Robotics is a logical extension of the AI revolution, these three robotics stocks bring AI-driven growth to healthcare, logistics, and... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Chris Markoch

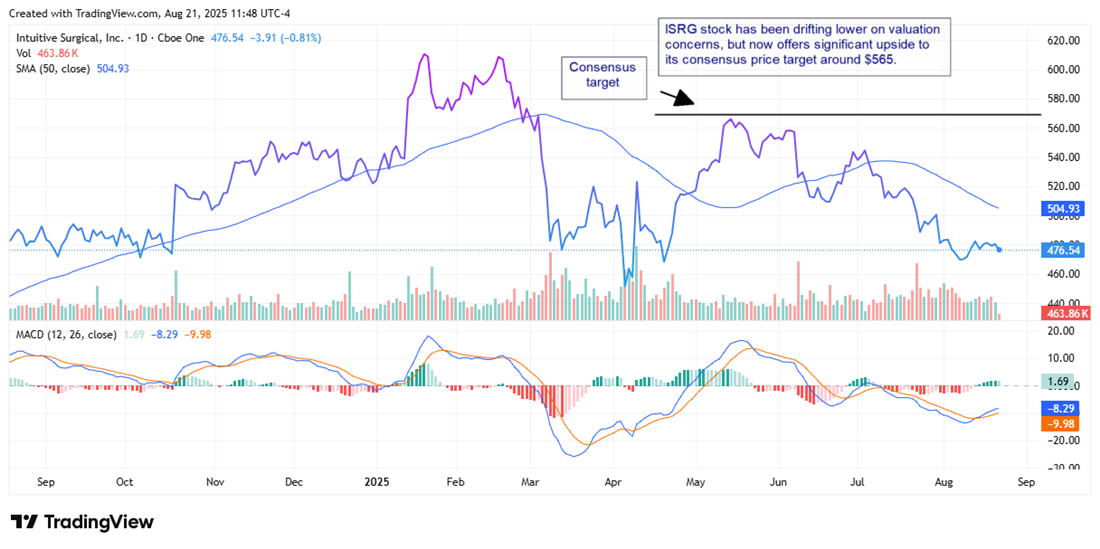

Investors have been looking at robotics companies for several decades. But artificial intelligence (AI) is taking robotics beyond basic automation by bringing more precision, flexibility, and adaptability into the sector. Many investors are choosing to invest in AI infrastructure via hyperscalers (e.g., Meta Platforms, Microsoft) and semiconductor stocks, notably NVIDIA. However, investing in robotics stocks may provide exposure to the next wave of AI with companies that offer unique moats with large total addressable markets (TAMs). Even though many of these stocks may look “cheaper” relative to AI stocks, many come with different concerns for investors to consider. Nevertheless, it’s a sector that merits thoughtful consideration, and here are three robotics stocks that address distinct growth areas. Specialized Exposure with Defensive Qualities Robotics in surgery is one of the most compelling, long-term applications for this technology. Investors know Intuitive Surgical Inc. (NASDAQ: ISRG) as a pioneer in this field. The company’s da Vinci surgical system is the unquestioned leader in this sector with a user base of over 11,000 installed systems worldwide. Intuitive Surgical also benefits from a significant services business that provides annual recurring revenue (ARR) beyond the one-time purchase of a da Vinci system. This ARR is now over 80% of the company’s total revenue. The overlay of AI into the da Vinci system provides surgeons with enhanced vision, precision, and training tools with the goals of shortening procedures and improving outcomes. Intuitive Surgical crushed its last earnings report with strong numbers across the board. That’s not reflected in the stock price. ISRG stock is down 8.6% in 2025 and is down approximately 7% since the report. That isn’t simply due to slower international growth. The likely culprit is a stock that’s valued at around 74x forward earnings. That’s a premium if investors consider the company part of the tech sector, and really expensive if it's classified as a medical stock. It’s also costly relative to its historical average. However, ISRG stock is now trading significantly below the consensus price target of analysts, which is at $565.95 as of this writing. That’s an upside of more than 25%.

Warehouse Robotics Powering the Supply Chain Revolution Symbotic Inc. (NASDAQ: SYM) is another stock pick representing robotics's physical (hardware) side. The company builds autonomous systems that transform warehouses into AI-powered logistics hubs. Walmart, an investor and key customer, gives the company a massive platform as proof of concept and to scale across the broader retail and logistics industries. Symbotic’s fleet of robots can store, retrieve, and organize goods at a speed and accuracy unmatched by human labor, a critical advantage in today’s labor-constrained supply chain environment. Over time, a larger installed base can provide strong recurring revenue from a business model that will resemble that of a software-as-a-service (SaaS) company. That will require significant capital expenses, which is a key reason the company is not yet profitable. That’s one reason for the high short interest in SYM stock, which is over 29% as of this writing. SYM stock has also had two analyst downgrades since its last earnings report, in which Symbotic beat on revenue but came in with negative earnings of 5 cents when analysts were expecting positive earnings per share (EPS) of 3 cents. However, risk-tolerant investors may be comfortable overlooking the cyclical weakness for long-term secular growth.

