You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. (A Must Read) How Finance Really Works After 2008...A breakdown in post-2008 finance by Adam Tooze confirms what we're preparing for and against... the Mother of All QE Events... coming to America in the years ahead...

Dear Fellow Traveler: When I started Me and the Money Printer, there was a simple focus on four macro-market concepts: Global debt, liquidity, insider buying, and market momentum. They all explain a lot about market timing, public policy, and the occasional chaos and then massive rebounds unleashed by a leveraged, largely unregulated system after the Great Financial Crisis of 2008… They also explain why, in the post-GFC world, the attitude about the financial system and our equity markets among people who truly understand how it all works… especially when all hell breaks loose (like it did in April 2025 or in the August 2024 Nikkei crash) and policymakers scramble to stop a total crash… has been this…

Every major downturn since 2008 followed a similar pattern, and every “crash” concluded with significant fiscal and/or monetary policy accommodations. The corporate insiders also bought at the same time the policies shifted, and then, a V-shaped recovery… really a K-shaped one… followed. The rich got richer, while the middle class was squeezed by currency debasement and higher prices on essential goods and services (especially in the cities)... The money supply surged with the creation of new capital to shore up growing debt… And all of this went underreported because half of America would likely march on the Eccles Building if they understood the lasting impact of post-GFC central banking… All that said… one of my most challenging tasks is explaining to people just how much the world of finance and economics has changed since the 2008 financial crisis. The concept of traditional banking has diminished for years, having been replaced by a shadow system that few people even know exists, let alone understand. To reinforce this truth, I'm always looking for voices that see the world for what it is… and honestly discuss it, instead of keeping it a secret that they only trade themselves. People like… Stanley Druckenmiller, David Tepper, QTR Finance, Tim Melvin, Michael Howell, Zoltan Pozsar… And historian Adam Tooze. On Friday, I revisited an incredible article by Tooze from July 2025. This article perfectly captures what has happened to the global financial system, why things always feel broken, and what is hiding in plain sight about our markets... Tooze started his analysis by doing something few people are willing to do… He actually read the Annual Economic Report of the Bank for International Settlements (BIS), a 2025 report that openly, yet academically, concedes reality. Tooze begins with the most important part of the admission, as stated in the report itself… Writes the BIS (skip ahead if it hurts your brain, I'll explain it)::

