Monolithic Power's strong earnings and exceptional guidance confirm its critical role in supplying the power-hungry artificial intelligence... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Jeffrey Neal Johnson

Following its July 31st earnings announcement, shares of Monolithic Power Systems (NASDAQ: MPWR) jumped more than 10% in a single session on unusually high trading volume. In the first few trading sessions of early August 2025, Monolitic Power’s stock price seemingly stabilized, holding on to an approximate 13% overall gain. Such a decisive move up in a company’s stock price is rarely arbitrary. In this case, it directly responded to a rock-solid quarterly report. More importantly, it was also a response to powerful forward-looking guidance that confirmed the company’s essential role in one of the technology sector’s most demanding and fastest-growing departments: The hardware infrastructure for artificial intelligence (AI). The results demonstrated accelerating business momentum, providing investors with a data-driven look into how the company is capitalizing on the insatiable energy needs of modern data centers. Monolithic’s Financial One-Two Punch For investors, a company's ability not only to surpass past expectations but also to raise future forecasts is a strong bullish signal known as a beat and raise. It shows solid execution and management's confidence in the company's ongoing momentum. Monolithic Power delivered on both aspects in its second-quarter 2025 report. - The Beat (Q2 2025 Performance): The company posted record quarterly revenue of $664.6 million. This figure represented a meaty 31.0% increase from last year and comfortably surpassed Monolithic Power’s analyst community’s expectations. Conversely, non-GAAP earnings per share (EPS) came in at $4.21, outperforming the consensus estimate of $4.12.

- The Raise (Q3 2025 Guidance): While the strong quarter was notable, the company’s outlook truly captured the market's attention. Management projected revenue for the third quarter to be between $710 million and $730 million. This forecast was higher than analysts had previously modeled, forcing an upward revision of the company's growth trajectory and signaling that its business is accelerating into the year's second half.

Why Power Chips Are Mission-Critical This impressive financial performance is tied directly to a fundamental technological shift. The immense computational power required for AI models has created a critical challenge in data centers: energy consumption. Modern AI accelerators, such as GPUs and custom ASICs, are highly power-hungry, generating significant heat and straining the power delivery infrastructure of even the most advanced facilities. This is where Monolithic Power Systems (MPS) has established a key advantage. During its earnings call, management provided the missing link for investors, confirming it had begun "initial shipments of our power solutions to support our customers' new ASIC-based AI products." This statement solidifies the company’s position as a direct beneficiary of the AI hardware buildout and provides context for the remarkable growth in its Storage & Computing business segment, which surged 70.0% year-over-year. MPS does not just sell components; it provides highly integrated and efficient power modules that solve this energy bottleneck. Its proprietary technology allows for higher power density, meaning more power can be delivered cleanly and efficiently in a smaller physical space. These solutions are mission-critical for data center operators trying to maximize computing power without overhauling their entire infrastructure, making MPS a key enabler of the entire AI ecosystem. How Analysts and Institutions Are Responding Following the earnings release, Wall Street analysts were quick to validate the market's enthusiastic reaction. The strong results and optimistic guidance prompted a wave of positive revisions, reinforcing the company's bullish thesis. Firms including Citigroup, Stifel Nicolaus, and KeyCorp all raised their price targets on Monolithic Power Systems’ (MPS) shares, with many reiterating Buy or Outperform ratings. This chorus of approval from financial experts signals a growing belief that the company’s strategic execution is not only on point but accelerating, driven by the durable demand from the AI sector. This confidence is further reflected in the company's ownership structure. Over 93% of Monolithic Power's stock is currently being held by institutional investors. This high level of ownership by large financial entities, such as mutual funds and pension funds, indicates a deep and widespread conviction in the company’s long-term strategy and execution. It suggests that major investors who perform extensive due diligence see a sustainable growth path, providing a stable foundation for the company's strategic initiatives. More Than Just a Good Quarter Monolithic Power Systems' second-quarter performance was more than a strong earnings report; it confirmed a strategic success. The powerful combination of a definitive financial beat, firm forward guidance, and a direct link to the explosive growth in AI infrastructure provides a clear picture of a company firing on all cylinders. The market's decisive rally acknowledged this fundamental reality. While high growth expectations are often priced into technology stocks, the company delivered the data to back them up. The results signal a strategic inflection point where Monolithic Power is cementing its role as an essential supplier for the AI revolution, effectively turning the immense energy needs of the buildout into robust and accelerating financial growth.  Read This Story Online Read This Story Online |  Something big is brewing in Washington.

According to my research, an executive order from President Trump could be just weeks away.

And it holds the potential to trigger one of the most explosive tech booms in US history.

At the center of it all? Robots.

Not the kind that clean your house or pour you coffee.