Bringing AI Into the Office The opportunity in robotics covers both hardware and software. For the latter, investors can consider UiPath Inc. (NYSE: PATH). UiPath is a leader in robotic process automation (RPA), which takes robotics beyond handling physical tasks. The company’s software “bots” streamline repetitive digital processes such as processing invoices, compliance, and HR workflows. The introduction of generative AI into this software allows for adaptive, intelligent workflows (i.e, agentic AI) that move beyond rigid, rules-based automation. UiPath does have strong customer retention with a dollar-based net retention rate (DBNRR) of 108%. However, the company faces growth headwinds in a higher interest rate environment. In this case, it’s not a cost of capital issue but a cost of acquiring new customers when budgets are under pressure. That could change if the economy picks up steam, perhaps fueled by a rate cut or two in the last few months of the year. That acquisition cost is one of the most significant risks to investing in PATH stock. This is becoming a crowded market. However, the chart shows signs that there could be some oversold conditions in play.

Read This Story Online Read This Story Online |  |

| Written by Jeffrey Neal Johnson

A fairly consistent climb in Tilray Brands' (NASDAQ: TLRY) stock price has started to capture the market's attention. After touching a 52-week low of 35 cents, the stock has rallied dramatically, climbing over 133% in the last three months on massive trading volume. This move up, however, is not a simple reaction to the company's latest earnings report; it goes much deeper. While Tilray did post a surprise adjusted profit of 2 cents per share in its fourth quarter 2025 earnings report, that was set against a staggering GAAP net loss of $2.18 billion for the fiscal year. Instead, the rally over the past three months seems to be a signal that investors are beginning to make a calculated, high-stakes bet on a single, sector-transforming catalyst: a pending decision from the U.S. government to reclassify cannabis, a move that could fundamentally rewrite the industry's financial future. Rescheduling: A Tax Revolution for U.S. Cannabis The market's anticipation centers on the U.S. Drug Enforcement Administration (DEA) potentially moving cannabis from its current status as a Schedule I substance to Schedule III. On paper, this is a regulatory shift; in practice, it is a financial revolution for the industry. Currently, cannabis shares a Schedule I classification with drugs like heroin, a category defined by a high potential for abuse and "no currently accepted medical use." A move to Schedule III would officially recognize its medical applications and lower its perceived risk. However, this change's most critical consequence is its effect on Section 280E of the U.S. tax code. This prohibitive rule prevents any business handling Schedule I substances from deducting normal operating expenses from its gross income. For a state-legal U.S. cannabis operator, this means essential costs like payroll, rent, utilities, and marketing cannot be used to lower their taxable income. This results in punishingly high effective tax rates that can exceed 70%, impeding their ability to generate profit and reinvest in their businesses. Rescheduling cannabis would eliminate the 280E burden overnight, instantly improving the financial viability of every U.S. operator and making the entire cannabis sector profoundly more attractive for investment. Why Investors Are Choosing Tilray While the direct tax benefits of rescheduling would apply to U.S. operators, Tilray has become the market's preferred vehicle to trade this catalyst. This is due to a unique convergence of market access, strategic positioning, and financial stability. - Accessibility and Liquidity: With a market capitalization of $1.17 billion, Tilray is easily traded by a global pool of investors. Its high average daily trading volume, often exceeding 40 million shares, allows for the efficient movement of capital, a feature that many U.S. multi-state operators that trade over-the-counter (OTC) cannot offer.

- The U.S. Optionality Strategy: A financially healthier U.S. cannabis market directly increases the value of Tilray’s long-term growth plan. The company has strategically built a U.S. infrastructure through its beverage alcohol segment, now the 5th largest craft brewer in the nation with $240.6 million in annual revenue, and its wellness division, which brought in $60.5 million. This platform is designed to serve as a springboard for THC products as soon as federal laws permit, creating a halo effect where a stronger U.S. market amplifies Tilray's future potential.

- A De-Risked Vehicle: In a sector known for high debt, Tilray presents a more stable profile. The company holds over $256 million in cash and has made approximately $100 million in debt repayments, strengthening its balance sheet. This stability, combined with a high short interest of over 17% of the float, also makes it a focal point for volatility, attracting traders betting on a potential short squeeze if a positive announcement is made.