Let’s put that into simple terms.…

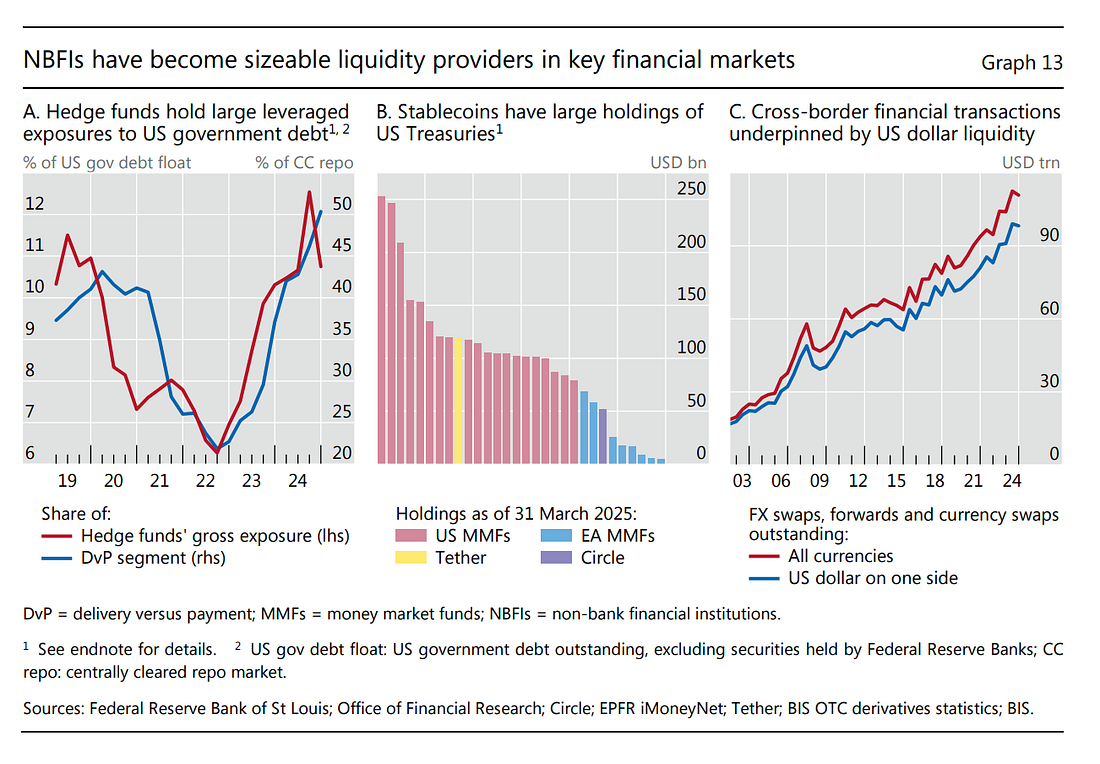

Yeah… It’s a lot to digest… But I’ll simplify it for you… Let’s start from the beginning… Let’s Dig A Little Deeper…Tooze kicks the ball through the uprights… The financial system has undergone a major transformation (turning into something that doesn’t resemble capitalism, but looks more like a hyperleveraged atomic bomb). This will sound somewhat familiar if you’ve been following me for years… First, there’s been a key shift in who buys and owns U.S. debt abroad… We know it's no longer China buying with fervor... Foreign private investors (largely investment funds in advanced European and Asian economies) now hold the majority of foreign-owned Treasuries. Second, instead of banks lending to businesses, hedge funds and shadow banks now buy government bonds and effectively run the show… while the Treasury Department and Federal Reserve smile, nod, and ignore the obvious threat today... Hedge funds now control 10%+ of tradeable US Treasuries (free float) using a significant amount of leverage, according to the BIS. It’s in the chart on the left…

The U.S. government is fine with it all because it creates Treasury bond demand and helps suppress yields, which is vital for a nation that’s $37 trillion in debt and rising. These funds also borrow money to buy even more bonds through a global FX derivatives market worth $111 trillion, with 90% of the deals involving dollar funding. All the while, the BIS notes that "private credit funds' assets under management have surged from $0.2 billion in the early 2000s to over $2.5 trillion in 2024." (Pg. 49) Here's what that $2.5 trillion surge really tells us about the banking system… Traditional banks have retreated from business lending. They’re either too scared (regional banks), too regulated (community banks), or just too lazy (mega banks) and shifted priorities after 2008. Many large banks would rather park their money in "safe" government bonds or shift toward loan origination for private credit providers than take on actual business risk. Everything’s been moved off their balance sheet… out of their regulators’ eyes… So, US businesses were pushed into the arms of private credit funds… These shadow lenders raise a pool of capital, then charge 12% to 15% instead of the 6% to 8% that banks used to charge. Sure, the lending is still happening, but now it costs a fortune. Meanwhile, a different group of shadow banks, hedge funds, has turned the Treasury market into a leveraged lemonade stand as they try to squeeze every single drop out of the Basis Trade. These aren't your traditional banks… These are the gunslingers who can buy Treasury bonds… then…

Effectively, the real US economy receives expensive loans, while shadow banks play Russian roulette with the "risk-free" asset of the global financial system... Oh… and one more fun thing from the report… That massive $111 trillion market in FX swaps doesn't appear on standard accounting books… It’s all off-balance sheet.

It’s effectively hidden leverage that can immediately fuel a sudden financial crisis. That’s basically what happened in August 2024 with the "yen carry trade" unwinding (more on that tomorrow… because it’s a doozy…) Isn’t finance incredible, everyone? No… this isn’t a dream…

