You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. How I Learned to Start Worrying And Hate The Bond Market BombI read the 2025 BIS Annual Report... and now I'm reminding myself why I don't dig too deep into things unless I want to lay awake at night... I now have seven reasons "why it's worse than we thought."

A Special Labor Day Weekend Edition Dear Fellow Traveler: Have a drink… have five… Yesterday, I discussed Adam Tooze's piece on global finance and the major systemic shifts after the 2008 Great Financial Crisis… But I went ahead, before the Texas-Georgia football game yesterday, and got curious. I read the Bank for International Settlements' 2025 Annual Economic Report. The BIS is considered the “central bank” of the Federal Reserve and other central banks. I wish I hadn't read it… It's a bureaucratic manifesto… Then I watched Margin Call - the film about a Wall Street firm that discovers toxic assets, and scrambles overnight to dump them before market collapse. I revisited the scene where the banker who discovered the problem looks around the streets of Manhattan and says that none of the people out to dinner or at bars have any idea what’s about to happen to the financial system (consider this around 2008). I look around and conclude that few Americans know what's going on today either… Or want to… The need to… Because if you have a bank account, you'll soon question everything you think you know about money… Since I'm that way… I've included page numbers and direct quotes from the report... And clear expectations on what’s ahead. It's too important… and parts of this are disturbing. 1. I Was Right. The Fed Has NO CONTROL Over US Financial ConditionsAmerica’s central bank, the Federal Reserve, has lost control of its policy and its influence on financial conditions and markets in the country. All of the talk about interest rates and job markets… It’s ALL THEATER. I've long argued this very fact, largely because I've been curious about cross-border flows and the broader macroeconomic events that have created loose conditions since the 1990s. To reach that conclusion, I’d previously cited my summer Global Business class with Forest Reinhardt, The Dollar Trap by Eswar Prasad, Capital Wars by Michael Howell, The Code of Capital by Katharina Pistor, and Jeff Snider's "Eurodollar University…" However, this report makes the explicit case for the Fed’s global interdependence, not its independence (the latter, which Jerome Powell claims is threatened by Trump). The Fed's control over American monetary policy isn't what it used to be. And may never be again… Last year proved the point… We don’t talk about the crisis last year in Japan - because it seems so far away… But when Japanese investors unwound their carry-trade positions in August 2024, U.S. markets felt the impact immediately. Page 63 states plainly:

To simplify what this means… Imagine you used to control your home's temperature with a thermostat. But years later… your neighbor's thermostat now affects your house temperature almost as much as your own. You still have some control, but you're no longer fully independent. This is our central banking system today… It represents a fundamental shift in how monetary policy is supposed to work... Central banks can't act in isolation and haven't truly been able to since… a long time… If you read "Lords of Finance" by Liaquat Ahamed, the book explains how the gold standard similarly constrained central banks and capital flows to nations before the Great Depression. In fact, Ahamed argues the Gold Standard, reintroduced after World War I, fueled the Great Depression… However, in modern times, Page 65 confirms just how deeply this issue extends…

This means they’re all connected through these powerful transmission channels, primarily through the international financial managers discussed yesterday... Now, the report does note on page 64…

But when foreign spillovers are "comparable" to domestic policy, we're in an interconnected world where one nation’s sneeze becomes the next global financial crash. Recall that the Fed sought to normalize rates in 2015-2016… They had to stop partly because China's devaluation and European weakness were tightening US conditions for them. The Fed now has to factor in what Tokyo and Brussels are doing before making any move. This isn't the monetary independence we were promised. And… let’s speculate here… Have we considered that this could be a part of the Trump vs. Fed fight that people aren't thinking about - that the Fed is already far less independent than it claims? 2. Stablecoins Could Blow Up the Treasury Markets Yesterday…Sure… why not? According to Graph 3.A on page 88…

Tether - the company that won't reveal all of its banking relationships and sits offshore- now moves Treasury markets like Fidelity. And Circle, which nearly imploded during the Silicon Valley Bank collapse, will start to impact markets in a similar way to BlackRock. The report (page 88, Graph 3.B) quantifies it:

In Treasury markets, “5 basis points” represent billions in value shifting. All because offshore entities decided to issue more tokens. Here's the kicker on page 89…

When crypto panic strikes - like FTX or the next disaster - stablecoin redemptions could hit the Treasury market with triple force. We've handed over influence to the world's "risk-free" asset to entities that could implode overnight or through an unforeseen banking crisis, which the media often fails to detect when we’re barreling into one and warn retail investors in time. The US government spent 100 years building the world's deepest and most liquid market in history. Now, companies that won't even disclose their auditors can move or freeze it. What a time to be alive… 3. Banks Are More Exposed to Private Credit Markets Than I ThoughtRemember 2008? When banks swore they'd never again hide risky loans on their balance sheets? Well, the “warehousing” game continues. It’s not Lehman or Enron level yet - there’s more disclosure these days… However, Page 26 reveals what your banks probably don’t want to discuss, as the activities will likely draw comparisons from harsh critics.

What the hell does “warehouse portfolios" mean? Well… pour another... That’s banker-speak for "we're holding these risky assets temporarily and hoping we can offload these hot potatoes to someone else before market conditions change." Basically… the entire plot of the movie Margin Call…  There’s a definition in an endnote 21 (p. 36, Ch. I)…

"Temporarily." What a word… Again… the plot of Margin Call. A temporary problem can become a permanent one when credit markets freeze. That’s highlighted on page 26…

So, when credit markets freeze, the "safe" bank gets stuck holding billions in leveraged buyout loans. The same loans that would take companies private at elevated multiples, accompanied by significant debt loads. And when they can't offload them? They stop lending to Main Street businesses and homebuyers (if they still do this…) This bank… that’s supposed to be… banking… isn't now taking deposits and making loans in this scenario... They're stuck in the middle of complex transactions that have suddenly become illiquid, and they can do nothing but pray for the liquidity conditions to resolve... [Narrator: They’ll need a bailout… but don’t call it a bailout… People get upset.] So what will probably happen when the music stops again? The Fed will likely need to establish a new lending facility, similar to the Bank Term Funding Program (BTFP) of March 2023 after the Silicon Valley Banking Crisis. The goal would naturally be to stabilize those banks and ensure credit reaches the economy. Perhaps a program to provide liquidity in exchange for these risky loans… Which feels nuts - but they’re already urging a program to bail out the Basis trade. They’d probably call this toxic private credit facility something like the E.M.L.F. The Emergency Market Liquidity Facility… since everything's an emergency now. Although I think - if we get to this point - they should call it L.A.U.N.D.E.R. Liquidity Assistance for Underwater Non-Performing Debt Emergency Relief facility. Clean those dirty loans, everyone! The truth is that naming a bailout program something mundane… it doesn’t work. The cat’s out of the bag, and it’s just a new form of liquidity that drives markets higher. I’d prefer it if the Fed got desperate, they would just cut the head off a chicken and let it run around until it lands on the words “Bailout…”

Then blame the chicken. And speaking of the Basis Trade… 4. Hedge Funds Control An Impractical Amount of Treasury Debt - And No One Thought to Ask Janet Yellen or Jerome Powell… Why?I mentioned this yesterday, and it’s stunning when you put it into perspective. On Page 27, it explains the current level of leverage surrounding U.S. debt…

Again… ten percent… which is a massive number… A handful of hedge funds now control more Treasuries than most sovereign nations. But we’re not done… because the borrowing terms in the repo markets don’t require much to increase their leverage… Check the endnote 24 on page 36… it reads:

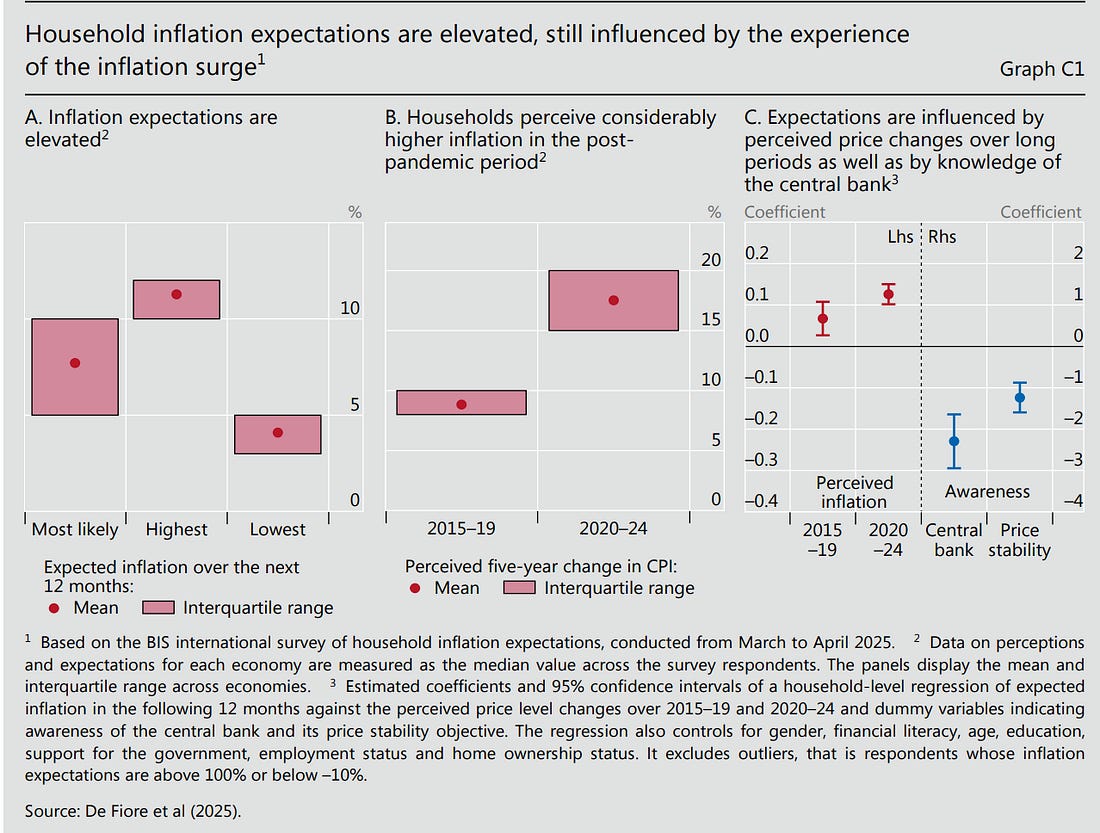

So, as I said about leverage, these funds are borrowing 100% of the value of their Treasuries. There’s no margin and no buffer. This is like buying a house with a 100% mortgage, then using that house as collateral to buy another house at 100% several times. The report sanitizes this by calling these strategies "procyclical." That's an economist’s way to bullshit and not have to openly say, "when things go bad, they amplify the downturn." Procyclical means that when markets rise, they leverage more. When markets fall, they're forced to sell everything at once. One fund faces margin calls… and others will follow. They’re all interconnected. March 2020 gave us a preview. The U.S. Treasury market is the deepest, most liquid market in human history. And yet it froze. The Fed had to inject trillions just to get it functioning again. And that was when hedge funds held less Treasury exposure than they do today. So, imagine a few percentage points of all floating Treasuries being liquidated in a compressed timeframe because a hedge fund's risk model failed to account for a tail risk event. (I keep referencing the film Margin Call… substitute MBS in the movie...) And that’s also a possible scenario in a world where people might start relying on AI, but fail to actually check the work or know what the inputs really are… Even without that future worry… The leverage is concerning. The concentration is concerning. The lack of haircuts is concerning. And yet, journalists can’t be bothered to ask follow-up questions to people like Janet Yellen about why these funds own so much “safe-haven” debt in the first place… Or even deeper ones like… why did the U.S. government put us into this situation in the first place that ultimately required us to tolerate all this financial engineering… It’s maddening… 5. Inflation Expectations Have Broken People’s Spirits Worldwide… And I Expect That Will Lead To More Polarizing Political OutcomesI might have found the real reason why the socialists are winning in U.S. cities… But even they probably don’t know how to articulate what’s going on here… People like Paul Krugman and Fed sycophants kept telling you inflation was conquered. The BIS data suggests otherwise. Page 22, Graph C1.A reveals the damage…

