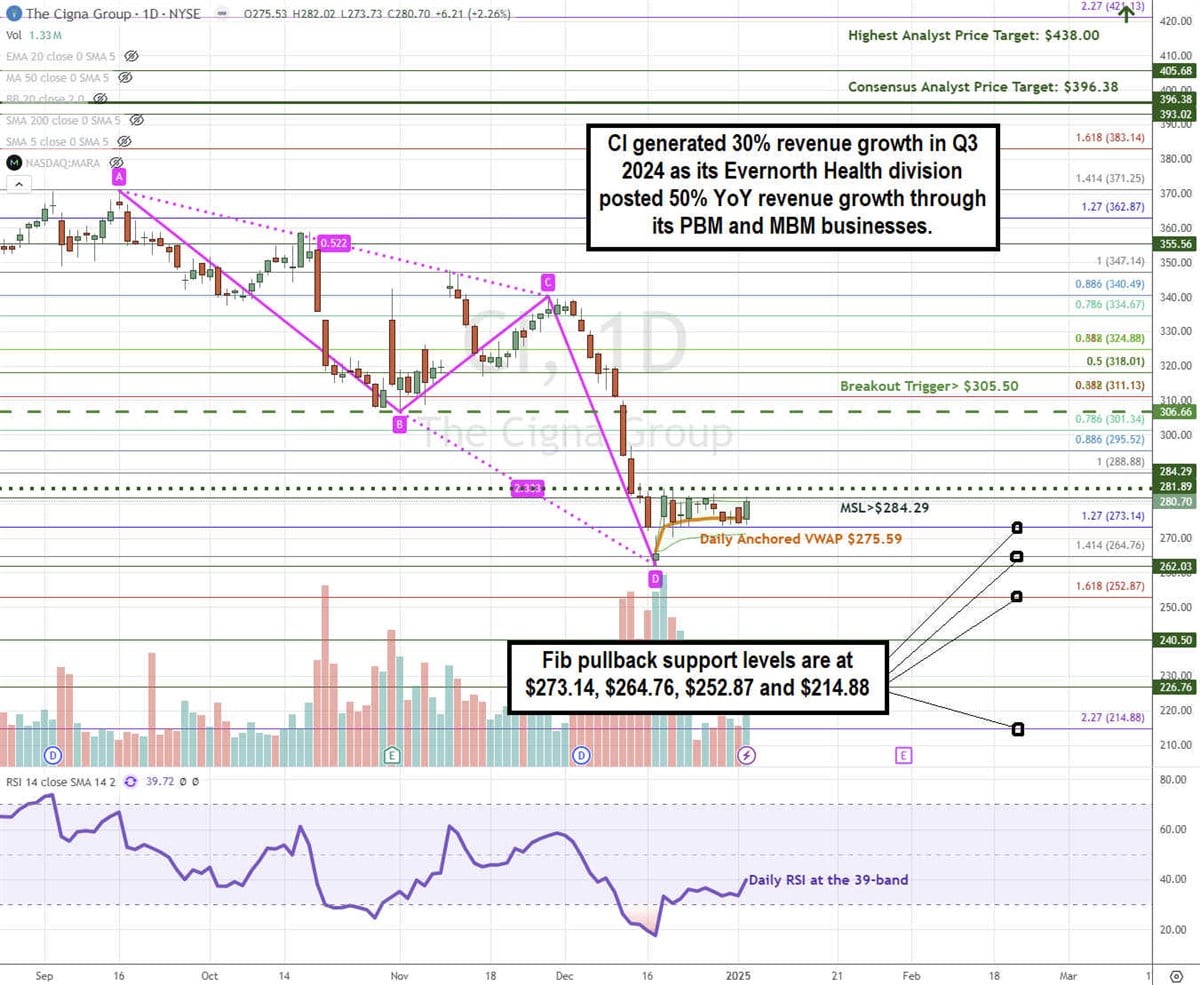

CI’s average consensus price target is $395.93, implying a 41.31% upside, and its highest analyst price target sits at $438.00. It has 13 analysts' Buy ratings and one Hold rating. The stock has a 1.69% short interest.

CI Forms a Potential ABCD Reversal Pattern

An ABCD reversal is a harmonic pattern comprised of four key points: A swing high, B bottom reversal, C peak, and D lower bottom reversal level. The reversal triggers when the stock bounces back up through point B.

CI formed the ABCD pattern comprised of a low and lower low that found support at the $273.14 Fib. The daily anchored VWAP is attempting to hold support at the $273.14 Fib as CI attempts to trigger a market structure low (MSL) buy signal above $284.29. The ABCD reversal breakout triggers above the $306.66 level. The daily RSI is starting to bounce at the 39-band. Fibonacci (Fib) pullback support levels are at $273.14, $264.76, $252.87, and $214.88.

Actionable Options Strategies: Bullish investors can consider using cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, writing covered calls at upside Fib levels executes a wheel strategy for income on top of its 2.00% dividend yield.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Insiders Are Loading Up: 3 Key Stock Picks for Investors"

Post a Comment