You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. This Map Tells Us Everything Wrong with FinanceThe cracks in private credit will be made worse today by a rising dollar and a possible race to cash as nations battle for dollar-denominated assets.Editor’s Note: I wrote this on Friday as I’m currently (I assume, hope?) coming out of a routine medical procedure. I couldn’t quite spend this morning on the Iran situation, commodities, or anything else related to it. However, I did produce about a 40-minute presentation last night on Iran, scenarios, and what it means for food, fertilizer, oil, and much more. If you want to check it out, it’s available right here…

Dear Fellow Traveler, As I said on Monday morning, the markets face a problem beyond Iran. A rising dollar is an issue because it’s the primary currency used to price and settle trade in oil and many global commodities. As worries surge about oil prices, the dollar can strengthen as energy importers need the dollar to purchase and settle oil deliveries. In addition, foreign investors may rush to the dollar during periods of financial stress or when global funding tightens… also creating demand and thus a stronger dollar. Then there’s the impact of a stronger dollar, given what the dollar really is. The dollar functions as the world’s most important settlement instrument for debt. It says so on the paper money in your pocket. “This note is legal tender for all debts, private and public.”

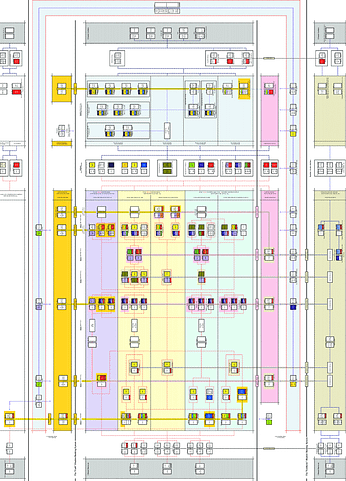

That’s a diplomatic way to tell the People of Earth that the dollar is what they need when it’s time to pay the tab… In a world awash in dollar-denominated debt, it’s the dollar that must be held to pay off that debt… or refinance that debt. That fundamental truth - simple as it is - creates new problems around liquidity… and can help trigger a bigger credit problem in time. With private credit currently facing redemption challenges and massive amounts of refinancing across commercial real estate, leveraged loans, and private credit in 2026, the dollar itself continues to find support thanks to the reserve system and its dominance in global finance… I mention this because it raises the stakes on the private credit front - and opens up questions about the U.S. and its refinancing needs this year. A liquidity crisis can trigger a credit event if there isn’t enough access to what’s required for refinancing… And that’s where today’s story asks a simple question. What the hell am I talking about? The Shadow Bank RoadToday, we want to talk about refinancing and the shadow banking system… Let’s go back to the original gangster in this storytelling… In 2010, a researcher at the New York Federal Reserve, Zoltan Pozsar, published "Shadow Banking," Federal Reserve Bank of New York Staff Report No. 458. He drew a map of the entire shadow banking system. It tracked every entity, funding flow, and step in the chain where credit moves from one institution to another… outside the traditional banking system. The map looks like a wiring diagram for a building that is already on fire.

His paper showed, in the obsessive detail only a person with ADHD like me would love, how this parallel financial system had grown to $22 trillion in assets by 2007... That figure was roughly comparable to, and briefly larger than, the traditional banking system you and I knew, centered on business loans and deposits. This “shadow system” process transforms short-term funding into long-term loans. And when confidence disappears, the whole thing can collapse within weeks as it did back in 2008. I’ve explained this system before… But what really matters today is that even after the crisis, Dodd-Frank, after all the hearings and the grandstanding…

Wall Street didn’t shut down the roads. They just added new lanes. And that’s how we got here today. What Shadow Banking Actually WasShadow banking is the activity of non-traditional financial institutions that perform the functions of a bank... They take in money, lend it out, and transform short-term funding into long-term loans... But it all happens outside the traditional regulatory system… In the shadow banking world (like hedge funds, private equity, and private credit), there’s no FDIC insurance, access to the Fed’s discount window, or capital requirements. It’s all the “fun and excitement” of banking… with none of the guardrails.