What’s the official, actual inflation in advanced economies? According to the report, around 2% to 3%… Now, assume the official inflation data is correct… That difference between expectations and reality is not a rounding error. That's mass psychological scarring. The BIS would argue that people are living in a different economic reality than the data suggests. Why? Because people got burned badly in not just the last five years, but the last decade... The report documents it on Page 22:

But here’s the thing… Are those households wrong? First… the U.S. dollar alone lost 21% of its value from 2020 to 2024… And second, you have the central bank of central banks saying one thing… And then you have groups like the Chapwood Index actually tracking the things that people buy in cities across the United States… and they’re reporting compounding double-digit price increases over the last eight years in places like Manhattan… Regardless, people can't shake inflation fears. They're still flinching from the last punch. The killer quote is buried on pages 22-23 and is presented as a challenge for policymakers. It reads…

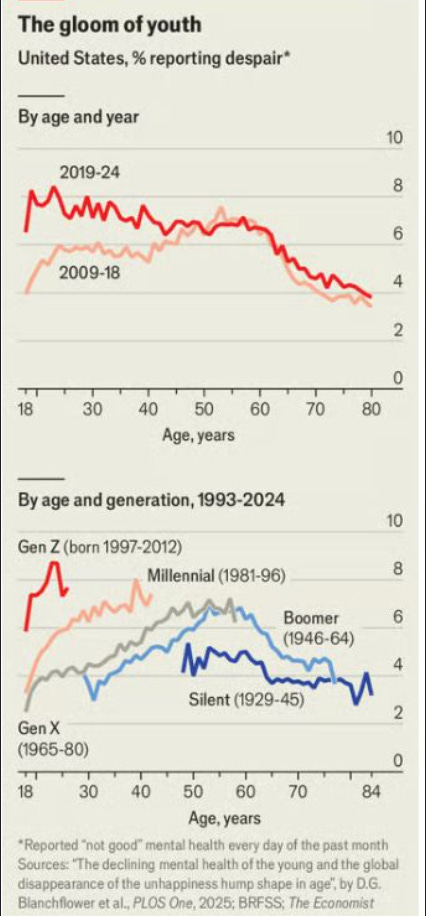

They might as well have just said inflation expectations are hereby destroyed. That’s what I interpreted from Jerome Powell two weeks ago… But what Powell and others won’t say is the issue… Once people stop believing prices are stable, that belief becomes self-fulfilling. Workers demand higher wages because they expect higher prices. Companies raise prices because they expect higher costs. An inflation spiral begins. The Fed appears to have broken something fundamental… That’s the basic trust that a dollar tomorrow will buy roughly what it buys today. According to the BIS's own data, that trust is unlikely to return anytime soon. The inflation psychology has shifted, possibly for a generation. I look at this chart below and think to myself… we’ve got a serious issue beyond debt and inflation…

We have a generation of people who are deeply impacted by the financial mistakes of past generations. They’re unhappy, depressed, and perhaps angry. I can understand, just by looking at the many financial realities brought on by our fiscal, monetary, supply-side, housing, banking, and other policies since the 1990s. And many unhappy Gen Z and Millennial Americans are going to vote “good and hard” for something different… What will they vote for? That’s the question… But the one thing - and maybe the only thing - they can control is their vote. Don’t dismiss this. Too many people did that in 2016. I can guarantee there will be political consultants and TV pundits using the term “Dispair Vote” in the 2026 midterms and 2028 Presidential election… The “Dispair Vote” percentages are so high they could swing many elections… 6. Central Banks Are Building Programmable Money… But Don’t Worry… They’re TOTALLY Not Going to Do Something WRONG There…Oh… yeah… by the way… Just in case you need more paranoia… This one… Central banks quietly began building something more significant than the CBDCs that had everyone on edge. This could be good or bad, depending on the use cases.... Page 97 lays out… Project Agorá… The author calls this…

[Editor’s Note: Can you punch me directly in the face and knock me out for a few hours? This will be in every financial newsletter promo on the planet, won’t it?] The author writes on Page 97 that the Agora project ended…