Where Strategy Meets Speculation The market's enthusiasm for Tilray represents a moment where a powerful external catalyst is amplifying the value of the company’s internal business strategy. While the current Wall Street consensus remains a Hold, the average analyst price target of $1.92 suggests a significant upside from its current level, reflecting the potential impact of a favorable regulatory outcome. This optimistic sentiment is mirrored by those closest to the company. Recent filings show that CEO Irwin D. Simon and CFO Carl A. Merton have been purchasing shares on the open market, investing their personal capital and signaling strong conviction in the company’s direction. Ultimately, Tilray's stock has become a primary barometer for U.S. cannabis reform. The recent rally is fueled by anticipation but is grounded in a catalyst with the potential for fundamental, industry-wide financial transformation. The final decision from the DEA remains the key variable that will determine whether this powerful momentum is sustained and converted into long-term shareholder value. Read This Story Online |

On September 17th, the Fed faces an impossible choice—and Wall Street insiders are already preparing for the fallout. Whether Powell hikes or cuts, both paths lead to wealth destruction for unprepared investors.

American Alternative Assets just released the Mar-A-Lago Accord, revealing how elites are positioning ahead of the decision—and how you can do the same.

Click here to get the free guide and protect your savings before the Fed acts. |

| Written by Sam Quirke

Shares of tech giant Amazon.com Inc. (NASDAQ: AMZN) have been trading a little softly this week, slipping about 2.5% from last Friday's high. However, what's important is that the stock remains more than 7% higher from the start of the month, when some post-earnings profit-taking briefly pulled it lower. And what matters even more now is that momentum appears firmly back in the bull camp, with a major technical signal having just started to flash green. For those watching from the sidelines, this could be the perfect entry point ahead of a rally into the autumn. Let's jump in and take a look. Why the MACD Crossover Matters The moving average convergence divergence (MACD) indicator measures the relationship between two moving averages of a stock's price, most commonly the 12-day and 26-day exponential averages. When the shorter average crosses above the longer one, it indicates that recent price action is accelerating upward compared with the longer trend. Traders then watch the MACD line against its nine-day signal line. A move above it is called a "bullish crossover," a classic sign that momentum is shifting back in favor of buyers. That is precisely what happened for Amazon late last week. The bullish crossover often confirms that short-term weakness has likely run its course and buyers are stepping back in. This is about as clear as they come for investors who have been watching closely and waiting for a technical entry point. The Fundamental Backdrop: Amazon’s Growth Justifies the Premium It should go without saying that technical signals alone are rarely enough to justify diving into a stock headfirst. What makes Amazon's current setup attractive is that the MACD is flashing green amid strong fundamentals. Take the company's most recent earnings report, for example, it topped Wall Street expectations across the board, and showed its key AWS unit growing at an impressive clip. Valuation will almost always form part of the debate too, and with a price-to-earnings (P/E) ratio of roughly 35, the stock is not the cheapest of the mega-caps. Yet Amazon has rarely traded like a value stock, and its investors have always been happy to pay a premium for its growth potential. Add in the fact that the bears look to have just raised the white flag, and we could be looking at the start of the next leg of the rally. Analyst Sentiment Supports the Buy Signal The final point to consider is that while the MACD may have just had its bullish crossover last week, the analyst community has, for a long time, been almost unanimous in its bullish stance on Amazon. Just last week, the teams at Morgan Stanley, Citigroup, and Evercore all reiterated Buy or equivalent ratings, adding to those that came before and after July's report. The most recent price targets range as high as $300, which points to more than 30% in potential upside from where the stock closed on Tuesday. Compared to Qualcomm Inc (NASDAQ: QCOM), which continues to divide analyst opinion. In a market where big-cap tech is increasingly being picked apart for valuation risks, Amazon remains a near-universal Buy, which makes this entry point all the more appealing. What to Expect Next for Amazon There's a growing sense that Amazon is setting up for a retest of July's high, around the $235 mark, in the near term. For investors getting involved, this is the first level to watch, and a close above it would clear the path to February's all-time high around $242. As long as the broader market sentiment remains risk-on and the major indices keep hitting new highs, very little could get in Amazon's way. Read This Story Online |  Axcelis Technologies went from $2.50 to $180—a staggering 7,100% return. These are the kinds of small-cap breakouts Fierce Analyst aims to catch before they go mainstream.

Our research team uses data and trend analysis to uncover high-potential stocks early. And now, you can get free alerts on the next set of breakout candidates—before the crowd rushes in. Click here to get the free alerts and see what's coming next. |

| More Stories |

| |

|

|

0 Response to "🦉 The Night Owl Newsletter for August 21st"

Post a Comment