Ticker Reports for January 1st

CarMax Is Firing on All Pistons as Growth Returns

When it comes to used cars in the United States, CarMax Inc. (NYSE: KMX) stands out as the largest used car dealership. The auto/tires/trucks sector giant operates more than 245 physical dealerships in the country, and it popularized the concept of a “no-haggle” pricing policy for buying used cars. The company buys, sells, services and also finances vehicle purchases through its CarMax Auto Finance division, which originates more than $8 billion in receivables annually.

The auto industry has been on a wild rollercoaster ride since 2019, as it saw an unprecedented surge during the pandemic and painful normalization afterward. However, CarMax is starting to reignite growth again following nine straight year-over-year (YoY) quarterly revenue declines. It also reported the widest earnings per share (EPS) beat since the first quarter of 2024.

CarMax has many competitors, from rival giant AutoNation Inc. (NYSE: AN) to Carvana Co. (NYSE: CVNA), local dealerships and online sites like Cars.com (NYSE: CARS ) and CarGurus Inc. (NASDAQ: CARG).

Q3 Marks Commences the Comeback Trail

Investors were treated to an upbeat Q3 2024 earnings report as CarMax earned 81 cents per share, firmly beating consensus estimates by 19 cents. Revenues grew 1.2% YoY to $6.22 billion, also firmly beating $6.15 billion consensus estimates. The positive revenue growth comes after nine straight quarters of YoY declines. This also beat analyst expectations for another YoY declining quarter.

CarMax Auto Finance (CAF) income rose 7.6% YoY to $159.9 million, driven by net interest margin percentage and average managed receivables. The company repurchased $114.8 million of stock in the quarter. Provision for loan losses stabilized in Q3 to $74 million, still up from a year ago at $68 million. This was an improvement over the previous Q2 provision at $113 million, up from $90 million in Q2 2023.

Stable Margins and Positive Revenue Growth Stood Out

Total retail used vehicle sales increased 5.4% YoY to 184,243 units. Comparable store used unit sales rose 4.3% YoY. Total retail used units sold rose 1.2% YoY, driven by the increase in retail used units sold and partially offset by the 3.9% drop in average retail selling price or approximately $1,100 per unit. Retail gross profit rose 1%, averaging $2,306 per unit. Wholesale gross margin rose 5%, averaging $1,015 per unit. Extended protection plans (EPP) margin rose $53 per unit to $573. The service margin grew by $60 per retail unit.

CarMax purchased 270,000 cars from consumers and dealers, up 7.9% YoY. From consumers, they bought 237,000 vehicles, up 4.1%. From dealers, they bought 33,000 vehicles, up 46.7% YoY. Total online sales rose 32% YoY on top of the 31% growth last year. This also includes all wholesale auction sales, which were virtual, representing 19% of total revenue in Q3.

CarMax CEO Bill Nash commented, “I am pleased with the positive momentum that we are driving across our diversified business model. Our solid execution and a more stable environment for vehicle valuations enabled us to deliver robust EPS growth driven by increases in unit sales and buys, solid margins, growth in CAF income, and ongoing management of SG&A.”

KMX Stock Is in an Ascending Triangle Pattern

An ascending triangle is comprised of a flat-top upper trendline resistance converging with an ascending (rising) lower trendline support. The breakout occurs when the stock surges through the upper trendline. If the stock collapses under the lower ascending trendline, then the pattern fails as a breakdown forms.

KMX formed the flat-top upper trendline resistance at $87.57, converging with an ascending lower trendline that formed at the $69.95 swing low. While the lower trendline has been tested and overshot three times, the daily anchored VWAP has been consistently holding support, which is now at $80.18. The flat-top upper trendline almost broke out after earnings until a gap and trap ensued, causing KMX to return to the ascending triangle range. The daily anchored VWAP is at $80.18. The daily RSI is chopping at the 52-band. Fibonacci (Fib) pullback support levels are at $79.67, $74.38, $70.62, and $65.83.