But the kind that could reshape entire industries, add $1.2 trillion per year to the US economy, and affect 65 million American lives — just in the next year. This little-known company holds nearly 100 patents and trades for around $7 |

| Written by Leo Miller

Over the past 52 weeks, AppLovin (NASDAQ: APP) has been one of the biggest stock market standouts. As of the Aug. 6 close, shares have surged by a whopping 446%. The company has an incredibly strong record of delivering impressive earnings. Shares have gained by 12% or more the day following its last six earnings releases. But, investors seemed to hit the panic button after seeing AppLovin’s Q2 2025 results, released on Aug. 6. Within minutes of the release, shares plunged around 13% in after-hours trading. However, as investors further digested the results and management commentary, worries subsided considerably. By 10 PM EST, shares were down 5.5% in extended trading. Then, in a massive shift, shares gained by more than 10% midday on Aug. 7 as the rest of the market provided its take on the results. So, what are the key details from AppLovin’s earnings, and what is the outlook for this gangbusters stock going forward? Let’s dive in to get to the bottom of these questions. Note that the company’s Q2 results only consider its advertising segment. On June 30, AppLovin sold its Apps business and excludes its results from the Q2 report. APP: Explosive Revenue Growth Plus Leading Free Cash Flow Margins In Q2, AppLovin reported revenues of approximately $1.26 billion, an increase of 77% versus Q2 2024. According to MarketBeat estimates, this figure fell short of the $1.37 billion Wall Street was looking for. Notably, that 77% rate was the highest growth figure the company’s advertising business posted over the past five quarters. The company’s bottom-line results were a different story. Diluted earnings per share (EPS) came in at $2.26, substantially higher than the $2.05 estimate. The figure marked a massive 163% spike versus the prior year's quarter. The company’s guidance for Q3 also came in moderately better than expected. AppLovin’s sale of its Apps segment drove one of its key intended results: massively lifting the margins of the overall business. AppLovin achieved an EBITDA margin of 81%, compared to 67.7% in Q1 2025 when the company included the Apps business in the results. AppLovin also posted an incredible free cash flow margin of just under 61%. Excluding the Apps business, this gives the firm a last-12-months free cash flow margin of 66%. That’s the highest figure of any large-cap U.S. stock in the software industry over that period. It’s also higher than any stock in the Magnificent Seven. E-Commerce Developments: AppLovin’s Next Frontier AppLovin dominates advertising in mobile gaming, but it sees huge potential in the much larger e-commerce market. Last quarter, the firm provided the first key data around its e-commerce push, stating that it had achieved an annual run rate of $1 billion with around 600 customers. In Q2, AppLovin didn’t provide any new numbers around the e-commerce push, which likely disappointed investors initially. However, it did provide key details on why that was the case and clarified the timeline going forward. AppLovin said it intentionally constrained the advertiser onboarding process in e-commerce to make its product better. The stock’s price action on Aug. 7 shows that although this wasn’t the best news, it certainly wasn’t a reason for investors to panic. AppLovin is entering a massive new market. To achieve sustained success, making sure its product is high-quality is much more important than moving quickly. The company said it plans to begin onboarding again on Oct. 1. However, new customers will require a referral from an existing customer to join, meaning the rollout will still be somewhat measured. A full rollout will begin in the first half of 2026. Based on this information, investors might not get a huge amount of new data on AppLovin’s e-commerce push until its Q1 2026 earnings release. The company says it is less than 1% penetrated in e-commerce in terms of the number of advertisers it works with. This highlights the huge opportunity it has going forward. APP: E-Commerce Could Bring Big 2026 Gains, Analysts Lift Targets Overall, AppLovin didn’t announce anything groundbreaking in Q2. Thus, for a stock that has risen so much, it wasn’t surprising to see shares fall after-hours. However, its enormous e-commerce opportunity still remains, and analysts are bullish on the stock. Morgan Stanley and Piper Sandler raised their price targets to $480 and $500, respectively, on Aug. 7. These numbers imply significant upside potential in shares going forward. They highlight how AppLovin could experience strong gains in 2026 if its e-commerce business really takes off. Read This Story Online |  Investing Legend Hints the End May be Near for These 3 Iconic Stocks

Futurist Eric Fry say Amazon, Tesla and Nvidia are all on the verge of major disruption. To help protect anyone with money invested in them, he's sharing three exciting stocks to replace them with. He gives away the names and tickers completely free in his brand-new "Sell This, Buy That" broadcast. Click to get the full details on Eric Fry's "Nvidia alternative" right here. |

