Editor's Note: Imagine typing an 18-digit code into your brokerage account and walking away one week later with a $6,316 payday. Sounds like a fantasy, but that's one of the ways Larry Benedict made over $274 million in profits at his top 1% hedge fund. And now he's sending the codes to ordinary people. They've seen an 84%-win rate so far, and the next code could go out any day now. For details and access, click here or read on…

Dear Reader,

A former top 1% hedge fund manager just cracked open his private playbook.

He's sharing what he calls "Skim Codes" with regular folks.

These aren't stocks. Not crypto. Not some complicated trading scheme.

They're simple 18-digit codes you punch into your brokerage account.

Lauren Wingfield Managing Editor, The Opportunistic Trader

Today's editorial pick for you

OKTA Stock Suffering from Case of Mistaken Identity

Posted On Dec 03, 2025 by Chris Markoch

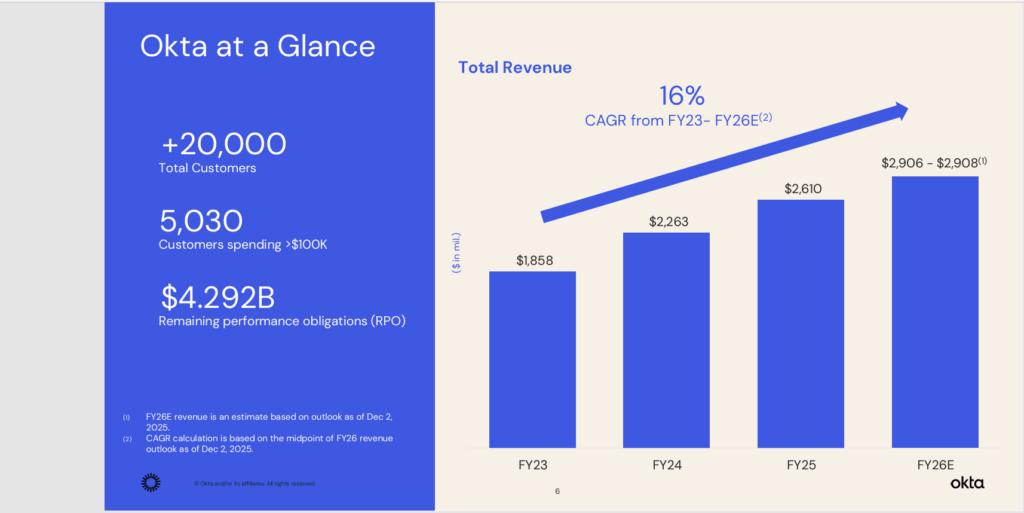

Okta. Inc (NASDAQ: OKTA) delivered its latest earnings report on December 2 after the market closed. The report was objectively strong, but the stock's reaction tells a different story. The identity specialist beat expectations on both revenue and earnings, raised guidance, and continued to post impressive margins.

But investors were unimpressed. Shares traded lower in after-hours, reflecting a market that still sees a growth profile mismatched with a premium valuation.

For investors, the issue is less about whether Okta is executing and more about what kind of company the market thinks it is, and what multiple that identity deserves.

A "Beat and Raise" That Didn't Matter

For the quarter ended October 31, Okta delivered revenue of about $742 million, up roughly 12% year-over-year and modestly ahead of consensus. Non-GAAP EPS came in around $0.82, handily topping expectations, while adjusted operating income and margin also exceeded Street models.

Management guided next-quarter revenue to roughly $749 million at the midpoint, above analyst estimates, and raised full-year non-GAAP EPS guidance, signaling continued operating leverage.

Despite that, the stock slipped more than 3% in after-hours trading to the high-$70s, erasing a modest year-to-date gain. Investors had seen this movie before: "good" numbers, a constructive outlook, and a share price that still bleeds because the growth trajectory doesn't clear the bar implied by the multiple.

Solid Fundamentals, Slower Growth

Under the hood, Okta's fundamentals continue to improve. Revenue is growing in the low-teens, powered by large enterprise customers and expanding adoption of newer products across identity governance, privileged access and device-level controls. Current remaining performance obligations (cRPO) grew in the low-teens as well, slightly ahead of expectations, suggesting that large deals and renewals remain healthy even as budgets stay scrutinized.

Profitability is no longer a question mark. Okta is running with non-GAAP operating margins in the low-20s and free cash flow margins north of 25%, levels that many software peers with similar growth would envy. The company also reiterated that it is no longer building extra conservatism into guidance related to its 2023 security incident, indicating that reputational damage is now largely behind it.

The sticking point is that growth is decelerating. Management's full-year outlook implies mid-teens revenue growth this fiscal year, while consensus expects growth to drop toward high single digits over the next 12 months—well below the 20–30% days that used to justify a richer valuation.

The Valuation Identity Crisis

Okta's problem is that the stock is still priced somewhere between a high-growth SaaS name and a mature, steady compounder. With an enterprise-value-to-sales multiple around 5x and very high EV/EBITDA metrics, the market continues to ascribe a quality premium even as growth expectations step down. At the same time, analysts' average price target remains meaningfully above the current quote, and the consensus rating is still "Buy," which keeps sentiment and expectations elevated.

In that light, the post-earnings selloff looks less like a verdict on this quarter and more like a slow multiple reset. When a company consistently "beats and raises" yet the stock still drifts lower, the market is effectively rewriting the narrative from hypergrowth disruptor to durable, mid-teens grower—with a more pedestrian multiple to match.

Growth Story vs. Identity Utility

There is also a strategic "mistaken identity" at work. Okta operates in identity, a category that sits at the center of zero-trust architectures and cloud security, but much of Wall Street still treats it like a standalone application vendor rather than foundational security plumbing. As hyperscalers like Microsoft lean into their own identity platforms and broader security suites ingest identity signals, investors worry that Okta's growth ceiling is lower than once hoped, even if the company remains profitable and strategically relevant.

Management continues to argue that Okta's independent, multi-cloud position and deep partner ecosystem are advantages as enterprises mix and match security tools. Large deals involving channel partners and cross-sell into governance and privileged access suggest that Okta can still expand wallet share inside its base, even if net-new logos grow more slowly. But the market appears unwilling to pay a "category king" valuation for what now looks like a more measured growth story.

What Investors Should Watch Next

For investors, the setup is increasingly binary. On one side, Okta offers a combination of double-digit growth, strong free cash flow, and a balance sheet that supports continued product investment—attributes that can justify a mid-single-digit sales multiple if sustained. On the other, if revenue growth glides down toward high single digits while platform competitors keep gaining ground, further multiple compression is a real possibility even if quarterly execution remains solid.

Going forward, the key metrics will be cRPO and large-deal activity, which indicate whether Okta can reaccelerate growth from its large-customer base, and margin durability, which will determine how much of today's valuation is supported by cash generation rather than hoped-for reacceleration. Until the market resolves Okta's "identity crisis"—deciding whether this is a steady identity utility or a still-scaling growth engine—the stock is likely to remain volatile, with good quarters not always translating into good returns.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

0 Response to ""Skim" $6,361 with an 18-digit code? 🔥"

Post a Comment