Ticker Reports for May 18th

Squarespace's Buyout Signals a Recovering Financial Market

Shares of Squarespace Inc. (NYSE: SQSP) are up nearly 30% after private equity firm Permira offered to take it private through a $6.9 billion all-cash deal. Before this offer, Squarespace had a market capitalization of approximately $4.6 billion. So, what could make this private equity fund willing to pay a 50% premium for this technology stock?

The simple answer lies behind the Federal Reserve's (the Fed) plans to cut interest rates later this year. It looked like the first cuts would come in March, then May, and now September, according to the CME's FedWatch tool.

Forget the Noise, Here's What Matters

After a disappointing 1.6% U.S. gross domestic product (GDP) growth in the past quarter, investors should have become worried about the economy's current state, but that didn't seem to happen.

Low economic growth is expected to push the Fed's agenda into cutting rates sooner rather than later, as the economy needs a more flexible financing environment to heat up again. According to ISM PMI readings, the manufacturing and business services sectors contracted in the past month. This is bad news for future GDP growth and may create another pressure point for the Fed to act more quickly than expected.

Inflation is another factor nudging the Fed into a decision. For the past month, inflation has been above the Fed's 2% target and just came in at 3.4%. Still relatively hot, and with no prospect of slowing down toward the Fed's target, it may pose a problem for investors betting on interest rate cuts to come relatively soon.

However, that's not the view at Permira, as the recent Squarespace acquisition leads many to believe that the financial markets may not be as shaken as they seem.

Investors Want Quality, Not Empty Promises

Despite recent rallies in meme stocks, those hoping to see GameStop Corp. (NYSE: GME) and AMC Entertainment Holdings Inc. (NYSE: AMC) reach a new ceiling might be in for a surprise. Because these companies lack one essential thing, their recent rallies may be short-lived.

According to the company's press release, one of the main reasons behind the Squarespace buyout is cash flow, which reached $85.2 million in the past quarter. Even after capital expenditures of $47 million, the company walked away with a free cash flow of roughly $38.2 million, giving investors confidence that this business can cushion low economic growth and high inflation (also known as stagflation).

This financial stance compares with GameStop's negative free cash flow. AMC is close behind, with share dilutions being the only strategy to keep funding losing operations. The takeaway? Investing is cool again, but it must come with solid fundamentals.

Better Fits for Today's Market

Knowing this, investors can find a much better proposition in Adobe Inc. (NASDAQ: ADBE), especially now that the stock trades at 76% of its 52-week high today.

Exposed to the broader tailwinds found in the artificial intelligence space, analysts are willing to bet that Adobe could deliver 12.8% earnings per share (EPS) growth in the next 12 months. Above-average growth is the driver here, as these same analysts see a valuation of up to $700, according to those at Piper Sandler. To prove these projections right, the stock must rally 43.9% from its current price.

Another example of technology exposed to the bullish trends in the U.S. real estate market is SoFi Technologies Inc. (NASDAQ: SOFI). When and if rates do come down, cheaper mortgage financing could spark a new demand boom in real estate. Because of this, analysts are willing to bet that SoFi can deliver up to 200% EPS growth this year, not to mention that Jefferies Financial Group slapped a $12 price target for SoFi stock, calling for a net 64.3% upside from where it trades today.

The lesson here is that if investors want to beat stagflation today, they must choose solid fundamentals at a reasonable discount; anything else is just noise.

$5,000 Gold?

Former Wall Street Banker Reveals Mysterious Gold Leverage

As gold continues to soar, this ex-Goldman Sachs VP says DON'T buy bullion or mining stocks. Instead, he's just shared a "gold bank" that uses about $10 of your money to harness the power of two ounces of pure gold (worth about $4,200 right now).

3 Small Cap Techs Gaining Traction for Investors

Tech stocks offer the largest gains for investors because the opportunity for growth is immense. Often started from nothing, microcap tech stocks can blossom into market-leading names, with Alphabet (NASDAQ: GOOGL), Apple (NASDAQ: AAPL), and Microsoft (NASDAQ: MSFT) as prime examples. This article examines three hot-tech small caps gaining business traction and providing shareholder value. There’s no guarantee that these tech stocks will blossom into the next mega-cap winner, but all are contenders with at least a double-digit upside potential for their share prices.

Lightspeed Results and Repurchase Plan Lift Shares 20%

Lightspeed (NYSE: LSPD) is a cloud-based SaaS that provides merchant and customer engagement services to small and medium-sized businesses. The platform resonates with clients. Clients are growing in number and deepening their use of services. The FQ4 results include a 25% increase in net revenue that outpaced the consensus estimate by 200 basis points on an increase in payment and transaction volume.