So… one more time for the people in the back… Wait… Step Back… Hold Up…Yeah, exactly… A reminder, here's how leverage works in this brave new world. The funds buy Treasuries, then use those SAME Treasuries as collateral to borrow more money. They then use that borrowed money to buy more Treasuries. Many can borrow up to 100% of the value (no "haircut" protection). That's right, no margin of safety. It's like jumping out of a plane with a parachute you bought on eBay from that Chinese account with only four historical sales and three one-star reviews... This creates a massive house of cards where small price moves trigger forced selling. Now, here's the problem… as Tooze explains. When fear hits or leverage breaks, the entire system can freeze or has frozen, since US Treasuries serve as collateral for everything else. In addition, these funds are far more interconnected globally than banks ever were... And, we’ve seen the result… Events in March 2020 showed what happens when the Treasury market freezes, and only unprecedented central bank intervention can save it… And August 2024 proved that the U.S. Federal Reserve isn’t as independent as it seems… The same BIS report (more on this tomorrow) shows that when Japanese investors unwound their positions last year, US markets felt the impact immediately… The BIS is the most conservative institution in finance… and they called the effect 'notable.' The exact words are that 'cross-border spillovers...are in some cases comparable with the effects of domestic transmission.' Comparable means the impact of Japan’s unwind has the same effect on U.S. economic conditions and markets as the Fed's own policy tools. As a result…the Fed must always anticipate what Tokyo, Frankfurt, or London may do. That's not central bank independence. That's a shadow FOMC with members from every major financial center. It’s Not Just Bonds, It’s EverythingHere's what Tooze's analysis doesn’t dive into, where his arguments complement mine, and what matters for you as an equity investor or trader… When Treasury markets seize up (like March 2020), hedge funds face immediate margin calls on their leveraged bond positions. The issue? Many funds also use Treasuries as collateral for equity positions, options strategies, and risk parity trades (a blend of stocks and bonds in leveraged combinations). The latter is a funny way of saying… “We’re market neutral.” [Narrator: There’s no such thing as market neutral in a liquidity crash.] Risk parity positions can crater when correlations break and traditional hedges fail to perform as expected. When correlations rise, everything goes in the same direction - bonds, stocks, other assets - and it’s usually down. It occurs during a panic or liquidity crisis, where sellers are forced to dump whatever they can, not necessarily what they want to sell, so even safe-haven assets are vulnerable. As the dominant driver is “forced selling” (more on that soon), there is a heavy demand for cash. We saw this happen in 2008, 2011 (Europe), 2016 (China), 2020 (Global), and the 2022 shock. Here’s where it gets tricky, but it explains what has been happening in equity markets. To meet those margin calls, the funds must sell their most liquid assets… and FAANGs (or Magnificent 7 stocks if you will) are among the most liquid assets they own… They’re second only to Treasuries themselves in terms of ways to get cash now... So, when Treasury volatility spikes, the collateral value drops, forcing liquidation across ALL positions. During periods of deleveraging, funds sell in this order:

And again, many funds also employ "risk parity" strategies - borrowing against "safe" Treasury securities to buy "risk" assets like stocks. When correlations break (both bonds and stocks fall), funds must delever on both sides simultaneously. This is what happened in March 2020... FAANG stocks get hit first and hardest because they're the easiest to sell quickly in size… However, they’re also the overwhelming weight on the S&P 500, which means a lot of deleveraging and selling at the same time, taking the market down quickly. What’s worse? Well, we have to think about all the money tracking the S&P 500 and the active managers who treat it as a benchmark to their own performance (and resultantly, end up owning the same stocks as the leveraged funds…) Passive funds - which may have very specific rules on the types of stocks they own or on the weights they have to replicate a broader Index like the S&P 500 - can also experience forced selling - triggering greater equity losses… And active investors and many money managers… well, they’re going to dump too at the first sign of real trouble… That leads to even more panic and volatility… That is why I continue to recommend watching the Bank of Montreal MicroSectors FANG Index 3X Inverse Leveraged ETN (FNGD)… An FNGD surge indicates massive, concentrated selling pressure on the world's largest and most liquid stocks. It broke out right as our signal turned negative on February 24, 2024, ahead of the April crash.

