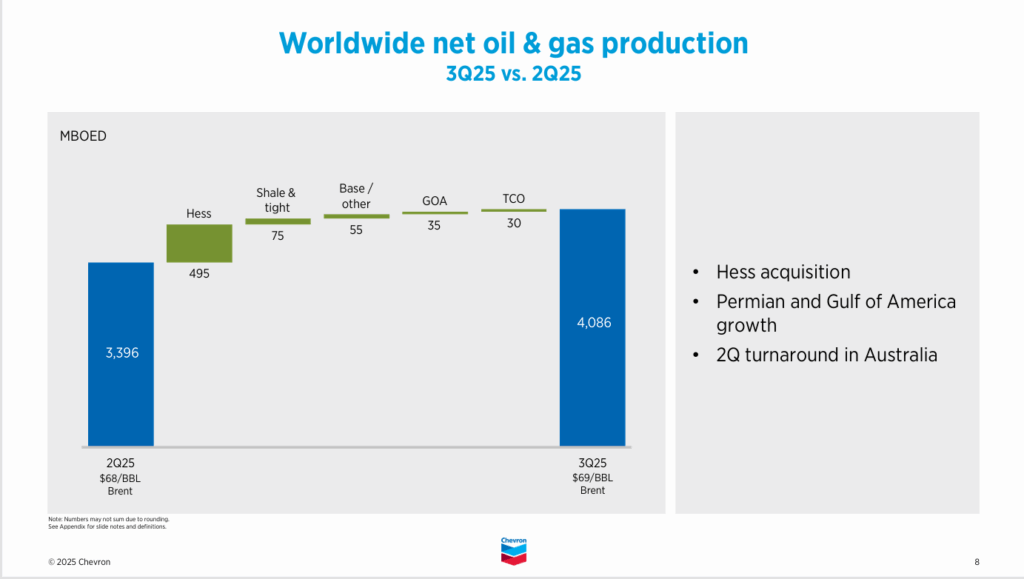

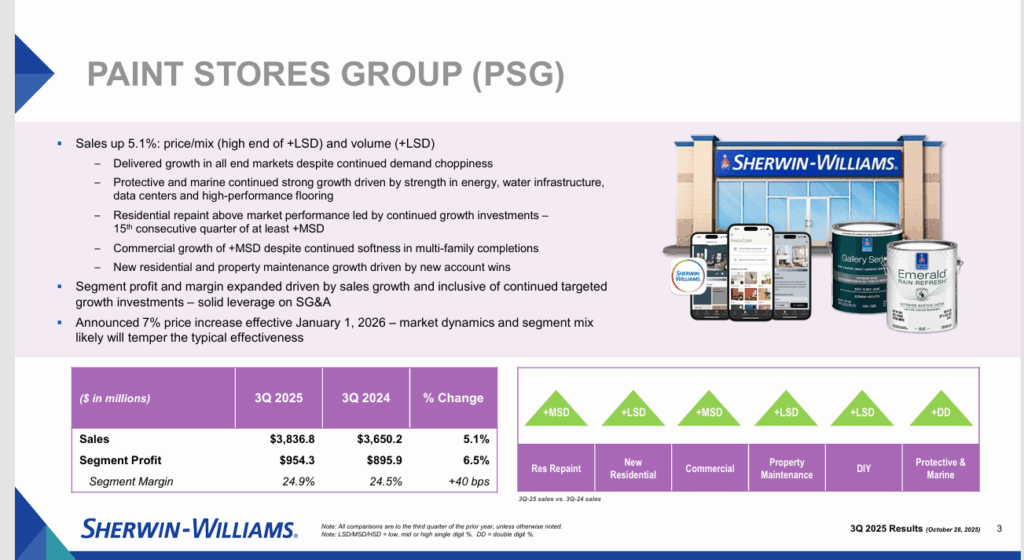

Lane Mendelsohn, President | © 2025 Vantagepoint AI, LLC. All rights reserved. Today's editorial pick for you 3 Dividend Aristocrats to Buy for Growth and Income in 2026Posted On Nov 10, 2025 by Chris Markoch  Dividend aristocrats are a group of high-quality companies that have increased their dividend for at least 25 consecutive years. If you're an income-oriented investor, these are blue-chip names that have rock-solid balance sheets that keep those quarterly dividend payments coming in like clockwork. Table of ContentsHowever, at a time when many technology stocks are delivering 2x or greater gains for investors, even dividend aristocrats can seem boring to investors. However, boring can be beautiful. The market is likely entering a period of sector rotation. The combination of lower interest rates, traditional infrastructure spending, and consumers likely to receive significant tax refunds in 2026 due to provisions in the One Big Beautiful Bill is likely to create a revival in some sectors that have been lagging. That’s showing up in the analysts' forecasts for several dividend aristocrats. These companies are not only well-known to investors; they're well-known consumer names as well. And right now, they're offering the near guarantee of a growing dividend with expectations for higher stock prices, fueled by earnings growth. Dividend Aristocrats to Buy: Chevron Sets Up to Be a GusherThe last five years have been brutal for oil stocks. First, there was a global pandemic, and even today, consumer demand is under pressure from sticky inflation followed by rising interest rates. Adding to the woes for Chevron Corp. (NYSE: CVX) was a delay in the finalization of its merger with Hess Corp. CVX stock has delivered a negative total return of 3.38% in the last three years. That’s despite increasing its output, which topped 4 billion barrels a day in the third quarter of 2025 for the first time ever.  However, Chevron is about much more than oil. The company is one of the leading providers of liquefied natural gas (LNG). It also has several clean energy initiatives that are moving the company on a path to a sustainable future. Higher oil prices at some point in 2026 seem nearly inevitable. There is the ongoing need for natural gas to power data centers, the reshoring of manufacturing in the United States. Plus, the country's own need to repair our traditional infrastructure. All of this lines up for higher oil prices. Analysts agree. CVS stock has a consensus price target of $165.45. That's about an 8% increase from its price on November 10, but it's lower