This is happening now... So… what exactly are they building? Page 91 describes "atomic settlement" and "contingent execution of actions…" This is programmable money where transactions can have built-in conditions and execute automatically. It’s ground-breaking stuff… This means money that can:

The BIS report emphasizes the benefits for wholesale banking and market efficiency. It’s increidble technology… But here's the thing… There’s plenty of reasons to be skeptical. The second you build the infrastructure for programmable money, other capabilities will exist whether you use them or not. What safeguards are being implemented at the legislative level right now? Does Congress even know what’s going on here? A technology that enables instant settlement could create transaction controls. The system that automates collateral management could theoretically automate spending restrictions… Smart money has surveillance built in…I’m saying it could stop you from buying things that someone doesn’t want you to buy… whether that product is legal… or not… The infrastructure for "contingent execution" refers to money that follows rules. And as we know, those rules are written by whoever controls the system. I'm not saying they're planning to control your spending. But I’ll leave the door open to that happening… because I don’t trust authority… I recall Bernie Sanders once complaining that there are too many types of deodorant and sneakers in America… Don’t tell me an idiot like that, or some of the other politicians who can’t mind their own business, wouldn’t put that technology to work to fit their “good world view...” The BIS report doesn't AT ALL suggest this will happen... And I’m not saying it will… But they're building tools that could do exactly that if policy ever shifts. Seven central banks and 43 major financial institutions are fundamentally changing what money can do. While they're selling it as efficiency - which it DOES provide - they're also creating unprecedented capabilities for monetary control. History shows that infrastructure matters more than intent. Because infrastructure outlasts the people who built the damn thing... 7. The U.S. Dollar Just Stopped Acting Like the Reserve CurrencyFinally… this is something I’ve forgotten to write about… because it felt like an anomaly or that I must have missed something… But something happened in April 2025 that should have made headlines worldwide. It didn't. The dollar didn’t rally during April’s selloff… the thing that is the instrument of settlement for so much debt didn’t see a swing up in demand at a time that it appeared something was seriously off in the global markets… It’s on Page 12… It reads:

For 80 years, whenever markets panicked, investors have fled to the US dollar. However, when the April 2025 tariff announcements were released… and the markets tanked… and the dollar fell. The world's reserve currency failed to act like one. What happened is on Page 87… It reads:

You see… people still wanted dollars… just not the ones from Washington. They're choosing Tether and Circle's digital dollars on blockchains beyond US control. And Washington could see this was going to happen from 100 miles away… So, here’s my interpretation of events… The GENIUS Act appears to be Washington's response to this reality. This legislation requires stablecoins to hold US Treasury securities, enforce US sanctions, and be subject to full regulatory oversight. It's a catch-22, though… and China will clearly respond with its own stablecoins… Washington needs stablecoins to buy Treasuries… As I’ve noted, they're now major buyers of debt, according to the BIS. However, the moment stablecoins become fully regulated and sanctions-compliant, they may lose what makes them attractive… the fact that they existed outside traditional US monetary and fiscal control. In my view, we're watching the US government become dependent on the very instruments that could undermine the dollar's decades-long monopoly. They need stablecoin Treasury demand, but regulating them could affect that demand. The BIS documented the dollar's failure as a safe haven, while “synthetic” dollars thrived. The GENIUS Act, in my view, is Washington's admission that they saw it coming and scrambled for a solution fast... When your reserve currency stops acting like one, and your solution is forcing its competitors to buy your debt, the system has fundamentally changed. The Crypto Bros built an alternative network… and authorities just took away their keys… It’ll be very interesting to see how this gamble pays off… My bet… it exacerbates a liquidity event in the future… All while other central banks around the globe continue to build their gold positions… I Guess We’ll Find Out What Happens… Right?Every fact I've shared comes directly from the BIS report, with page numbers and quotes. The implications and interpretations are mine, but the facts are theirs. What we're seeing is a financial system in transition:

The question is no longer whether the system is changing. I feel that we’re living through a monetary regime change that could soon rival the end of Bretton Woods in 1971. And there’s not enough conversation about it… The difference is, it's all happening in slow motion, with algorithms and stablecoins instead of gold and treaties. Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "How I Learned to Start Worrying And Hate The Bond Market Bomb"

Post a Comment