|

You see the breakout after it's already up 40%. |

My Ghost Prints scanner sees the volume spike three days before that happens. |

It caught KSS before the 375% run. RKT before the 150% surge in 25 hours. PLUG before the 206% climb in 5 days. |

Right now, it's flashing on multiple setups. And what it's showing explains why December might not deliver the rally most traders expect. |

👉 JOIN ME LIVE MONDAY 7PM EST. |

|

How to Fade the Biotech Squeeze |

By Brandon Chapman, CMT |

Markets don't believe in Santa Claus...but traders do. |

Every December, the same pattern emerges. Traders convince themselves this time of year magically produces positive results. Then reality hits. |

Pull up the sector performance list from Friday. |

Energy led. Financials rallied. Gold sat near the top. |

Gold doesn't rally during risk-on environments. High beta names just squeezed higher for four straight days. |

Rate cut odds jumped from 30% to 82% in one week. Gold rallying in that setup means someone is positioning for what comes next. |

Materials stocks outperformed the S&P 500 by 5% this week. XLB rallied 6%. |

When materials lead during a rally, institutions aren't chasing momentum. They're rotating into defensive positioning. |

Market signals are everywhere. The volume on SPY is the easiest way to confirm it. |

Tuesday's volume came in at half of the previous Friday's level. That's not holiday trading. That's liquidity disappearing. |

The VIX 3-month to 1-month ratio is knocking on the door of 1.20. That's the same extreme we saw on October 27th, right before the market corrected 5%. |

Skew sits at 1.45. When that indicator rises, hedges are being put on. |

Now, here's where it gets interesting. The Ghost Prints Console flagged institutional hedging activity in the exact sectors still rallying. |

Let me show you what that means and why it matters. |

Understanding Delta: The Language of Market Maker Hedging |

When institutions buy or sell options, market makers take the other side. But market makers don't want directional risk. They want to collect the spread and stay neutral. |

To do this, they hedge using the underlying stock. |

Delta measures how much an option's price moves for every $1 change in the stock price. You can think of delta as the equivalent number of shares the option controls. |

A call option with a 30 delta acts like owning 30 shares of stock. A put option with a 30 delta acts like shorting 30 shares. |

When a market maker sells a put option to an institution, they're now long delta (bullish exposure). To neutralize that risk, they sell shares short to get back to zero. |

Here's what the Ghost Prints Console caught this week: |

QQQ: 27,000 put contracts traded in a single block. Someone rolled from $585 strikes to $605 strikes. |

|

That's a move from a 12 delta hedge to a 30 delta hedge. |

Translation: institutions just increased their downside protection by 150% while the market was rallying. |

XLP (Consumer Staples): 3,000 put contracts hit the January $77 strike after the sector rallied 3% in a week. |

|

When institutions hedge both tech (QQQ) and defensive sectors (XLP) simultaneously, they're not protecting against a specific sector risk. They're protecting against broad market two-way action. |