than the company's expected earnings growth of around 16.6%, which suggests higher revisions are likely. Chevron has increased its dividend for 38 consecutive years, and the stock has a current dividend yield of 4.46%. This is in addition to the company's ongoing share buyback program. Dividend Aristocrats to Buy: Sherwin-Williams is Ready for a Renovation RevivalSherwin-Williams (NYSE: SHW) may seem like a contrarian play with a weak housing market. However, the market is forward-looking, and analysts are considering the impact of lower interest rates on the home renovation market. Paint is a fast and relatively inexpensive way to freshen the look of a home. And Sherwin-Williams is the category leader. The company announced a 7% price increase for its paint stores group effective January 2026. That means that earnings growth expectations for around 11% in the next 12 months may be too low.  It's worth noting that, despite the weak housing market, SHW stock has delivered a total return of over 57% in the last three years. Analysts give the stock a consensus price target of $390.87, which is about 15% higher than its share price on November 10. Skeptics may point to the company's price-to-earnings (P/E) ratio, which is around 33x as of this writing. However, that's below its historical average and above the 28x forward earnings forecast. Plus, while the dividend yield of 0.93% may not excite investors, that dividend has increased for 48 consecutive years. It’s also well covered by a payout ratio of around 30%. Dividend Aristocrats to Buy: Stanley Black & Decker May Go from Laggard to LeaderIndustrial stocks have been performing well in 2025, which makes the performance of Stanley Black & Decker Inc. (NYSE: SWK) discouraging for investors. SWK stock is down approximately 15% in 2025 and the stock has managed only a 0.34% total return in the last three years. The company reported third-quarter earnings in November. Despite a beat of more than 20% on the bottom line, revenue came in flat both sequentially and year-over-year. The company cited tariff pressures and soft consumer demand as reasons for the topline results. But the company's efforts to improve its gross margin are moving the needle for analysts who are forecasting a 21.9% increase in earnings in the next 12 months. That’s why analysts give SWK stock a consensus price target of $88.10. A nearly 30% increase in the next 12 months. That goes along with a dividend that yields 4.89% and has increased for 58 consecutive years.  This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe. StockEarnings, Inc |

0 Response to "Gold’s Up 50%. Here’s What Most Traders Missed 😥"

Post a Comment