Despite beating forecasts, why did Visa's shares fall after its latest earnings? The firm sees big opportunities in Visa Direct and in a key... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Leo Miller

Visa (NYSE: V) is a dominant player in the worldwide payments industry, and even amid macroeconomic difficulties, the stock has delivered impressive performance in 2025 so far. As of the July 29 market close, Visa shares have provided a year-to-date (YTD) total return of more than 11%, moderately surpassing the approximately 9% total return of the S&P 500 Index. However, the company’s July 29 earnings release weighed on the stock. Although the firm beat expectations on both sales and earnings in the quarter, V stock fell by 2%-3% in after-hours trading. So, what caused markets to sell the stock after the results? And how does this impact Visa stock going forward? Mixed Signals: Strong Earnings, Cautious Outlook In its fiscal Q3 2025 results, Visa reported revenues of just under $10.20 billion, equating to 14% revenue growth. This solidly beat estimates of around 11% growth. The company also noted impressive adjusted earnings per share (EPS) of $2.98, a 23% increase, beating the analyst estimate of 17%. However, Q4 guidance may have been responsible for the after-hours sell-off. The company forecasts “high-single-digit to low-double-digit” revenue growth in Q4, and sees EPS growing in the “high single-digit range." These figures appear to be less than what analysts were hoping for. Payment volume growth, a key business driver, remained solid at 8% in constant currency. It remained stable compared to the prior year quarter and to fiscal Q2 2025, indicating that trade wars are not having much of a negative impact on consumers so far in 2025. Consumer Spending and Global Transactions Still Driving Momentum The company called consumer spending "resilient." As Visa’s payment-driven business thrives on consumer health, this is good news for Visa investors. It is also good news for the overall market since consumer spending accounts for around two-thirds of the U.S. gross domestic product (GDP). The company’s value-added services (VAS) saw robust growth of 26% in constant currency, a solid acceleration from 22% growth last quarter. This is another positive sign, as VAS is also a key growth driver and increases the stickiness of Visa’s platform, helping solidify its market position. Management said VAS is “firing on all cylinders." In general, Visa’s business remains healthy, with strong growth across key verticals, supporting the continued bullish thesis around the stock, as the company is well-positioned to benefit from long-term economic growth. Visa Direct and Stablecoins: How Visa Is Expanding Its Horizons Visa added notable color to two key initiatives, Visa Direct and stablecoins. Visa Direct is the company’s remittance platform. It enables foreign workers to send money back to their families in their home country. Banks and other financial institutions integrate Visa Direct into their platforms. Overall, Visa Direct saw a 25% increase in transactions and added several new banks to the platform during the quarter. The company's substantial progress on this front is key. Visa sees cross-border transactions as a relatively under-penetrated, enormous total addressable market (TAM). Thus, Visa Direct is a way for the company to drive strong growth for an extended period. The company thinks stablecoins will also be beneficial for capitalizing on this opportunity. The firm sees stablecoins as benefiting two key areas. The first is in emerging market economies, where local currencies can be volatile and people have limited access to U.S. dollars. Consumers and businesses may prefer to hold stablecoins tied to the U.S. dollar or euros, helping their money maintain its value. To capitalize on this opportunity, Visa is expanding its offerings of stablecoin-linked cards. The company is working to integrate stablecoins into Visa Direct. While Visa Direct often works well on its own, stablecoins can occasionally facilitate faster cross-border money movement. Early testing results have been good. Where Opportunity Lies, Visa Finds It Despite the drop in shares after hours, Visa remains a hard stock to bet against. Its long-term strength lies in its global scale, technological readiness, and forward-looking strategy. By combining resilient core payment demand with innovation in tokenization and stablecoin-enabled services, the company is expanding its addressable market while reinforcing platform loyalty. The conservative guidance may reflect prudence amid macro uncertainties, but it doesn’t undercut Visa’s strategic momentum. As more ways to pay emerge, Visa will likely be there and make money from them, adding significant weight to the finance stock’s bullish thesis.  Read This Story Online Read This Story Online |  Leaked: Jobs' Final Apple Project Exposed

