Ticker Reports for January 3rd

Rivian Defies Doubters: Delivery Triumph Fuels Stock Surge

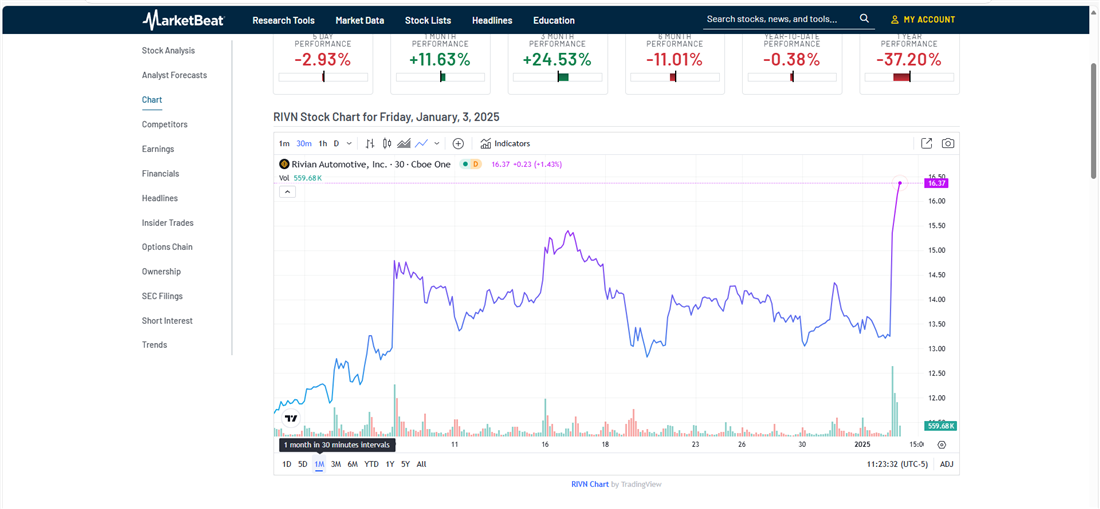

Rivian Automotive Inc. (NASDAQ: RIVN) stock is up more than 15% the morning after the company announced fourth-quarter deliveries that came in well above analysts’ estimates.

Better still, the electric vehicle (EV) manufacturer announced that it is no longer experiencing a component shortage that was limiting production for select models.

The company announced total deliveries of 14,183 vehicles for the three months ending on December 31, 2024. Here’s some context around those numbers:

-

The consensus among 15 analysts was for 13,472 vehicle deliveries.

-

The number was 42% higher than the prior quarter and the highest delivery number in over a year for the EV maker.

-

It came in a quarter that is historically lighter as Rivian’s largest customer, Amazon.com Inc. (NASDAQ: AMZN) is typically scaling back deliveries.

Rivian first reported the component shortage with its third-quarter delivery numbers in October. The shortage affected parts the company used in its R1 SUV, R1T pickup trucks, and delivery vans.

At that time, the company lowered its annual production target, and RIVN stock, which had been trading at around $18.11 in July 2024, was cut nearly in half by the beginning of November.

However, with this key constraint on production removed, analysts will now be looking for Rivian to prove that it can become a profitable company. Keep in mind that despite beating estimates for vehicles it manufactured in the fourth quarter, Rivian still came in light on full-year deliveries by about 13%. This was reflected in the company’s revenue which came in sharply lower on a year-over-year basis.

That said, the 49,476 vehicles it manufactured were above its revised forecast of between 47,000 and 49,000 vehicles.

A Key Step Towards Profitability

After hitting a 52-week low in November, RIVN stock has been on the rise after it announced a $5.8 billion joint venture with Volkswagen (OTCMKTS: VWAGY). Under the terms of the agreement, Volkswagen will use Rivian’s software in its coming EVs. Investors were enthusiastic about how this additional revenue stream, which is less capital intensive and, therefore, more profitable, would push the company towards profitability.

However, for the company to achieve sustained profitability, it will have to show that it can build EVs in a cost-effective manner. The company is not likely to answer that question until it releases its new models with lower material costs in 2026.

In the meantime, analysts will be looking for Rivian to raise its delivery outlook for fiscal year 2025. An analyst from Truist Financial remarked, “...the focus will now be on RIVN’s ability to execute on its path toward profitability as we see only modest YoY growth in FY25 ahead of the company’s planned 2026 R2 launch at Normal.” Truist reiterated its Hold rating on RIVN stock in October and lowered its price target from $16 to $12.

Does the Breakout Have Legs?

A 15% rally in RIVN stock is impressive, particularly since it’s occurring with high trading volume. On the morning of January 3, trading volume in RIVN stock was approximately 40% higher than the average.