KMX's average consensus price target is $85.17, implying a 1.26% upside and its highest analyst price target sits at $105.00. It has six analysts' Buy ratings, five Hold, and three Sell Ratings. The stock has an 8.61% short interest.

Actionable Options Strategies: Bullish investors can consider implementing cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, then writing covered call at upside Fib levels executes a wheel strategy for income since there is no dividend.

Grab This Altcoin Before Trump's Crypto Announcement

Grab This Altcoin Before Trump's Crypto Announcement

Whatever it is, I expect it to pump the market, which is why I'm recommending ONE coin to all investors right now.

Woodward: Delivering Critical Components for the Aerospace Boom

Woodward Inc. (NASDAQ: WWD) manufactures critical control systems and components for the commercial aviation, industrial, and defense industries. Modern commercial passenger airliners can contain up to five million components, while military aircraft can have up to two million. This aerospace leader supplies essential components, from engine and power systems to sensors and missile guidance, ensuring consistent, non-disrupted performance.

Some of Woodward's high-profile clients include Raytheon Technologies Co. (NYSE: RTX), Caterpillar Inc. (NYSE: CAT), General Electronic (NYSE: GE), Baker Hughes Co. (NASDAQ: BKR), The Boeing Co. (NYSE: BA) and Airbus.

Despite challenges in its industrial segment, Woodward delivered record fiscal 2024 growth driven by strong aerospace sales. The stock is now forming a technical pattern that may indicate potential future price movement, presenting new opportunities for investors.

Record Sales Growth in 2024

Woodward delivered record fiscal full-year 2024 revenue, growing 14% year-over-year (YoY) and surpassing $3 billion. It delivered 45% YoY EPS growth of $6.11, 61% net earnings growth of $373 million, and 46% YoY adjusted free cash flow growth to $348 million.

Its fiscal fourth-quarter 2024 EPS was $1.41, beating consensus analyst estimates by 15 cents. Revenues rose 10% YoY to $855 million, crushing the $810.39 million consensus estimate.

Aerospace Sales Grew Double Digits

Its commercial aerospace OEM sales grew 13% YoY, supported by strong demand despite supply chain challenges, while commercial aftermarket sales increased 17%, fueled by higher passenger traffic and greater aircraft utilization. Defense aerospace OEM sales rose 10%, driven by improved guided weapons shipments and ground vehicle growth, and defense aftermarket sales surged 21% due to better operational execution and a stabilized supply chain. Overall, Q4 Aerospace sales climbed 22% to $553 million, boosting earnings by 25% to $106 million and expanding margins by 200 basis points to 19.2%.

Industrial Sales Dragged Down by Oil and Gas

Woodward's Industrial sales fell 6% YoY to $302 million, while earnings fell 30% to $38 million, causing margins to slip 430 bps to 12.6%. The Industrial markets are comprised of three main segments: Power Generation, Transportation, and Oil and Gas. Power Generation saw 11% YoY sales growth driven by robust global power demand driven by data centers and associated backup power. This also caused an increased demand to support grid stability. The Transportation segment saw 22% YoY growth due to a healthy global marine market with shipyards at capacity with higher utilization.

There's been increasing demand for alternative fuels across the marine industry. However, demand for heavy-duty trucks was soft in China due to the weak local economy and narrowing fuel price spread. The Oil and Gas segment sales fell 3% YoY due to softening overall oil and gas demand. The outlook remains positive related to potential investments in refinement and petrochemical activities in China, India, and the Middle East.

Full Year 2025 Guidance

CEO Chip Blankenship was upbeat during the conference call. He noted that both segments, Aerospace and Industrial, reported strong performance. Aerospace sales rose 15% YoY to hit record levels as margins expanded 260 basis points. Industrial sales still hit a record that was boosted by its China on-highway product line, resulting in all-time high EPS and free cash flow increase by over $100 million YoY. He did note that the work stoppage had negatively affected its direct sales at Boeing, but the company shifted by redeploying resources to other areas.

