Hidden outside San Antonio sits the only US factory producing a new “AI metal” that could cut power bills by 99%.

Google, Microsoft, IBM… every major AI player will be forced to secure massive amounts of this material just to keep their artificial intelligence hopes alive…

Without it, their data centers risk being crippled by soaring energy costs.

And with only one US company able to produce it at scale, control of this supply could decide the winners and losers of the entire $27 trillion AI market.

See why the race for supply has already started.

Chris Rowe

Target: Missing the Mark in 2025—Downtrend May Continue

Written by Thomas Hughes. Published 8/20/2025.

Key Points

- Target's Q2 results are insufficient to bring this market back into a buying mode.

- The choice for the new CEO is uninspiring and will likely impact market sentiment in the second half of the year.

- Analysts' trends are negative, suggesting this market will move down to set a new low before the year's end.

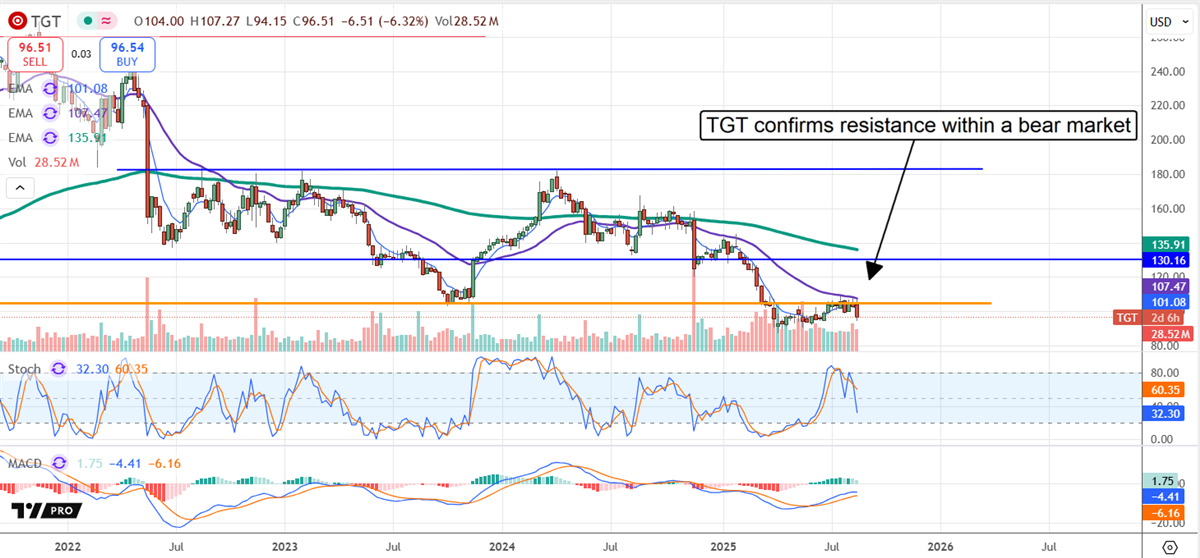

While Target’s (NYSE: TGT) FQ2 2026 results show some improvements, the company continues to lag its peers, lose market share, and contract its business. Moreover, the choice of the new CEO did not boost market optimism. Yes, Cornell is out, and COO Michael Fiddelke is in, and the market did not like it.

The takeaway from the chatter is that Fiddelke has had ample opportunity as COO to positively impact the turnaround, and an outsider would have been a better choice. The stock fell more than 10% on the news, confirming resistance at a critical level within an existing bear market.

With this in play, if the buyers do not step in quickly, this market could hit new lows before the end of August and extend its downtrend to even lower levels.

The hit to sentiment is significant. It is possible that Fiddelke can turn the business around, but it won’t be known for at least another quarter, and there are significant headwinds.

In the meantime, analysts, who have recently begun to improve sentiment trends, are unlikely to continue with stock price increases until there is proof that he was the right choice.

As it stands, the analysts rate this stock as a Hold. The bias is bearish, with the number of Hold and Sell ratings increasing in 2025, and the price target trend revision is downward.

The consensus forecasted a 10% upside ahead of the release, but it was down 35% in the preceding 12 months, exerting downward pressure on the market. The low-end led to $82, a new low when reached.

Target’s Better-Than-Expected Quarter Is No Catalyst for Higher Prices

Target’s results reflected a sequential improvement in the business and outperformed the consensus reported by MarketBeat, but they did not provide a catalyst for higher prices. The $25.21 billion in net revenue outperformed by 120 basis points but is down nearly 1% compared to last year.

The decline is underpinned by a 1.9% decline in systemwide comps driven by a 1.2% decrease in merchandise sales.

The weakness in merchandise is offset by a 14% increase in non-merchandise sales, i.e., revenue from Starbucks (NASDAQ: SBUX) occupancy and ads, but this is insufficient to produce core growth or be reliable.

Weak store traffic will likely weaken partners' revenue as they exit stores. Likewise, the 4.3% increase in digital sales is a positive. Still, it is weak compared to Target’s competitors and not a reliable driver for systemwide growth.

Target Earnings Contract at an Accelerated Pace in FQ2

Margin is another mixed bag unlikely to support the price action in the second half of calendar 2025. The company’s gross and operating margins contracted despite internal efforts.

Markdowns and merchandising efforts cut into the bottom line and can be expected to impact results moving forward. The $2.05 outperformed due to the top-line strength, but the margin is slim at under 50 basis points, and EPS is down 20% compared to the prior year.

Guidance is another factor likely to impact the stock price action in the second half. The company reaffirmed its guidance despite the Q2 strengths, which equate to a weaker-than-previously-expected second-half forecast, and there is potential for it to be overly optimistic.

Investors should watch institutions. Their trends in 2025 are bullish, with them buying on balance every quarter of the year through the fiscal Q2 release date and activity ramping sequentially.

If this trend continues in 2025, the stock price decline may end as soon as it begins, keeping TGT shares trapped within the existing trading range.

This email communication is a paid advertisement sent on behalf of True Market Insiders, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you need assistance with your newsletter, please don't hesitate to email our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

Copyright 2006-2025 MarketBeat Media, LLC.

345 N Reid Place, Sixth Floor, Sioux Falls, SD 57103-7078. USA..

0 Response to "The Hidden Key to Powering the $27T AI Boom"

Post a Comment