Now, let's connect this to the trade opportunity. |

Why Biotech Is the Most Vulnerable Sector Right Now |

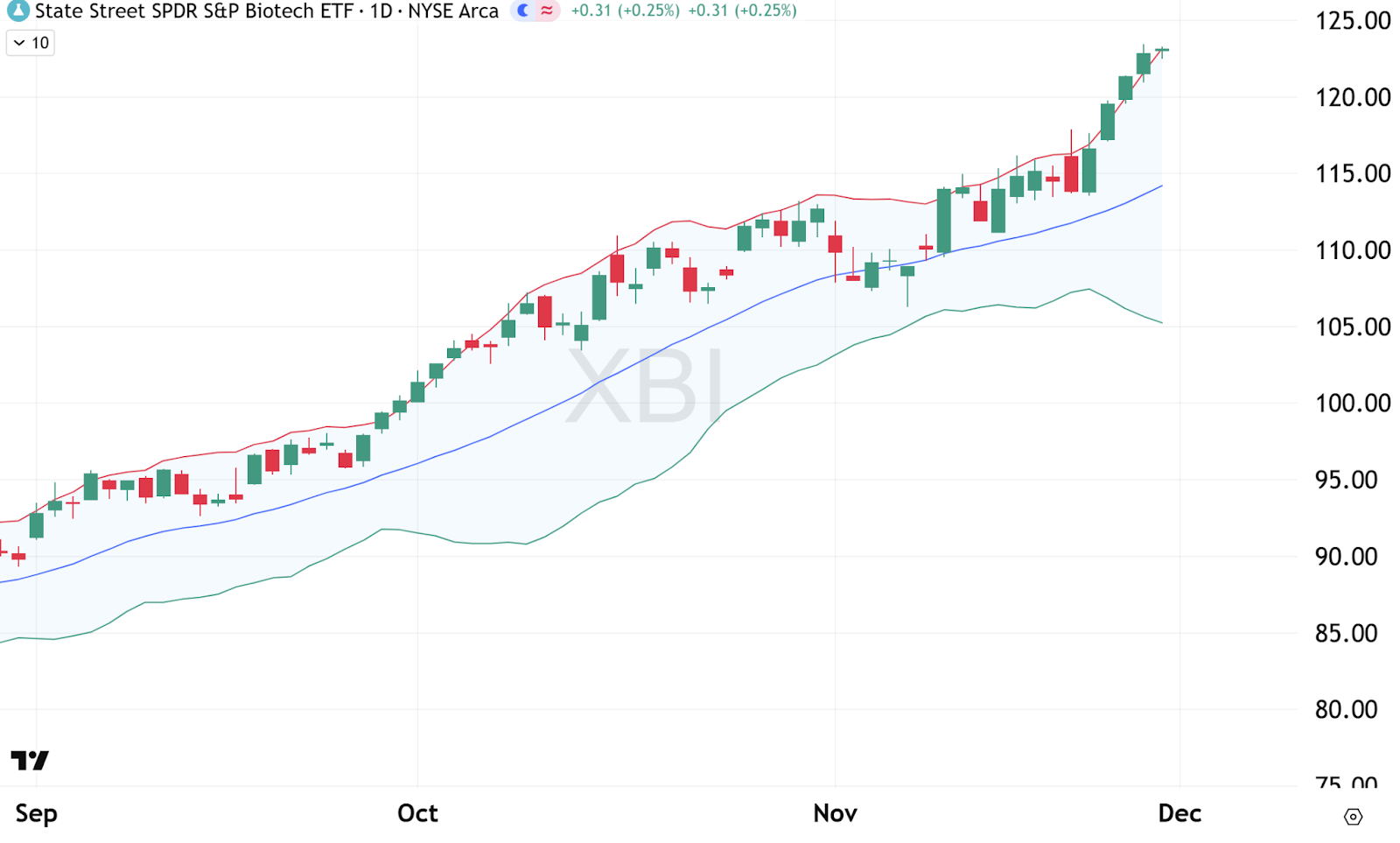

Biotech has exploded higher over the past week. XBI rallied from $107 to $123 in just four trading days. |

That's a 15% move in a sector known for volatility, but this move came with a specific pattern that creates opportunity. |

|

XBI traded above the upper Bollinger band for four straight days. |

For those unfamiliar, Bollinger Bands measure standard deviation. When price trades outside the bands, it means the stock is making a statistically extreme move. |

One day outside the bands can happen. Four consecutive days is rare. |

Here's what makes this setup compelling: institutions are aggressively hedging the broader market while biotech remains the most extended sector. |

XBI currently trades at $123. The recent low sits around $95. |

A 50% retracement of that move would take XBI back to $109. That's only an 11% pullback from current levels. |

But we don't need an 11% move to profit. We just need a modest reversion. |

The Trade Structure: How to Use a Put Spread |

Most traders avoid put options because they're expensive, especially on extended stocks with elevated implied volatility. |

That's where a put debit spread becomes useful. |

Here's the structure: |

|

Let me break down what this means. |

When you buy a put spread, you're buying the right to sell XBI at $120 (the long put) and simultaneously selling someone else the right to sell it to you at $118 (the short put). |

Your maximum loss is the $80 you paid to enter the trade. This happens if XBI stays above $120 at expiration. |

Your maximum profit is the width of the strikes minus your initial cost: ($120 - $118) - $0.80= $1.20, or $120 per spread. |

This happens if XBI trades below $118 at expiration. |

But we're not holding to expiration. We're targeting 70% of the maximum profit. |

Here's why that matters. |

Why 70% Is the Right Target |

Put spreads behave differently from single puts because you're working with two options moving in opposite directions. |

When you buy the $120 put and sell the $118 put, you're creating a position with defined profit potential. |

As XBI drops, your long $120 put gains value faster than your short $118 put. The closer XBI gets to $118, the closer your spread gets to its maximum value of $2.00 (the width between strikes). |

But here's the key: the final 30% of profit requires the most movement. |

Think of it like this: getting from $0.80 to $1.64 (70% of max) might only require XBI to drop to a few percentage points. |

Getting from $1.64 to $2.00 (the final 30%) requires XBI to fall a whole lot more or wait until we're near expiration. |

That's because as your spread moves deeper in-the-money, both options start behaving more like the stock. The delta difference between them narrows, slowing your profit acceleration. |

At 70% of max profit, we're capturing $84 in profit on our $80 initial investment. |

Why This Trade Works When Institutions Are Hedging |

The institutional put buying in QQQ and XLP tells us something critical: smart money expects volatility, not a straight-line rally into year-end. |

When market makers sold those puts to institutions, they had to hedge by selling the underlying stocks. That creates subtle selling pressure even as prices rally. |

Biotech, meanwhile, carried none of that hedging activity. It's pure momentum with no institutional protection underneath. |

That makes it the most vulnerable sector when the market gets two-way action. |

The other factor working in our favor is mean reversion. XBI makes extreme moves regularly, but those moves tend to snap back faster than broad market indices. |

Four days above the upper Bollinger band is statistically extreme. Reversion to the mean doesn't require a bearish thesis. It just requires normal market behavior. |

Why Ghost Prints Subscribers See These Setups First |

Most traders see a sector rallying and assume they missed the move. |

Ghost Prints subscribers see institutional positioning that contradicts the surface action. |

The Console caught the QQQ and XLP put activity before anyone was talking about hedging. It flagged the exact delta levels institutions were targeting. |

That's the difference between reacting to price and anticipating the next move. |

I'll walk through several similar setups live on Monday's Ghost Hour at 11:30 EST. |

You'll see how to identify institutional hedging in real-time, structure spreads that capture mean reversion without overpaying, and manage positions as volatility develops. |

The market just shifted into defensive positioning while prices keep rallying. The question is whether you're trading the setups with the most extreme divergence. |

Register for Monday's Ghost Hour Session |

Brandon Chapman, CMT

Creator of Ghost Prints |

0 Response to "How to Fade the Biotech Squeeze"

Post a Comment