For the full year 2025, the company anticipates:

-

EPS: Between $5.75 and $6.25 (aligning with the consensus estimate of $5.85)

-

Revenue: Between $3.3 to $3.5 billion (consistent with the consensus estimate of $3.38 billion)

-

Free Cash Flow: Between $350 and $450 million

-

Aerospace Sales: Increase by 6% to 13% YoY

-

Industrial Sales: Decrease by 7.5% to 11% YoY

The rise of AI and other computing needs is fueling the growing demand for data center power. Blankenship notes that "Woodward is well positioned to capture this opportunity, which includes control, actuation, and fuel metering systems for both base load natural gas and backup diesel applications."

WWD Stock Forms a Symmetrical Triangle Pattern

A symmetrical triangle is comprised of a descending (falling) upper trendline resistance converging with an ascending (rising) lower trendline support at the apex point. A breakout occurs when the stock surges above the upper trendline resistance. A breakdown occurs when the stock collapses below the lower trendline support. A breakout or breakdown becomes eminent as the stock gets closer to the apex point as the channel narrows.

WWD formed its descending upper trendline resistance near $187.44, while the ascending lower trendline support started at $145.80. The robust Q4 earnings report triggered a gap that peaked at $201.64 and triggered a gap and crap sell-the-news reaction that caused WWD to slip back into the symmetrical triangle range. Shares slipped through the upper trendline to retest the lower trendline and daily anchored VWAP support at $168.83. The daily RSI coil also stalled out at the 43-band. WWD will either fall below the lower trendline from here or retest the upper trendline, ultimately setting up a break as it nears the apex point. Fibonacci (Fib) pullback support levels are at $161.66, $152.81, $145.80 and $140.29.

WWD's average consensus price target is $187.44, implying a 10.32% upside, and its highest analyst price target sits at $228.00. It has four analysts' Buy ratings and five Hold ratings. The stock has a tiny 1.73% short interest.

Bullish investors can consider using cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, then writing covered call at upside Fib levels executes a wheel strategy for additional income while collecting the 0.59% annual dividend yield.

Grab This Altcoin Before Trump's Crypto Announcement

Grab This Altcoin Before Trump's Crypto Announcement

Whatever it is, I expect it to pump the market, which is why I'm recommending ONE coin to all investors right now.