But at a time when all automotive stocks are under pressure, should you chase the stock higher? If you’re a trader, you’ll note that RIVN stock continues to carry a high short interest of nearly 19%. Those short positions will be under pressure, which could mean the stock still has a little higher to run.

However, if you’re thinking about a long position, some caution may be necessary. At $15.74 per share, RIVN is now at a level of resistance it met in mid-December 2024. It’s also consistent with the current options chain for February 2025.

With the stock now slightly above analysts' consensus price target, now may be a time to wait for a better entry point. As of midday trading on January 3, analysts had not responded to the company’s news.

That could come when Rivian reports earnings in February. At that point, analysts will look for confirmation that the company is indeed moving closer to profitability.

"Fed Proof" Your Bank Account with THESE 4 Simple Steps

Starting as soon as a few months from now, the United States government will make a sweeping change to bank accounts nationwide.

It will give them unprecedented powers to control your bank account.

Hindenburg Short Report Slams Carvana Over Alleged 'Grift'

Polarizing activist short-seller Hindenburg Research—known for its bombshell reports alleging corporate fraud and other malfeasance by companies including Nikola Corp. (NASDAQ: NKLA) and India's Adani Group—published on January 2, 2025, an article about its latest target: Carvana Co. (NYSE: CVNA).

In the report, Hindenburg alleges that the $44-billion online car dealer's stock spike of 284% throughout 2024, which some investors have hailed as a major turnaround following bankruptcy scares in 2022 and 2023, is a "mirage." At the core of Hindenburg's report is an allegation that Carvana engaged in accounting manipulation and lax loan underwriting to give the appearance of income growth in recent quarters. As is its custom, Hindenburg also announced at the time of the report's release that it had entered a short position of undisclosed size in CVNA shares.

Allegations of Suspicious Loan Sales and Inflated Top- and Bottom-Line Performance

Hindenburg claims to have identified $800 million in loan sales to a "suspected undisclosed related party" as Carvana's prior purchase commitment agreement with Ally Financial has changed in ways not entirely clear to outsiders in recent years. Carvana sold $3.6 billion of vehicle loans to Ally in 2023, representing about 60% of its total originations. However, sales to Ally dwindled throughout the first three quarters of 2024 to roughly 35% of Carvana's originations, or $2.2 billion, for that period.

Hindenburg's report suggests that the unnamed buyer of an additional $800 million in loans in the first quarters of 2024 is likely a trust affiliated with Cerberus Capital—that company's Chairman of Global Investments, Dan Quayle, is a Carvana Director.

Further, Hindenburg claims that Carvana's model focuses on non-prime and subprime loans and that its "toxic loan book is a result of lax underwriting standards," resulting in more than $15.4 billion in asset-backed securities that the car dealer has issued. The report also suggests that 60-day delinquencies across Carvana's borrowers are more than four times the industry average.

The report alleges Carvana has used accounting "games" to give the appearance of stronger revenue and profit performance. These include the use of borrower extensions to avoid loan delinquencies and a range of manipulations using DriveTime (a dealership run by the father of Carvana's CEO), including profit-share agreements between the two companies and Carvana's history of offloading costs of extended warranties and even excess inventory to DriveTime. The report also cites a former executive at Carvana who claimed that the company would manipulate income figures by holding loan sales over the quarterly line.

Meanwhile, Hindenburg alleges that Carvana's CEO and his father have timed the market with incredible precision, allowing them to earn billions in sales of Carvana shares.

Valuation and Debt Concerns

Hindenburg's report also indicates potential concerns investors may have about Carvana even without accounting for its alleged "grift." At the time of the report's release, Hindenburg said that Carvana traded at an 845% premium to its peers on a 1-year forward P/S basis and a 754% premium on a 1-year forward P/E basis. The firm had a net debt of $4.8 billion at the end of September 2024, with cash interest payments of $215 million per year due beginning February 2025 based on long-term debt obligations. Further, Carvana's credit rating of B- is the lowest of its peer companies as well.

Carvana: Overview, Business Model, Bankruptcy Fears

Founded in 2012, Carvana is an online car dealer that operates a platform through which individual customers can buy and sell used cars. Activity on this platform makes up the large majority (around 70%) of the company's business by revenue, with other operations including services like insurance, financing, and protection plans. Finally, Carvana operates a wholesale auction business called ADESA. Carvana had its IPO in 2017.

In a recent investor presentation, Carvana noted that its operations cover more than 81% of the U.S. population, with more than 45,000 vehicles available for sale as of September 30, 2024.

