Ticker Reports for February 13th

Honeywell's Breakup: Is HON Stock a Sweet Deal for Investors?

On February 6, 2025, Honeywell announced plans to fully separate its Automation and Aerospace Technologies divisions. This follows its earlier decision to spin off its Advanced Materials unit. However, the push for a full breakup was largely driven by activist investor Elliott Investment Management. The firm took a $5 billion stake in November 2024, pressuring the company to unlock shareholder value.

Once the split is complete, which is expected in 2026, investors will hold shares in three distinct business units encompassing aerospace stocks, materials stocks, and technology stocks. Honeywell aims to create stronger, more focused businesses that can grow independently. This mirrors GE’s approach when it announced its own breakup in 2021. That restructuring resulted in three separate companies: GE Aerospace, GE HealthCare Technologies Inc. (NYSE: GEHC), and GE Vernova (NYSE: GEV), which oversees its renewable energy operations.

Traders Sell, Analysts Indicate Caution

HON stock fell roughly 6% on the news, extending its losses in 2025 and pushing the stock below its 250-day simple moving average. From a technical standpoint, the stock appears oversold at these levels.

However, the drop was primarily linked to the company’s fourth-quarter earnings report. While Honeywell delivered strong headline numbers, a deeper look at the results suggests another reason for the split. The company reported earnings per share of $2.47, which was higher than the $2.37 analysts expected. Revenue came in at $10.09 billion, beating estimates of $9.83 billion. Despite these strong numbers, most of the company’s growth in 2024 came from the aerospace division, while other segments struggled. The separation could allow the aerospace unit to grow without being weighed down by slower-performing divisions.

This raises questions about the near-term outlook for HON stock. The full breakup will not be completed until 2026. The Basic Materials spinoff is expected in 2025, but investors who buy in now will need a long-term perspective to benefit from the restructuring.

That means looking at Honeywell’s forward guidance, which was cautious and may hint at the rationale behind the split. Management and activist investors may see the conglomerate as too complex to manage effectively as a single entity.

For income-focused investors, Honeywell’s dividend yield of 2.18% and annual payout of $4.52 per share may provide a reason to hold onto shares. Analysts currently rate the stock a Moderate Buy with a consensus price target of $248.71, representing a 19% upside. However, several analysts have lowered their price targets since the earnings report, with some falling below the consensus.

What’s Old Is New Again

It remains to be seen whether Honeywell’s breakup will achieve its intended goals. However, the decision to spin off its aerospace division follows a pattern seen with companies like GE and Lockheed Martin, which have restructured in recent years.

This marks a shift from the decades-long trend of consolidation in the aerospace industry. Many of the same companies that once sought diversification now see greater value in a more focused approach.

For GE, the strategy has paid off. Its stock is up 47% in the past 12 months and 23% in 2025 as of February 11.

Honeywell is hoping for similar success. However, investors will be watching closely to see if the move truly unlocks more value or simply reshuffles the company’s existing challenges.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

When these candles turn green, pay attention

Experts are calling it the best buy/sell indicator of 2024…

A finance whiz from northern Florida has coded an indicator that isolates the precise dates to buy in and out of the stock market.

According to the creator, it allows him to ride all the market highs yet sidestep the lows.

And for the first time ever, he's sharing his indicator with the public.

As you'll see in today's free trading session, you simply buy when the candles turn green and sell when they turn red.

PayPal: Time to Strike With Shares Down Double Digits?

Payments giant PayPal (NASDAQ: PYPL) has had an unimpressive start to 2025, based on the returns of the stock. However, some argue it is unjustifiable for the stock to be down nearly 11% as of the Feb. 12 close. Differences in opinion largely stem from what investors took away from the company’s latest earnings report on Feb. 4.

The financials stock beat on revenue and adjusted earnings per share (EPS), yet shares fell over 13% in one day. Does this mean there is now a prime buying opportunity in PayPal stock, or is the drop a sign of things to come? I’ll break down the key points of contention in the report and answer this ultimate question.