Before 2008, the shadow banking system included structured investment vehicles, asset-backed commercial paper conduits, money market funds, repo markets, and securities lenders. Don’t know what those are? Neither, it appears, did people who wrote Dodd-Frank… But they should have… Because these weren’t back-alley operations that people didn’t see in the newspaper or on CNBC. They were right out in front… run by the world's largest financial institutions, often as off-balance-sheet elements to avoid regulatory capital requirements. The asset-backed commercial paper market alone hit $1.3 trillion in July 2007. Repo funding financed a large share of the trading books and inventory of the major investment banks. Money market funds held well over $2 trillion (it’s more than triple that today). These were not small numbers... This was the plumbing of the global financial system... And this plumbing had a design flaw that everyone knew about, but nobody fixed. How It BrokeThe design flaw was maturity mismatch... the same concept we talked about in Money Printer 204, just on a much larger scale. Shadow banks were borrowing short and lending long. They funded themselves with overnight repo agreements and 30-day commercial paper. They turned around and used this money to buy mortgage-backed securities (MBS). They also bought up structured credit products that matured in years or decades from the time of purchase… The system worked fine if short-term funding was available or the secured overnight funding rate (SOFR) wasn’t blowing out. But then subprime mortgages started to crack in 2007. Delinquencies began to pile up, and lenders began to worry about the consumer's condition. So they started demanding more collateral from the repo market when lending money. This is something known as a “haircut.” If you borrowed $100 against $100 worth of bonds or other assets, you could now only borrow $95, $90, or $80. That type of action has a similar impact to a bank run, but it’s actually happening in the wholesale markets between larger institutions instead of what you would see with depositors lined up at branch windows. In July 2007, Bear Stearns (yes… that firm) had two subprime hedge funds that imploded. The first lost 91% of its value. That was the good one. The other was totally wiped out. Bear Stearns tried to bail them out with a few billion dollars. Investors were told that the subprime impact was under 10%. It was obviously… much, much higher. In September 2008, Lehman Brothers’ Dick Fuld finally lost his fight against reality. His firm filed for bankruptcy… meanwhile, the original money market - known as the Reserve Primary Fund… “Broke the Buck.” The fund, created in 1970, held more than $60 billion, but its share price slumped under $1 because it held commercial paper from Lehman Brothers. Investors yanked out half of the fund’s assets in two days. Almost 30 other money market funds nearly saw their price fall under $1 as well… What followed was a widespread repo funding freeze as private collateral dried up. The shadow banking system lost about $3 trillion in just a few months… Zoltan Pozsar saw this coming because he understood what this system really was… It was a “chain of credit intermediation…” (Drink!) Each link in the chain was funded by the one in front of it. If any of those chain links broke, the entire thing would come apart… It did. What Dodd-Frank Fixed (and What It Didn’t)The Dodd-Frank Act of 2010 was supposed to fix the financial system. It was 2,300 pages long… and I actually read every page while working for an advocacy shop in Washington D.C. That length is why most people in Congress didn’t. The law created new regulatory bodies, added stress tests for banks, created the Volcker Rule, and generally made it much harder for traditional banks to do the risky things they’d been doing… But here’s what Dodd-Frank did not fix... The three things that caused the crisis. It didn’t address structural challenges in money markets. It didn’t address the structural risks in the repo market. And it didn’t fix securitization in any meaningful way. The three things at the center of the shadow banking collapse were left largely intact. What Dodd-Frank did accomplish was making it more expensive for banks to hold risky loans on their balance sheets. Which created incentives for banks not to hold them… and to find new ways to make money off those risky loans. Higher capital requirements meant banks needed more equity against their lending activities… That made different types of lending less profitable for banks. So the lending didn’t stop. It just moved… To a different part of the plumbing… The Road to Private CreditThis is the part where you need to pay attention, because it’s the link between 2008 and everything I’ve written about in the last several issues. When Dodd-Frank made it expensive for banks to hold leveraged loans and risky credit on their balance sheets, banks stopped. That created incentives for a new wave of institutions to do the same thing the banks had been doing... just without the regulation. Guess what they called it? Private credit, baby.

That industry has grown from roughly $40 billion in 2000 to nearly $3 trillion today. Everyone has known the risks of this… The Financial Stability Board monitors global non-bank financial intermediation activities. They reported in December 2025 that the total non-bank financial (NFBI) sector hit $256.8 trillion in assets... or about 51% of all global financial assets. It grew 9.4% in 2024, roughly double the rate of the banking sector. The narrow measure... the part that the FSB considers to have bank-like financial stability risks... is $76.3 trillion and growing at 12% per year. (That is defined as “entities that authorities have assessed as being involved in credit intermediation activities that may pose bank-like financial stability risks.” Sleep well...) The IMF published a warning in April 2024… The title was “Fast-Growing $2 Trillion Private Credit Market Warrants Closer Watch.” The blog post laid out every challenge that Pozsar mapped in the shadow banking system, just in a new wrapper. In private credit, borrowers are smaller and carry more debt than companies with public loans. Valuations aren’t public. The funds mark them internally using “mark-to-model. This means the fund tells us what they say the loans are worth, and we take their word for it… In these funds, we have several layers of leverage. It comes at the fund level, at the borrower level, and in the funding lines that banks provide to private credit funds. The FSB knows that data limitations exist, which means regulators have no real way to completely assess risk… Preqin noted the IMF’s statement that “If private credit remains opaque and continues to grow exponentially under limited prudential oversight, the vulnerabilities could become systemic.” That sentence could have been written about shadow banking in 2006. The only difference is the name. The structure is the same. And the prospectus is nicer… it has an owl on the cover… Same Roads, Different CarsPozsar’s 2010 map outlined a system in which credit flowed through a chain of interests… Each funded itself with short-term borrowing… Each transformed maturity and liquidity beyond regulatory setups… And each was connected to traditional banking that was hard to measure or understand until it was too late. Private credit has those same characteristics today… It takes in investor capital, lends it to companies that can’t get bank loans, holds those loans on its own books at self-assessed valuations, and in some cases offers investors periodic liquidity on assets that can’t be sold quickly. The IMF has flagged trillions in bank exposure to non-bank financial institutions, like hedge funds and private credit funds… Blue Owl Capital... the story I told you in February… isn’t an outlier. It’s the system working exactly the way it’s designed… Meaning, it works until too many people want their money back at once, and then it doesn’t work at all. The shadow banking system in 2008 was roughly $20 trillion. Today, regulators estimate that about $76 trillion of the financial system operates with similar bank-like risks outside the traditional banking system. And we’ve seen that shadow banking is the overwhelming driver of global liquidity in broad markets. The roads Pozsar mapped were paved over and widened. What You Can Do With ThisA reminder… if you have money in any private credit fund, BDC, or “alternative income” product, you need to understand that you are participating in a system that operates outside the regulatory framework created after 2008. This system works as long as liquidity is abundant. When liquidity dries up, the question isn’t valuation. It’s whether the exit door exists. Protections you might assume exist... deposit insurance, capital requirements, regulatory oversight of valuations... don’t apply to your investment. If you hold bond funds in your retirement accounts, check the fund’s exposure to private credit. Many “core bond” and “total return” funds have been adding private credit exposure to boost yield. That exposure carries risk that traditional bonds don’t… And read Pozsar’s original paper if you have the stomach for it. I did… and now I won’t shut up about it… Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "This Map Tells Us Everything Wrong with Finance"

Post a Comment