Get Ahead with This Free Report! (From Stock News Trends)

DraftKings Posts Record Quarter, Eyes Profitability

Key Points - DraftKings beat Q2 estimates with record revenue and GAAP EPS of 30 cents.

- Management raised full-year revenue and adjusted EBITDA guidance.

- Technical setup and a golden cross suggest a potential breakout ahead.

DraftKings Inc. (NASDAQ: DKNG) reported record revenue and earnings in its second-quarter 2025 earnings report. This was expected, as DKNG stock was up approximately 11% in the month before earnings, and analysts had been raising their price targets. But even investors may have been surprised at the magnitude of the beat on the top and bottom lines. In fact, DraftKings set records in both generating earnings per share (EPS) of 30 cents on revenue of $1.51 billion. The top-line number was 37% on a year-over-year (YOY) basis. A highlight of the report was DraftKings' acknowledgment of higher sportsbook-friendly outcomes. The translation is: more customers lost their bets in the quarter. That worked to the company’s favor. The company also raised its full-year guidance for both revenue and earnings: - The new full-year 2025 revenue guidance is for $4.95 billion to $5.05 billion (previously $4.8 billion to $5.0 billion).

- The new full-year 2025 adjusted EBITDA guidance is for $460 million to $540 million (previously $410 million to $500 million).

Investors should focus on the company’s results, which the company believes put it on track for sustained profitability. Supporting that outlook was a 29% increase in average revenue per user and the YOY growth in iGaming revenue. The hidden fuel behind AI? Your phone.

Billions of data points — from your clicks, swipes, scrolls, and searches — are feeding the next wave of AI innovation.

Big Tech is harvesting it. Mode Mobile is giving it back to you.

They are creating a user-powered data economy that shares the upside, and +50M users have already generated +$325M in earnings.

This isn't a theory… Mode's 32,481% revenue growth from 2019-2022 landed them the #1 spot on Deloitte's 2023 list of fastest growing companies in software, and they've secured the Nasdaq ticker $MODE ahead of a potential IPO. The offering could close any moment now.

AI breakthroughs are everywhere, but these models need your data to survive. Invest in the company that allows you to share in the profits from yours. 🚨Round closing — invest at 0.30/share now. Seasonal Factors Impacted Profit One reason DraftKings was able to book such a substantial profit is that the last quarter didn’t involve football. That may seem counterintuitive, but as the company's CEO remarked to CNBC’s Jim Cramer, DraftKings typically reduces its advertising and marketing spending after the Super Bowl in February. Therefore, more of its revenue can go directly to the bottom line. This has been true for the company since it went public. The second quarter has been profitable, but the challenge is reaching full-year profitability. Like its competitors, DraftKings relies on heavy promotional spending, particularly during the American football season. That results in cash burn, which has held back the company’s share price. The company is seeing continued growth in the number of unique customers on its platform, so the strategy is working. To that end, management is guiding to full-year profitability on an adjusted EBITDA basis. However, that doesn’t mean the next two quarters will be profitable on a GAAP EPS basis. Is Growth Slowing or Stalling? DraftKings continues to see slower growth in iGaming and active users as it expands into more markets. On the one hand, that's typical for any maturing growth company. However, investors may be concerned that the slowdown will show up in weakening engagement numbers. That’s particularly true of iGaming, which has higher margins than sports betting, so any slowdown there could impact DraftKings’ path to profitability. Slowing monthly active user growth can also signal that the company is reaching saturation in early-entry states, putting more pressure on new markets to deliver. DraftKings still trades at growth-stock valuations, so while some deceleration is expected, the company will have to show that this is a natural plateau and not an early sign of deeper issues with market penetration or user engagement. What if you could eliminate all the uncertainty from your trading?

This isn't just a theory—it's a game-changer.

What if, in just seconds, you could pinpoint trending small cap companies?

With a single alert, you'd know exactly when to move—

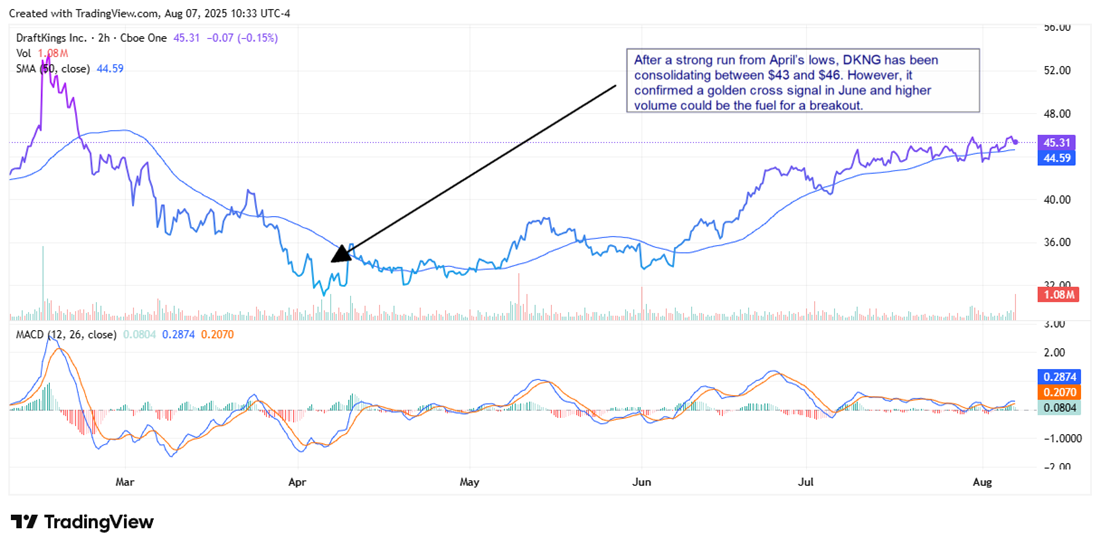

Here's the good news: our team specializes in uncovering hidden gems before the market catches on. 👉 Download Your Free Guide Now No Prediction About Prediction Markets The 2024 presidential election introduced many consumers to prediction markets, allowing them to wager on outcomes ranging from political races to major economic events. DraftKings has since launched its own prediction markets in select states and jurisdictions. However, management has acknowledged that these products may fall under the oversight of the U.S. Commodity Futures Trading Commission (CFTC), which has some investors concerned. In that scenario, the best-case situation would probably require a more complicated licensing process for such wagering. In a worst-case scenario, it would have to shut down these products. To be fair, wagering in prediction markets makes up a small amount of DraftKings' revenue. However, investors were enthusiastic about the company's opportunity to expand beyond sports betting as this kind of innovation would help provide growth opportunities in a highly competitive market. A Golden Cross Signal Could Be a Bullish Setup DraftKings stock is up more than 20% in 2025, easily outpacing other consumer discretionary stocks. It's also trading above its 50-day simple moving average (SMA) at $44.59. That line continues to slope upwards after the stock formed a golden cross signal in May that was confirmed in June, reinforcing the idea that a longer-term uptrend may be underway. However, after a strong run from April’s lows, DKNG has been consolidating between $43 and $46. These earnings results, if supported by strong volume, could be a setup for a move higher. Analysts have given DKNG stock a consensus price target of $54.48, which is 22% higher than its closing price on Aug. 6.

Written by Chris Markoch Read this article online › Featured Articles:

Did you find this article helpful?

|

0 Response to "DraftKings Smashes Q2 Records, Boosts Outlook"

Post a Comment