| Written by Chris Markoch

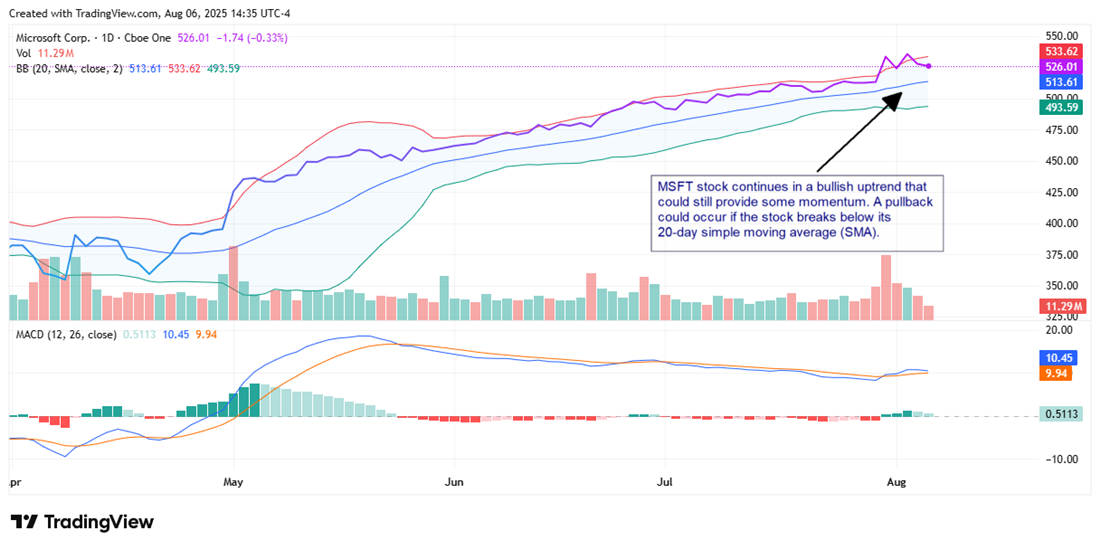

Microsoft Corporation (NASDAQ: MSFT) delivered an earnings report that can be considered a blowout, even for a mega-cap company with high expectations. Microsoft beat on revenue and earnings and reiterated its guidance for data center spending for the remainder of the 2025 calendar year. Analysts have taken notice. The Microsoft analyst forecasts on MarketBeat show that nearly two dozen analysts have either reiterated or raised their price target for MSFT stock. Many of the new targets are above the consensus price of $609.86, which is a 15% gain from the stock’s price on August 6. Why Buying the Best Still Matters August is a tricky month for investors. Apart from a few names like NVIDIA, the major technology stocks have already reported. The economy continues to give off conflicting signals, and Congress is out on recess, which generally leads to a less active market. This is a good reminder of why buying the best matters. In the tech sector, that means Microsoft. The company’s stock has been up about 2.8% since the earnings report, but that’s down from the 5% gain it had before a slight pullback this week. Earnings Drive Stock Price Growth Earnings reports provide a snapshot of a company’s performance. However, the headline numbers are lagging indicators. In other words, they tell what’s happened in the past. What a company has to say about the current and future quarters can drive up a stock price. For a mega-cap company like Microsoft, that usually comes down to its earnings outlook. Analysts project Microsoft to post 12.3% earnings growth in the next 12 months. That compares favorably to another mega-cap hyperscaler, Meta Platforms Inc. (NASDAQ: META), which analysts project to post 13.15% earnings growth. That aligns with the company’s guidance for “double-digit earnings growth on a constant currency basis.” However, it also means that analysts are slightly more bullish about earnings expectations for Microsoft, which largely explains the outlook for 15% stock price growth. Leading the AI Revolution Microsoft emphasized that its projected future growth will be driven by continued investment in AI and cloud infrastructure, improving operating leverage, and disciplined expense management. That aligns with Dan Ives' sentiment. The Wedbush analyst continues to be bullish on the tech sector, specifically the Magnificent Seven stocks that will lead the AI revolution. Ives and his team believe that the market is not fully appreciating the amount of spending that will be needed over the next three years. Wedbush lists Microsoft, Meta Platforms, NVIDIA, Tesla, and Palantir as its top five tech stocks for the second half of 2025. That bullish outlook comes with a price target of $625, up from $600. However, Wedbush isn’t the most bullish on MSFT stock. That would be Brent Thill from Jefferies Financial Group. The analyst raised his price target for Microsoft to $675 from $600. A Cautious Chart That Still Has Momentum MSFT stock continues to be in a sustained uptrend. The 20-day simple moving average (SMA), currently around $513.61, is serving as a reliable short-term support level. Price action remains above the 20-day SMA and within the upper range of the Bollinger Bands, signaling strength and proximity to potential overbought conditions. The MACD (Moving Average Convergence Divergence) shows a slight bullish crossover, with the MACD line (10.45) above the signal line (9.94), suggesting upward momentum could continue. However, there may be limited strength behind the move.

One reason is the relative strength indicator (RSI), which, at 64, suggests that MSFT is approaching overbought territory. However, there may still be room for modest upside before a possible pullback or consolidation. Another potential short-term concern is lighter volume after the post-earnings surge. That’s not a bearish signal but could signal that momentum is slowing. Read This Story Online |  |

| More Stories |

| |

|

|

0 Response to "🦉 The Night Owl Newsletter for August 7th"

Post a Comment