Other significant highlights include another quarter of adjusted operating profits, which made the first full year of profitability. The guidance is also favorable, indicating at least 20% growth in 2025 compared to the 23% forecast by the analysts' consensus estimate.

Profitability is a key highlight. The company’s cash flow stabilizes, allowing the board to authorize a share repurchase plan. The plan aims to reduce the count by the maximum 10% TSX regulators allow and will likely continue in the following fiscal year. The post-release action is noteworthy because it lifted the market to the low end of the analysts' target range, leaving ample upside for inventors. Analysts rate this stock as a Moderate Buy and see it advancing another 27% at the consensus midpoint.

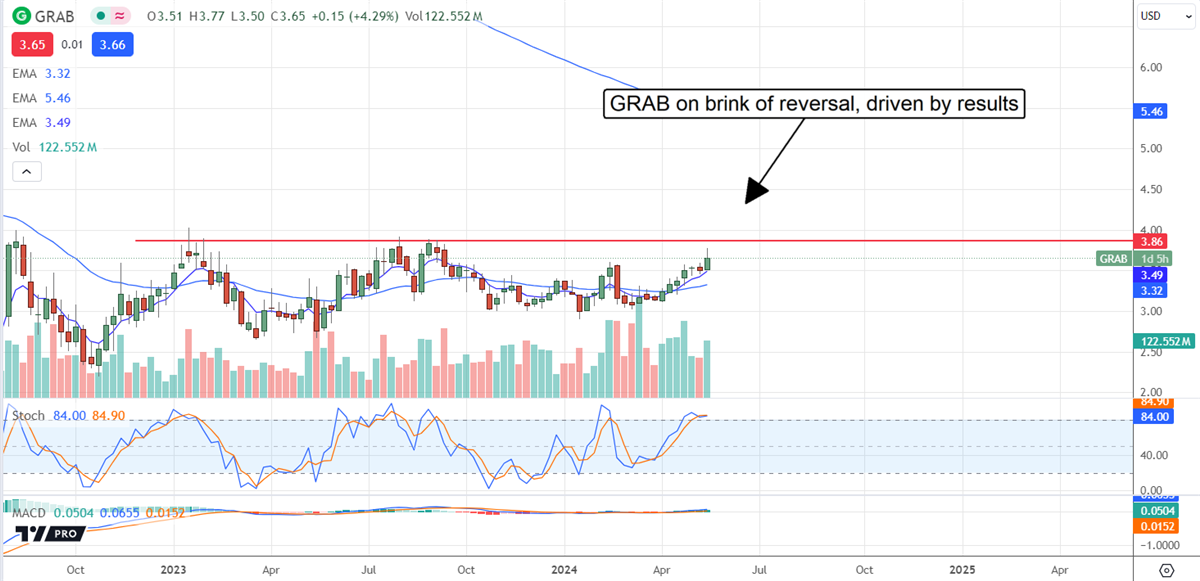

Grab some Grab, The Super App for eCommerce

Grab (NASDAQ: GRAB) operates a platform for eCommerce spanning verticals and is known as a super-app. The company serves the Southeast Asian markets and is generally viewed as a deep value on the brink of sustained profitability with ample opportunity for growth. The latest results were mixed. Revenue grew 24% and outpaced the consensus, but earnings fell short. However, it is the outlook for profitability that has the market moving. The company reiterated its outlook for revenue while raising the range for adjusted EBITDA to above the previous.

The news is spurring the analyst to act. The first update tracked by Marketbeat is from Benchmark, reiterating a Buy rating and $6.00 price target. The buy rating aligns with the consensus of six analysts; the $6 price target is at the high end of the range and roughly 20% above the consensus target, which implies a 37% upside from current levels.

The technical action is favorable to investors and traders. The market is up more than 2.5% on the news and on the cusp of completing a reversal. The critical resistance is near $4.00 and may be reached soon. A move above that level would open the door for a sustainable rally to form. In that scenario, the market could reach the consensus target of $5.10 quickly, possibly before the end of the year.

Katapult is Ready to Launch, but Will it?

Katapult (NASDAQ: KPLT) operates a lease-to-own platform in the US. The share price dived in 2021 and hit new lows this year, but looks ready to start moving higher now. The FQ1 results include 18% top-line growth, better-than-expected GAAP losses, and favorable guidance for Q2. The company expects growth to continue in Q2 if at a slower 10% pace, supported by expanding the client base and growing share among existing merchants. That combination is expected to accelerate the top-line growth in the coming quarters.