Rubrik, Inc.: Under the Radar Cyber Security Stock Gains Traction

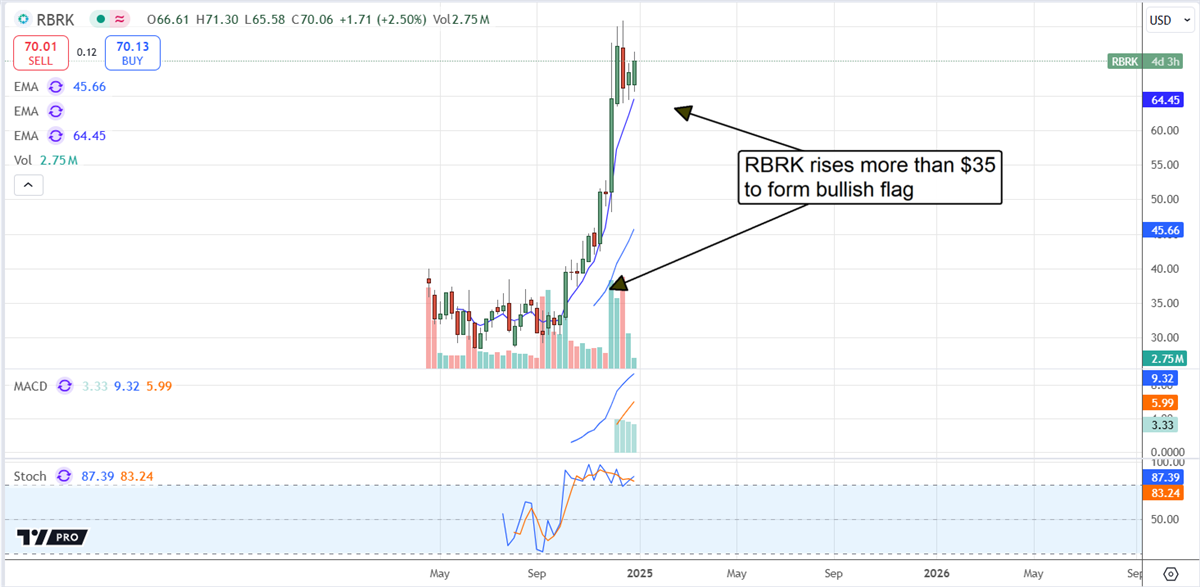

Rubrik, Inc. (NYSE: RBRK) is gaining traction with its business and its share price. Up more than 100% in Q4, the stock price is on track to double again over the next year. The company is establishing itself as a leading cybersecurity company focused on data, backup, and recovery for commercial and government applications. The latest news includes FedRAMP approval and expanding services to drive sustained sequential and YOY growth for many quarters. Commercial clients include mega-caps PepsiCo (NASDAQ: PEP), Allstate (NYSE: ALL), Home Depot (NYSE: HD), and technology leader Advanced Micro Devices (NASDAQ: AMD).

Rubrik Taps Into Billion-Dollar Government Cyber Security Market

Rubrik, Inc.’s FedRAMP approval is noteworthy for two reasons. The first is obvious: approval opens the door to the government market and the long-term contracts that come with it. The second is that the approval came on the recommendation of the National Nuclear Security Administration, which carries some weight.

The takeaway is that the company will likely benefit from its FedRAMP approval. Cyber security threats are rising at a double-digit pace and accelerating in 2024, increasing scope and cost, and cyber security is in high demand by governmental agencies. U.S. governmental cyber security spending is estimated to top $27.5 billion in 2025, roughly double the 2024 estimate and at record high levels expected to be sustained. The nod from the NNSA makes Rubrik a top-shelf option.

The company's business results since the IPO have been good. The first three quarters saw sequential revenue growth accelerate from 9.6% in Q2 to over 15% in Q3. The results also included better-than-expected guidance that suggests strength will continue. The company forecasted $232.5 million at the mid-point of the revenue range and may be cautious in its estimate. The forecast assumes a sequential contraction that goes against the trend.

Catalysts for growth in calendar 2025 include the roll-out of new API tools. The tools will allow users to connect their data to critical cloud infrastructure at Microsoft Azure and Amazon AWS with Rubrik in place. The takeaway is that Rubrik is entering the realm of AI and can facilitate the secure development of AI and AI applications.

Analysts Sentiment Drives Price Action in Rubrik Stock

The analyst sentiment trends are bullish for this stock, including increasing coverage, a rising consensus target, and high conviction. The number of analysts covering it reached 20 in December, up two for the month, with 18 or 90% rating it as a Buy. The price target lags the stock price in late December but is rising, up 50% in calendar Q4, with revisions providing a significant lift to the market. The high-end range of targets suggests a move to $83 is possible, another 18% upside from the critical resistance target, and higher targets are likely in 2025.

Institutional activity is also lifting this market. The institutions have been buying this stock in volume since its IPO and have acquired more than 50% of it, with activity ramping in Q4. Holders include ETF and mutual funds, public and private investment capital and provide a stable support base. Their activity aligns with the market's bottom and subsequent rally to new highs.

The technical outlook for Rubrik is solid. The 2024 uptrend is marked by high volume and bullish momentum, likely leading to higher share prices. The critical resistance is near $75 and will likely be tested in early January. A move to highs is a bullish signal. This stock could advance another $35 to hit the $110 level in that scenario, a move equal to the magnitude of the rally that came before it.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 Rubrik, Inc.: Under the Radar Cyber Security Stock Gains Traction"

Post a Comment