Earnings: Good News on the Top and Bottom-Line

On the top line, PayPal's revenue grew by 4% in Q4 2024 compared to Q4 2023. Its nearly $8.4 billion in revenue was about 1% higher than analysts surveyed by FactSet expected. Additionally, the company’s $1.19 adjusted EPS was 6% higher than anticipated. The midpoint of both Q1 2025 and full-year 2025 adjusted EPS also came in significantly above forecasts. Lastly, PayPal’s Board of Directors approved a large $15 billion share buyback program, which is often seen as a positive for shareholders. So why, then, did PayPal shares retreat so significantly after the release?

Breaking Down Underlying Metrics Causing Trepidation

Much of the concern revolved around a key part of the business: branded checkout. This is where online sellers provide consumers with a PayPal-branded checkout option when making a purchase. Customers who already have a PayPal account can simply click a few buttons to make the purchase. This prevents them from having to enter lengthy credit card information, which may prevent them from purchasing at all.

The value add is that sellers complete more sales, increasing revenue even though they must give PayPal a cut. Branded checkout payment volume growth of 6% was lower than hoped. PayPal’s Chief Executive Officer called branded checkout the company’s “number one priority” in early 2024. Thus, failing to meet expectations on this metric shows the firm’s execution isn’t up to par on a key goal. However, it's important to note that branded checkout volume still grew at a solid 6% clip, an acceleration from 5% in Q4 2023.

Another important focus was PayPal’s unbranded payment processing, known as Braintree. It fell from 29% growth to just 2%. However, profitability improved. The company is letting customers who aren’t profitable go, improving margins at the expense of growth. PayPal expects merchant renegotiations to improve Braintree margins by 1% in 2025 while hurting revenue growth by 5%. The company is boosting margins by advocating for the value of its extra services beyond payment processing in negotiations. Given the difference between margin benefit and revenue growth, this is clearly a strategy that is going to take a while to pay off.

Final Thoughts on PayPal's Opportunity

At this point, the market clearly seems to be prioritizing growth over the profitability strategy that PayPal is pursuing. The gap between PayPal and market priorities suggests that PayPal shares may face short-term downside.

However, one thing that PayPal has that is difficult to ignore is very strong free cash flow generation. It plans to generate $6.5 billion in free cash flow in 2025. That gives it a forward price to free cash flow ratio of just under 12x as of the Feb. 12 close. That’s much cheaper than most of its competitors, but it is also growing much slower than companies like Affirm (NASDAQ: AFRM). This leads to concerns over the company’s competitive position. Still, the company maintains a massive lead in market share, according to data from Statista.

I think PayPal stock represents a solid risk-reward opportunity at this point. The company's strong position feels overlooked. Its focus on long-term profits is causing an overreaction to short-term growth-reducing headwinds. The company’s Investor Day is an important event. It will provide details on the progress of its strategy. It could also showcase new and exciting initiatives.

Overall, there was a mixture of Wall Street analysts lowering and raising price targets after the company’s earnings call. Among four price target updates tracked by MarketBeat, the average was a target of $97 per share. The implied upside of this average comes in at 27%.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

Buy NVDA Now?

After weeks of volatility, did President Trump just turn Nvidia (NVDA) into a raging BUY?

The beloved chipmaker has struggled this year, facing increased competition and regulatory pressure.

Double-Digit Gains Ahead? These 2 Cybersecurity Stocks Look Ready

Fortinet (NASDAQ: FTNT) and Cloudflare (NYSE: NET) are two cybersecurity stocks poised for double-digit gains in 2025. They are poised for double-digit gains because of their differentiated positions in a rapidly growing market, utility to clients, 2024 results, 2025 guidance, cash flow, and analysts' sentiment.

Regarding the market, cybersecurity stocks are supported by the dual tailwinds of businesses' widening use of digital and increased exposure to cyber threats.

Estimates vary, but generally agree that cyber attacks are thriving, with many categories up triple digits in 2024. Along with the increase in attacks is the increase in cost, time to mitigate, and lingering impact on operations. The bottom line is that businesses need digital technology to operate and compete in today’s world; it is central to efficiency and growth, and cybersecurity is part of the package.

Fortinet and Cloudflare both serve businesses and organizations but in different ways. Fortinet’s forte is network security, including firewalls and endpoints, while Cloudflare is a cloud-based service focused on websites.

It helps improve performance and site speeds via numerous security features, including DDOS and DNS attack protection and hackers.

