Three times over the last 30 years.

That’s how often I’ve received the signal to go “all-in” on gold.

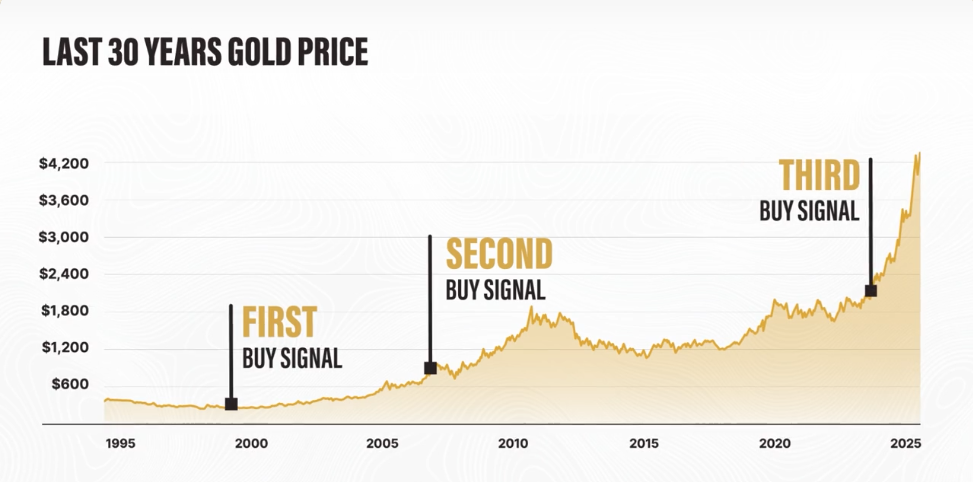

The first time was back in the 2000s…

The dot-com mania was nearing its peak, money was flooding into any and all tech stocks, and equity valuations were trading at nosebleed levels.

I was in my mid-20’s. Just starting my first business.

And although I didn’t have much capital to spare, I scrounged together as much money as I could to load up not on tech stocks… but on gold coins.

At the time, gold was despised by Wall Street.

Goldman Sachs called it “a 19th-century asset.”

One of Merrill Lynch’s top investment analysts said that it was only for “grandmothers and conspiracy theorists.”

And two of America’s leading economists at the time called it a “barren asset.”

Yet, I chose to go in at under $300 an ounce.

My second signal came in 2008 when, amidst the chaos of the financial crisis, gold prices dropped briefly below $800 an ounce… and I once again went “all-in” on gold.

And a little over a year ago, I did it again…

I moved roughly 50% of my liquid net worth into gold and Bitcoin:

Three “all-in” decisions… Each of which seemed crazy to most at the time.

But for me… it was the most obvious move to make.

Why?

It’s all thanks to an incredible secret I learned from famed economist Kurt Richebächer - the last of the true Austrian economists.

What he taught me has been incredibly accurate at predicting the price of gold over the years.

It’s helped me make an absolute killing each of the three times I went “all-in.”

And right now, it is again predicting a shocking new price for gold in the near future.

Click here to see my full prediction for gold now.

Good Investing,

Porter Stansberry

Disney's Q1 2026 Missed Hype, But the Turnaround Builds

Submitted by Thomas Hughes. First Published: 2/2/2026.

What You Need to Know

- Disney's turnaround gains traction in early 2026, setting up for a leveraged earnings recovery.

- Analysts responded favorably, aligning with trends that suggest a market reversal is imminent.

- Capital return is a factor, including a reliable dividend and accelerating share buybacks.

Walt Disney Company's (NYSE: DIS) Q1 2026 results and guidance were not a blowout, but they confirm the company is gaining traction. Years in the making, the Bob Iger-led turnaround has the company back on track, growing, and positioned for a leveraged earnings recovery over time.

The weakest aspect of the report was diminished earnings quality. Headwinds were present: higher operating costs and growth investments, plus elevated CapEx tied to expansions and cruise ship launches. While these items weighed on near-term earnings, the investments and increased CapEx are intended to expand capacity and support higher revenue and margins over time.

Disney Outperforms in Q1: Reaffirms 2026 Guidance

The Silver Strategy Hiding Inside IRAs (Ad)

In 2000, I told Barron's that a popular dot-com stock was headed for trouble. It dropped 90%. Now I'm making the opposite call on that same company: buy it now. This stock has become the lifeblood of AI data centers, yet almost no one has caught the story. While the media focuses on AI chip wars, they've missed this company's essential role in building out data centers. Their hardware is so critical that a single building uses enough of it to stretch around the world eight times. If you own Nvidia, you might want to pivot. If you missed Nvidia, this is your second chance at the AI data center buildout happening worldwide.

See the under-the-radar play fueling AI data centersDisney delivered a solid Q1, with revenue rising 5.3% to $26 billion — about 40 basis points above analyst consensus. All segments showed sequential improvement and year-over-year (YOY) growth: Entertainment led with 7%, Experiences grew 6%, and Sports was up 1%.

The Sports segment was hit by one-offs, including YouTube availability issues that have since been resolved.

Strength in Experiences came from both domestic and international operations, with U.S. growth supported by a 1% increase in traffic and a 4% rise in guest spending.

As expected during a turnaround, the company faced margin pressure from expansion and growth investments, though the hit was smaller than feared. Operating income declined 9%, and adjusted operating margin fell by more than 700 basis points.

However, adjusted results still beat consensus by roughly the equivalent of 300 basis points versus expectations, leaving Disney well positioned to continue executing its strategy this year.

The guidance was constructive but not an outright bullish catalyst for the stock. Management reaffirmed its full-year outlook, calling for growth and margin expansion with strength expected in the second half of 2026, which essentially reaffirmed its prior guidance.

Analysts reacted favorably after the release, pointing to margin resilience and a solid growth trajectory. DIS carries a Moderate Buy consensus in early February, and the price target consensus is trending higher, implying roughly 20% upside from critical support. January 2026 revisions also skew toward the high end of the range.

A move higher, even merely to the consensus price target, could lift the market out of its long-term trading range and signal a technical reversal.

Walt Disney's Capital Return Is Reliable and Accelerating in 2026

Q1 cash flow was pressured by increased investment, pushing overall cash flow into negative territory. Financing activities, however, helped minimize the cash burn and left the balance sheet strong enough to sustain an aggressive capital return.

Balance-sheet highlights at the end of Q1 include steady cash levels and higher current and total assets, partially offset by increased liabilities. Long-term debt ticked up and equity declined, but leverage remains low, with debt under roughly 0.35X equity. The equity decline also reflects share repurchases, which raised treasury shares.

The capital-return program combines dividends and share buybacks. The dividend annualizes to $1.50, is paid semiannually, and yields about 1.3%. Buybacks accelerated, reducing the share count by 1.4% YOY in Q1, and are expected to stay robust through year-end. Management targets roughly $7 billion in buybacks for 2026, about 3.5% of the early-2026 market cap.

Post-release price action was unfavorable despite signs of business improvement and an outlook for a stronger back half of the year. The stock dropped more than 6%, falling below a key support level near the top of the existing range. Early trading suggested some buying support, albeit not at the prior range top, which means a 2026 rebound and a potential technical reversal are still possible. Catalysts for a recovery include a subsequent earnings report or a vote by the board on Mr. Iger's successor later in the quarter.

This email is a sponsored email for Porter & Company, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you need help with your subscription, please don't hesitate to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, South Dakota 57103. United States of America..

0 Response to "When to buy gold (mathematically)"

Post a Comment