Bloomberg just leaked details of a secret project Steve Jobs set in motion before his death. After more than a decade under wraps, Apple is finally preparing to unleash this breakthrough — one that could reshape a $9 trillion industry overnight. Its secret codename… Project Mulberry. |

| Written by Jeffrey Neal Johnson

Marvell Technology (NASDAQ: MRVL), a company that experienced underperformance and became a favorite among short-selling skeptics through the first half of 2025, has recently demonstrated a significant shift in momentum. Over the past five days, the stock has begun to recover, and in the final days of July, it has shown breakout momentum, signaling an apparent change in narrative. What was once a target for short-sellers has now captured market attention with what looks like the start of a powerful rally. This raises a crucial question for investors: What is driving the shift in market sentiment? For Marvell, the answer lies in a foundation of strong business results, suddenly ignited by a specific, confidence-boosting catalyst. How Strong Fundamentals Paved the Way for a Breakout Before the market-moving headlines of July 30, Marvell had already laid a foundation of strong fundamental performance. On July 24, the company released a preliminary report on its second-quarter fiscal 2026 results, signaling to the market that its business was running ahead of schedule. The full Q2 earnings report is expected after market close on Aug. 27. Management announced it expected revenue and earnings to finish at the high end of its previously guided range, implying revenue approaching or exceeding $2.1 billion and non-GAAP earnings per share (EPS) at or above 72 cents. The company attributed this strength to two key factors. First, demand for its data center products, particularly those related to artificial intelligence (AI), accelerated faster than anticipated. This confirmed that its primary growth engine was performing at a high level. Second, management noted that the long-standing inventory correction in its enterprise networking business was finally showing signs of concluding. The stabilization de-risks the company's financial profile and provides a firmer foundation, allowing Marvell's high-growth AI story to drive overall results. The Catalyst That Ignited the Rally That spark arrived on July 30. The primary trigger for the stock price jump on that day was a bullish sell-side report that, according to market commentary, specifically addressed and increased investor confidence in Marvell's custom-chip relationship with Microsoft (NASDAQ: MSFT). The news directly countered the narrative of doubt that had weighed on the stock. Before the rally, Marvell was known as a favorite short play in some hedge fund circles, with uncertainty around its major customer programs being a primary reason for the skepticism. The positive analyst note directly targeted this concern, effectively neutralizing a key part of the bearish argument. This sentiment shift was accompanied by a tangible market signal from Morgan Stanley, which raised its price target on the stock from $73.00 to $80.00. The market’s reaction was immediate and powerful. After closing the previous day at $76.34, Marvell's stock gapped up at the open, beginning the trading day at $83.11. This type of significant price gap is a classic sign of overwhelming pre-market demand, typically driven by large institutions acting decisively on new information. The high trading volume throughout the day confirmed this was a broad-based move, suggesting a significant re-evaluation of the stock was underway. Why the New Confidence Is Justified The rally did not happen in a vacuum. The company's strong underlying performance fully supports the newfound confidence sparked by the analyst report. The market's strong reaction on July 30 was a direct and logical consequence of investors finally digesting the solid fundamental news revealed just days earlier. This near-term execution fits perfectly within the company's long-term strategic vision. Marvell's goal is to capture 20% of the custom AI chip market by 2028, an objective that would dramatically reshape its revenue profile. The stronger-than-expected preliminary Q2 results and the renewed confidence in its key customer relationships serve as powerful, real-time proof points that this long-term plan is an achievable reality. Further bolstering its strategic position, Marvell recently appointed Rajiv Ramaswami, the current CEO of cloud software leader Nutanix, to its Board of Directors. This move adds a wealth of relevant cloud ecosystem and software expertise to Marvell's leadership, further aligning the company with the needs of its most important customers and strengthening its strategic vision for the future. The Race Is Just Beginning The recent jump in Marvell's stock price represents what appears to be a significant sentiment reversal. A foundation of strong business results, ignited by a specific, confidence-shifting catalyst, has allowed the stock to break free from the skepticism that previously held it back. This positions the company as a potentially undervalued architect of the future of the AI Revolution. Read This Story Online |  Bitcoin just hit a record high—but it's not the top crypto play right now.

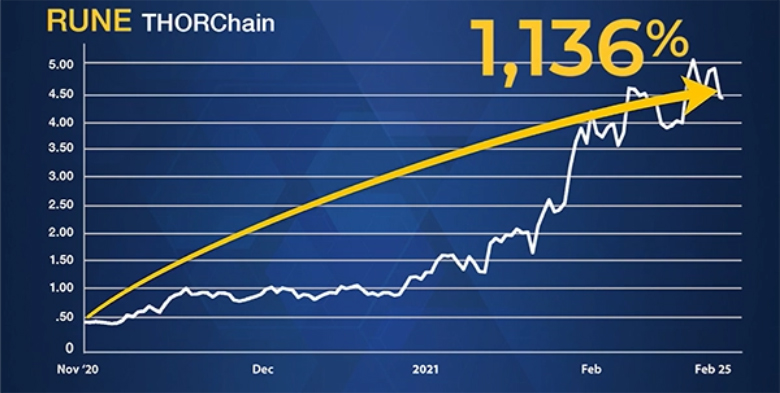

Crypto analyst Juan Villaverde, who called Bitcoin's breakout to $100K nearly to the day, says a lesser-known coin could be even bigger. It's faster, cheaper, and backed by Google, Visa, and top VCs with over $200 million already invested. Get the name of this "third pillar" crypto in Juan's free report → |