And here’s a chart of the FNGD breaking out during the COVID crisis…

Both charts rise quickly as equities plummet, revealing the same thing… This pattern isn't normal profit-taking - it's liquidation. The violence and speed of FNGD moves (3X leveraged remember) captures forced selling very well... which is why I worry when it breaks above its 50-day EMA. The same funds managing portions of the $111 trillion in FX derivatives market almost certainly own massive FAANG positions. When they have liquidity needs and Treasury collateral becomes stressed, they need cash quickly. MAG 7 stocks are like a working ATM in the middle of a massive power outage. Again, these are the only other things liquid enough to sell in size very quickly… Even if they are cascading in price… So What?So what? So, let’s dance…

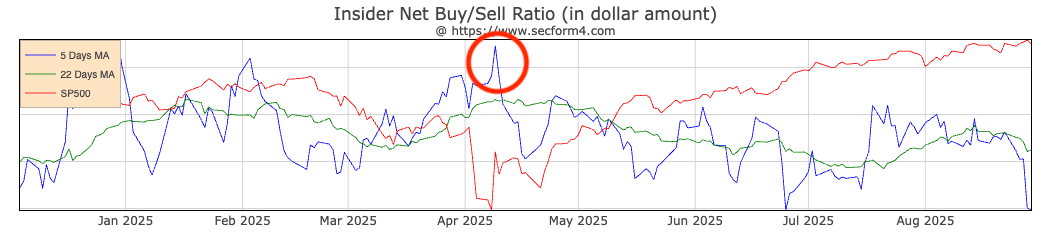

The music has been playing again since April 8, when the Insiders bought in droves, trade policies were accommodated (though supportive policies by the Fed and Treasury were also in effect around this time), and momentum returned to the market.

But what happens now if we need another HUGE bailout like in 2008 or 2020? [Narrator: We’ll need another huge bailout at some point…] Well… you know what that means… That’s the sound of money printing. It’s music to a gold bug's ears and terror to anyone holding cash. There's a reason why future QE or other stability measures will be necessary… As Tooze explains, this isn't like 2008, when we could identify and bail out specific banks. These are unregulated entities playing God with the US government bond market itself… You know… the "risk-free" foundation of international finance. Tooze's core warning: "The liquidity of the US Treasury market is nothing less than the foundation of the entire global financial system. That could now be at risk." [Narrator: It is at risk… that’s what’s been going on since COVID…] And when it fails, it fails fast... If we get something bigger…the Fed would have to buy unlimited bonds or watch everything collapse. …. …. BUT…

There’s A Catch…Tooze is also concerned about the current state of the political landscape… The problem is that President Trump and the Fed are not on the same page. That felt pretty apparent back in April… when leveraged funds were dumping Treasuries, and no one thought it was smart to ask people like former Fed Chair Janet Yellen why the funds owned so many Treasury bonds in the first place… Tooze writes, "Currently, there is no immediate crisis, but relations are even worse” with Trump and the Fed now than in 2020, making the next crisis response uncertain. The ground the entire system stands on - US Treasuries - is now controlled by highly leveraged funds that use the bonds themselves as collateral to buy more bonds. In times of stress, they all run for the exits at once. And if the bond market goes… the equity market will follow. We’ve seen it happen multiple times since 2008… and remember the pattern… because it always goes one way… The real question… the one that Jamie Dimon asked… is when and if the music really stops. What happens when the funds stop buying or have to stop buying? Well, the Fed will likely have to engage in the Mother of All QEs… The question is whether we have the political cohesion to respond correctly or quickly enough, and how that will impact Americans, many of whom are already priced out of housing, equities, and other assets due to the bailout culture we’ve already endured. We’re more politicized than ever… we have financial leaders blaming inflation on supply chains instead of monetary policy for where we are today… and all the while… I’ll bet 99% of Americans have zero idea about what I just explained today… They’ll likely blame capitalism… and whomever is in charge at that exact moment… Even though this has been building and festering since 2008… and years prior… The thing is… you’re now aware of what’s happened for 17 years… Even though you may have wished you’d have just taken the Blue Pill…

Sometimes ignorance is bliss… That said, you’re in the car now… And all roads lead to more monetary inflation, more bailouts, looser policy, and greater misdirection in the post-2008 world. So plan your drive accordingly… And if you are just getting started, we’ll show you how… Stay positive, Garrett Baldwin P.S. The BIS revealed several other things that require a deeper dive… things like the fact that when you pay someone, your money doesn’t actually go anywhere - it’s just moved around on spreadsheets… and that stablecoins don’t really hold their value, are easy ways to engage in money laundering, and will probably end up undermining other countries' control over their own economies. But hey…

About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "(A Must Read) How Finance Really Works After 2008..."

Post a Comment