Thanks for signing up for DividendStocks.com! It's the daily newsletter built for dividend and income investors. Before we can begin sending your daily updates, there’s one quick step left. Please confirm your subscription using the link below so our emails reach your inbox. Click Here to Confirm Your Subscription to DividendStocks.com Here’s a small glimpse of what you’ll get access to: Dividend Stock Ideas — Each newsletter features dividend stocks with high yields, sustainable payouts, and strong growth potential. Ex-Dividend Stocks — Want to capture upcoming dividend payouts? Find out which stocks are going ex-dividend this week. Market News and Events — Stay in the loop on the latest developments impacting popular dividend names like AT&T, Exxon Mobil, IBM, Procter & Gamble, and Verizon. Bonus: As a thank-you for confirming, you’ll also receive a free PDF copy of Automatic Income, our popular guide to building wealth through dividend investing. Let’s get your dividend journey started! Discover Top Income-Generating Stocks Here See you in your inbox soon,

The DividendStocks.com Team P.S. Don’t miss out click here to verify your subscription and secure your daily dividend insights and your free investing guide!

This Week's Exclusive News

TJX Companies Fires on All Cylinders With 9% Revenue GrowthReported by Thomas Hughes. Posted: 5/21/2026.

Key Points

- TJX Companies is on track to hit fresh highs and continue advancing as cash flow and capital returns underpin price action.

- Off-price business is hot, and TJX expects strength to persist this year.

- Analysts and institutions show high conviction and accumulated shares ahead of the Q1 earnings release.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

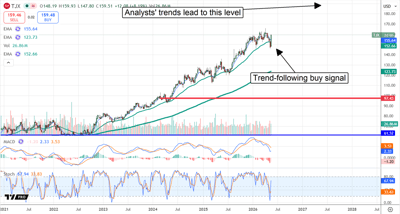

TJX Companies' (NYSE: TJX) uptrend has limits, but those limits have yet to be reached. Accelerating business, dividends, and share buybacks suggest the uptrend will not only continue but may even accelerate in the second half. The company recently increased its share buyback authorization, giving investors added confidence in its future. As of the end of Q1, TJX had completed only 20% of its new fiscal-year 2027 (FY2027) goal, and the share count was down 1% year over year (YOY) and year to date. That offers meaningful leverage for investors who already have several reasons to own the stock. TJX Companies Is in Demand: Consumer Trends Are Strong for This Retailer

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost. Get the SpaceX infrastructure stock name and ticker here

TJX Companies had a solid quarter, with results reflecting both consumer strength and the pressures shoppers continue to face. While inflation is limiting some retailers, consumers are flocking to off-price names, and TJX remains the leader. The company reported $14.32 billion in quarterly revenue, up more than 9% YOY and more than 200 basis points above expectations. Strength was seen across all segments, led by a 9% gain at HomeGoods, a 7% increase in Canada, and a 6% gain in the core U.S. market. Comparable sales, a key measure of organic growth, increased 6% across the network, well ahead of management's forecast. The company’s deal quality and store traffic were reflected in the margin profile. TJX widened gross margin by 180 basis points (bps), pretax margin by 170 bps, and GAAP earnings by 2,900 bps, 1,900 bps better than MarketBeat’s reported consensus. Looking ahead, management expects these strengths to continue and raised guidance. The only issue is that Q2 and FY2027 guidance came in slightly below market expectations, but that does not appear to be bothering investors. The trends, including comparable-store growth and store count, suggest the guidance is conservative and that further outperformance is likely. Executives forecast 2.5% comparable-store growth in Q2.

TJX price action surged more than 5% following the earnings release, signaling support at the $150 level. The move was strong, confirming a support target identified earlier this year and a trend-following entry point for investors. The likely outcome is that this stock will continue to rise, potentially crossing a critical threshold by midyear. That threshold is its existing all-time high, which could trigger many market participants to buy or add to positions. TJX shares could quickly move into the $170 range in that scenario and then continue trending higher in subsequent quarters. Long-term forecasts suggest as much as 100% upside over the next three to five years. TJX Balance Sheet Strengthens in Q1: Shareholder Value ImprovedTJX Companies' balance sheet reflects the strength of its position and Q1 cash flow. The company’s cash, receivables, inventory, and assets all increased, while debt declined, despite aggressive capital returns. The dividend is nearly as attractive as the buyback, yielding approximately 1.2% as of late May, with further distribution growth expected. The payout ratio remains manageable at only 35% of earnings, and dividend growth has held at a respectable double-digit pace in recent years. The pace of increases will likely slow in the years ahead, but not stop, keeping this Dividend Champion on track to eventually be crowned a Dividend King. Institutions and analysts show strong conviction in this investment. MarketBeat tracks 25 analysts who rate it a Buy, with unanimous support, while institutions own more than 90% of the stock. The consensus forecast suggests only modest upside, but the revision trend is bullish and points toward $200, with room to continue improving as the year progresses. Institutions were reducing shares early in 2026, helping to cap gains, but shifted back to an accumulation posture in early Q2, reinforcing support at the key price level. TJX Fires on All Cylinders in Fiscal Year 2027TJX Companies' biggest risks this year include rising fuel costs, increasing inventory levels, and a high valuation. Rising fuel costs could pressure profitability, but that has not yet shown up in results or guidance. Increasing inventory levels may also pressure margins if markdowns rise, but that is not evident in the report or outlook. High valuation is a more immediate concern, since execution will be critical. Even so, the stock’s 29X current-year earnings multiple is average for this market. The takeaway for investors is that TJX is firing on all cylinders in 2026, with signs of growing momentum. It is taking share from competitors, including Target (NYSE: TGT), which continues to struggle with its turnaround efforts. |

0 Response to "Dividend Income Update"

Post a Comment