| Written by Jeffrey Neal Johnson

The technology sector is in a constant state of transformation. The rapid adoption of artificial intelligence (AI) and the shift to multi-cloud environments have created immense opportunities, but they have also opened the door to a more complex and dangerous generation of cyber threats. For years, enterprises fought back by deploying a patchwork of individual security tools, leading to a complicated and often ineffective defense. Today, that approach is changing. Businesses are now demanding simplification, seeking to consolidate their security with a single, integrated platform. This market shift has created a significant opportunity for a definitive leader to emerge, and Palo Alto Networks (NASDAQ: PANW) is making a compelling case that it will be that leader. Many Tools, 1 Platform: Palo Alto's Winning Formula Palo Alto Networks' core strategy hinges on a concept it calls platformization. The goal is to provide a single, unified platform that can replace dozens of separate security products, giving businesses a clearer and more effective way to manage their defenses. This strategy is built on three main pillars that cover the entire IT environment: - Strata secures the corporate network with its industry-leading Next-Generation Firewalls.

- Prisma protects the cloud, securing everything from cloud applications to remote workers with its SASE (Secure Access Service Edge) technology.

- Cortex powers the modern Security Operations Center (SOC), using artificial intelligence to automate threat detection and response.

This platform approach is being actively executed through strategic partnerships and acquisitions. To dominate the crucial new market of AI security, the company recently completed its acquisition of Protect AI on July 22, 2025. This move directly integrates AI model scanning and runtime protection into its Prisma platform, giving customers a secure way to adopt new AI technologies. Further, a recent expansion of its partnership with identity leader Okta (NASDAQ: OKTA) on July 15, 2025, allows for the unification of security and user identity, enabling automated threat responses that competitors with siloed products cannot easily match. This strategy is gaining traction, with the company securing 19 new platformization deals in its most recent quarter, proving that customers are buying into its unified vision. How Platformization Fuels Growth A successful strategy must translate into strong financial results, and Palo Alto Networks' financials are delivering. The company is proving that its platform-centric model is fueling a successful transition to a more predictable, high-growth business profile. Its Next-Generation Security (NGS) Annual Recurring Revenue (ARR) is the most compelling evidence of this success. This metric, which tracks performance in high-growth areas like cloud security and AI-driven operations, surged 34% year-over-year to reach $5.1 billion as of April 30, 2025. This healthy growth confirms a successful shift from reliance on traditional hardware sales to a more durable software and subscription-based model. This is supported by impressive top-line performance. The company's total revenue grew 15.3% to $2.3 billion in the third quarter of fiscal 2025, beating analyst expectations. Perhaps most impressively, Palo Alto Networks has delivered 12 consecutive quarters of positive GAAP net income, showcasing a rare and valuable combination of high growth and sustained profitability at scale. A Bold Move for Market Dominance A company with ambitions to lead a market must sometimes make bold moves, and Palo Alto Networks appears ready to make its biggest one yet. Recent reports indicate the company is in advanced talks to acquire identity security leader CyberArk for a price that could exceed $20 billion. While the company has not confirmed the deal, such a move would be a decisive step toward creating a truly end-to-end cybersecurity platform. Integrating CyberArk’s best-in-class identity security would significantly widen Palo Alto's competitive moat. While the market reacted with some short-term caution to the rumored price tag, the long-term strategic benefit is clear. The move underscores the company's commitment to its platform vision. This ambition is reflected in the stock's premium valuation, with a price-to-earnings ratio (P/E) that stands above 110. Such a valuation indicates that investors have high expectations for future growth, a belief that appears to be shared by Wall Street. The stock currently holds a Moderate Buy consensus rating from 41 analysts, with an average price target of $209.42. This confidence is rooted in the company's proven ability to execute its strategy and consistently deliver strong financial results. A Compelling Case for a Cybersecurity Leader Palo Alto Networks has established a clear and aggressive strategy to dominate the consolidating cybersecurity market. The company backs its platform vision with decisive acquisitions and partnerships while delivering the impressive financial results needed to prove its success. Palo Alto Networks presents a compelling case as a market-shaping leader with a clear path for continued growth for investors looking for a core holding in the essential and growing technology sector. Read This Story Online |  The Trump economy is back in full force, and it's creating huge opportunities for investors.

With Trump pushing for lower taxes, fewer regulations, tariffs on foreign competitors, and domestic manufacturing dominance, some stocks are set to skyrocket in value—while others will be left behind.

That's why we put together this free report revealing the 7 MAGA stocks poised to thrive in 2025. 🔻 Download the full report now and get the inside track on these 7 powerhouse stocks. |

| More Stories |

| |

|

|

0 Response to "🦉 The Night Owl Newsletter for July 30th"

Post a Comment