Still, the company has fairly recently experienced concerns about potential bankruptcy. In September 2023, for instance, it aimed to trim $1.3 billion in debt as part of a major restructuring effort. This, along with efforts to achieve positive EBITDA and to roughly triple its retail vehicle gross profit per unit from September 2022 to September 2024, likely helped to drive a significant rally in the last several months.

As of January 3, 2025, Carvana had not yet issued a press release addressing Hindenburg's report.

An iconic crypto discovery indeed… check it out

I want to let you in on what may be the hottest crypto discovery of all time…

One that has NOTHING to do with creating a crypto wallet or touching ANY risky coin for that matter.

Instead, it's a way that could let regular folks like you and me target 10X the possible results you'd expect from buying Bitcoin … in just a fraction of the time

It sounds nuts… trust me I know that…

But just as I would hate for you to jump into any risky crypto asset…

That's exactly how I would hate for you to miss out on what could be a safer and better way to benefit from the crypto bull run of 2024.

Which is why I'm giving you an opportunity to get all the details of this iconic crypto discovery with you for the first time ever… completely free…

MicroStrategy Feels Bitcoin's Weight: 2 Smart Dips to Watch

Especially in the way that stocks with heavy Bitcoin or other cryptocurrency holdings in their balance sheets have seen the wildest price action in 2024, such as MicroStrategy Inc. (NASDAQ: MSTR). The stock was a darling of the industry while it was hot, but now that Bitcoin is pulling from its highs, it is being questioned down to 55% of its 52-week high.

While investors might start to fear missing out if they don’t buy that massive dip, other discounted stocks might make better buys today. One example can be made out of Tesla Inc. (NASDAQ: TSLA), as the automotive stock has come down to as low as 77% of its 52-week high, or Advanced Micro Devices Inc. (NASDAQ: AMD) to give investors one of the best discounts in the semiconductor industry at 53% of its 52-week high today.

The Risks Behind MicroStrategy Stock

Even though the stock has traded down to what would otherwise be an attractive level to buy, the business model has some inherent risk. Just as it was responsible for the stock’s success, it might also be responsible for its downfall. The reason is that the core business, based on software, doesn’t make any money.

So, MicroStrategy buys Bitcoin for its balance sheet through ownership dilution. In other words, the company issues shares to the market to fund its leveraged Bitcoin buying spree. While this is great for investors as Bitcoin goes up, the leverage and unsustainability of this machine are also disastrous when the coin comes down.

That is why, even though 55% of its 52-week high is attractive, MicroStrategy's risk-to-reward ratio is just not worth investor capital—nor their time. On that note, these two stocks offer a completely different setup in the first quarter of 2025.

Tesla Stock’s Tailwinds Outweigh MicroStrategy’s Discount

After a tragic explosion involving a Tesla Cybertruck outside a Las Vegas hotel, the stock dropped 6.7% as investors reacted to the alarming incident. Adding to the pressure, Tesla reported its first annual sales decline in over a decade, signaling that the stock is facing significant challenges at the moment.

However, others focused on value would see that Tesla sold over 2 million vehicles in 2024, coming second to only China’s BYD (OTCMKTS: BYDDF). The fact that oil prices are so low right now, dragging gas prices lower, is usually a cyclical tailwind in electric vehicle sales.

Adding to this are the trends in consumer credit, investors have the perfect storm to expect lower Tesla sales. But that ends there. Wall Street analysts, particularly those at Mizuho, still give the stock an Outperform rating as of December 2024, this time along with a valuation of up to $515 a share.

To prove these analysts right, Tesla would have to rally by as much as 36% from its current position. The risks for Tesla stock at these discounts are priced in, giving investors a much better risk-to-reward setup as a potential buy moving forward.

Advanced Micro Devices: The New NVIDIA

Speaking of other stocks taking the podium, Advanced Micro Devices might take over NVIDIA Co. (NASDAQ: NVDA) as the new head of the artificial intelligence race through semiconductor manufacturing. This stock offers not only a price discount but also massive upside from Wall Street analysts.

Today, Advanced Micro Devices stock has a consensus price target of $191.96, which would call for a net upside of as much as 60% from today’s prices. This setup would offer investors a much better view than NVIDIA’s consensus price target of $164.1 a share, which calls for only 20% upside.

Carrying three times the upside, at a fraction of NVIDIA’s relative price action, drew in some institutional investors for Advanced Micro Devices stock recently. Over the past 12 months, up to $19 billion flowed into the company from institutions, but a recent buying spree might be more meaningful for investors.

Those from State Street have decided to boost their Advanced Micro Devices holdings by 2.3% as of November 2024, bringing their net position to a high of $11.5 billion today, or 4.3% ownership in the company.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 MicroStrategy Feels Bitcoin's Weight: 2 Smart Dips to Watch"

Post a Comment