Both are user-friendly, unified platforms powered by proprietary technologies and may be integrated into a comprehensive security package for businesses and enterprises.

2024 Was Good for Cybersecurity Business, Guidance for 2025 is the Same

Cloudflare and Fortinet had solid 2024s, capped off by strong performance in Q4. Each produced high-double-digit growth, with Fortinet accelerating to 17% and Cloudflare sustaining its high-20% pace. Business drivers include strength in services and product segments, significant growth in large clients, and deepening service penetration. Margin news is also good, with earnings growth accelerated and outperforming MarketBeat’s reported consensus figures despite increased share counts.

Guidance for 2025 includes an expectation for growth to slow but sustain at high-double-digit paces. Margins are also expected to remain strong, driving robust cash flows. Cash flow margins hit record highs in 2024 and are central to the long-term stock price outlook. These companies are heavily reinvesting in product development and new technology today, but they are also improving cash flow and are on track for capital returns. At the end of 2024, the balance sheet highlights include increased cash, securities, current, and total assets, which are only partially offset by increased liability. Equity is rising, turning positive in the case of Fortinet, and leverage is low. Fortinet is net cash, and Cloudflare is nearly so, but it is only expected to improve.

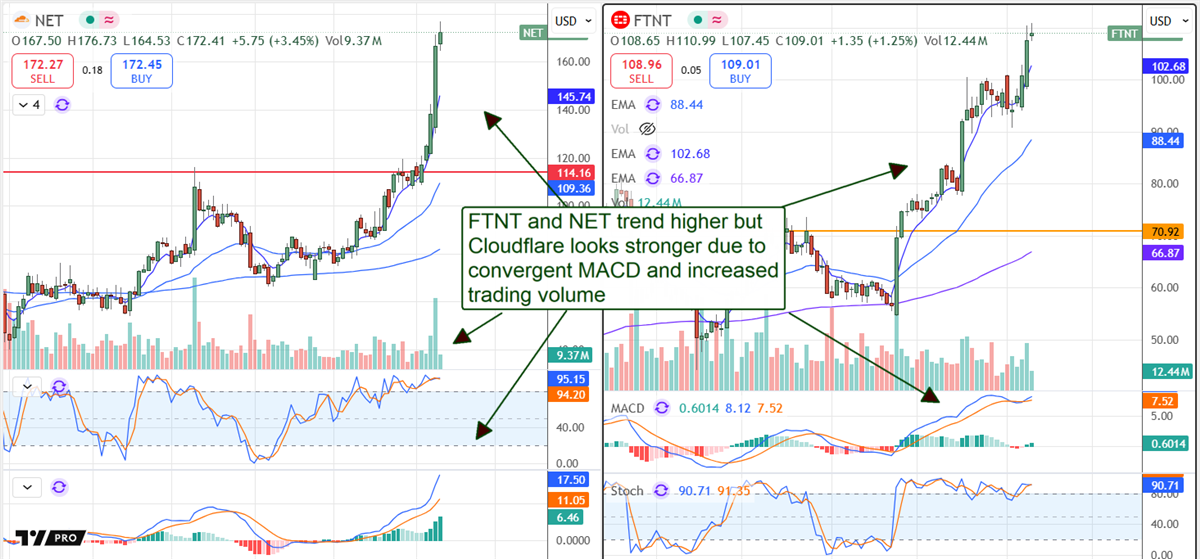

Cloudflare, Fortinet Analysts Lift Price Targets After Q4 Results

Analysts were catalyzed by Cloudflare’s and Fortinet’s Q4 results, lifting their price targets in response. The consensus targets for these stocks lag their stock price action in mid-February but are up by double-digit amounts in the week since their reports, with the freshest targets leading to new highs. They put these stocks up another 35% to 45% in 2025.

The price action is favorable. Both stocks are trending higher, although Cloudflare's market looks stronger. Its uptrend is accompanied by a convergent MACD, not a divergent one, indicating market strength and a higher probability the uptrend will continue. Cloudflare's chart also includes a conspicuous volume spike, making it the better choice for near-term oriented trades and investments. Fortinet's market has divergent momentum and may lag Fortinet in price performance.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 PayPal: Time to Strike With Shares Down Double Digits?"

Post a Comment