Risks for this market include a lack of interest. There is only one analyst following it, Loop Capital and the last update is over six months old. The price target issued in September 2023 is $20, about 15% above the current action, but there is little to no market conviction to support it. Institutions own about 27%, suggesting a lack of conviction, and sellers outpace buyers this year. The market surged on the news but hit resistance above the $20 target and quickly reversed. The market now shows significant resistance that may not be broken without another solid catalyst.

Bitcoin's Biggest Year Yet

2024 is set to be a historic year for Bitcoin.

It's all thanks to three major catalysts that I reveal in my newest video.

The Real Reason Michael Burry is Buying Physical Gold

Michael Burry, the legendary investor who predicted the 2008 financial crisis, has once again made waves with his latest 13-F filing.

While he added to and trimmed several positions, the standout move was his new investment in Sprott Physical Gold Fund (NYSEARCA: PHYS). In this article, we'll delve into the highlights of this filing and why he chose to invest in physical gold over other forms of the precious metal.

Burry is the maverick investor who netted $700 million during the 2008 financial crisis by betting against the housing market—a feat captured in the award-winning film The Big Short—and is widely regarded as a prescient Wall Street outsider.

Since his famous bet, he has made several notable trades. He strategically invested in water assets, anticipating future scarcity, and bought into GameStop (NYSE: GME) in 2019 before it became the poster child of meme stocks. During the COVID-19 pandemic, Burry purchased put options on equity indices, anticipating market turmoil amid the global crisis.

In his latest 13-F filing (an SEC report that details large managers’ equity holdings), Burry shows a substantial new position in Sprott Physical Gold Trust, which now makes up 7% of his portfolio. This move highlights his focus on physical gold as a hedge against economic instability and inflation.

Here are some key reasons why gold is relevant for any investor's portfolio:

- Long-Term Store of Value: Gold's industrial use and limited supply make it a reliable long-term store of wealth, trusted for centuries. The metal also protects against the eroding effects of inflation.

- Fed Policy Misstep: Gold serves as a safeguard against potential Federal Reserve policy errors, especially as the Fed is under pressure to cut rates amid rising inflation and public deficits.

- Fiat Devaluation: Gold hedges against the devaluation of the US dollar and fiat currencies in general, offering stability when confidence in traditional money wanes. The rise of Bitcoin also reflects this trend.

So…gold makes sense. But why physical gold?

Investors have multiple ways to gain exposure to gold, including ETFs, gold mining stocks, and futures. There are a few reasons why he chose the Sprott Trust specifically. Let’s find out why.

1. Direct Exposure

The Sprott Physical Gold Trust offers direct exposure to gold bullion, providing a way to invest in gold without the operational and management risks associated with mining companies. Investors purchase real gold stored in secure vaults, which is more stable and less volatile than mining stocks.

2. Reduced Operational and Management Risks

Gold mining companies face various operational risks, including high fixed costs and regulatory issues, particularly as many gold mines are in politically volatile regions. Investing in PHYS eliminates these risks, as it purely tracks the price of gold without the added complexities of mining operations.

3. Redemption Feature

This is the key to Burry’s decision. Subject to minimum quantity requirements, PHYS allows investors to redeem their units for gold bullion, a unique feature not offered by most gold ETFs.

A doomsday investor like Burry wants the ability to retrieve gold if markets are going through an extreme crisis. In a scenario like that, a regular ETF investor might face a situation in which the ETF issuers are in financial trouble themselves and may not fulfill their obligations. The Sprott redemption feature eliminates that risk for Burry and other investors.

Burry made other significant changes to his portfolio in the first quarter of 2024. He bolstered his stakes in Chinese tech stocks JD.com (NASDAQ: JD) and Alibaba (NYSE: BABA), bringing his total holdings in these companies to $9.9 million and $9 million, respectively. On the flip side, he completely exited his positions in tech names such as Oracle (NYSE: ORCL), Google (NASDAQ: GOOGL), and Amazon (NASDAQ: AMZN).

Investing in gold carries risks, particularly if inflation subsides. The appeal of gold would also diminish if the Federal Reserve begins a rate-cutting cycle. For investors looking to hedge against inflation and market instability, however, following Burry’s lead could provide a robust and tangible store of value.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 The Real Reason Michael Burry is Buying Physical Gold"

Post a Comment