Ticker Reports for May 22nd

TJX Companies Can Hit New Highs; Double-Digit Upside to Follow

TJX Companies (NYSE: TJX) industry-leading position in off-price retail and quality operations will soon lead its stock price to new heights. Like Walmart (NYSE: WMT), TJX Companies benefits from the high inflation and interest rate environment because shoppers are still flush but turning more to value and opportunity than ever before. The Q1 results are not robust but show growth compared to contraction, as was reported by Target (NYSE: TGT), and margin strength to drive capital returns. The takeaway is that TJX Companies' business is progressing normally; it’s growing, paying its dividend, repurchasing shares, and driving shareholder value.

TJX Companies Advances on Mixed Results

TJX Companies Q1 results are mixed relative to the analysts' consensus reported by Marketbeat, but in that special way the market likes, where tepid top-line data is offset by bottom-line strength. Revenue was as expected at $12.48 billion, driven by a 3% systemwide comp. All segments contributed to the positive comp, with Marmaxx up 2%, HomeGoods up 4%, Canada up 4%, and International up 2%. HomeGoods is the strongest segment, with positive sales growth compared to last year’s contraction.

Margin news is also favorable. The company reported a wider gross and operating margin due to lower freight costs and favorable mark-up. The net result is a 22% increase in GAAP earnings, more than triple the top-line growth, and a cash build on the balance sheet.

Guidance is also mixed. The company held its revenue targets steady but increased the outlook for earnings. The only bad news is that the $4.03 to $4.09 in GAAP earnings forecast for the year aligns with the analysts' consensus and would not normally be a positive catalyst. However, the cash flow, cash build, and capital returns help to offset it and have the market moving higher premarket after the release.

TJX Companies' Robust Capital Returns are Safe and Reliable

TJX Companies' dividend isn’t all that impressive, with a yield near 1.5%, but it is above the market average, reliable, and compounded by share repurchases. Share repurchases more than double the effective yield and are significant to shareholders because the company retires shares to reduce the count. Repurchasing activity lowered the share count by an average of 1.5% diluted in Q1 and is expected to continue at a robust pace this year. The roughly $500 million spent in Q1 is 20% of the FY target, suggesting the pace will increase as the year progresses.

Quarterly cash flow was insufficient to cover the capital return, but the annualized outlook is solid. The company’s strongest quarters are still ahead, and strength is seen in the balance sheet, reflecting the impact of last year’s results. Despite the deficit, the company’s cash position increased compared to last year, and other balance sheet details are favorable. The inventory is down, aiding the cash build, but it is still solid and total assets are up. Liabilities are flat, debt is flat, and equity is up 17%. Leverage is very low at less than 0.5X equity, leaving the company in a lean, nimble shape to pursue this year's retail opportunity.

Analysts See TJX Companies Forecast at New Highs

The trend in analysts’ sentiment is bullish and unlikely to change with these results. The seventeen analysts tracked by Marketbeat have the stock pegged at Moderate Buy and see it trading near $107. That’s worth a 10% upside from the prerelease levels and puts the market at a new high. Because the freshest targets are above consensus. The $107 target is a minimum for this market.

The post-release price action is favorable. The market is up more than 2.0% on the news, confirming support at the 30-day moving average and a long-term uptrend. The move has the market on track to retest the current high soon, and a new high could be set. In that scenario, the new high could trigger an influx of capital to drive this market up to the high end of the analyst's range near $130, another 20% upside from consensus.

$5k to $1.3m in just 3 trades

It doesn't happen often, but occasionally, something completely unique comes across my radar.

In this case, I'm talking about legal "Insider Trading".

Traders who have consistently signaled 453% … 610% .. and even 1036%... gains.

And until now they have been doing it completely under the radar.

In an upcoming interview I am revealing the strategy behind this gold-mine and how you can piggy back their every trade.

A Hidden Gem Retailer With 20% Upside

“Be fearful when others are greedy, and greedy when others are fearful.”

Warren Buffett said it best: Great investing often involves seeking out unloved names that the market has overlooked or undervalued.

While it's tempting to buy popular stocks like NVIDIA (NASDAQ: NVDA) and Tesla (NASDAQ: TSLA), these high-flyers don't always offer the best returns because much of their potential is already priced in (or worse, overestimated).

And that’s exactly how Buffett and Charlie Munger made a career: finding stocks discarded by markets but still offered great value.

Today, we’ll introduce you to a stock on the cusp of a turnaround. When sentiment is low, but the potential for recovery is high, a prime buying opportunity presents itself.

Let’s dive in.

Ethan Allen Interiors Inc. (NYSE: ETD) is a renowned interior design company that manufactures and retails high-quality home furnishings. The company focuses strongly on the premium, upper-end market segment, with 75% of its products custom-made in the United States.

Despite recent challenges, Ethan Allen’s strong financials and strategic initiatives make it a compelling addition to your portfolio.

Signs of Recovery

The home furnishings industry has experienced a downturn over the past few quarters as consumer spending normalized after the pandemic-induced surge. However, there are promising signs of a potential turnaround.

First, remote work is here to stay. BCG's "Workplace of the Future" survey reveals that companies expect approximately 40% of their employees to utilize a remote working model in the future. This is particularly relevant for Ethan Allen’s premium market segment, which is less affected by broader economic concerns like elevated inflation and interest rate uncertainties.

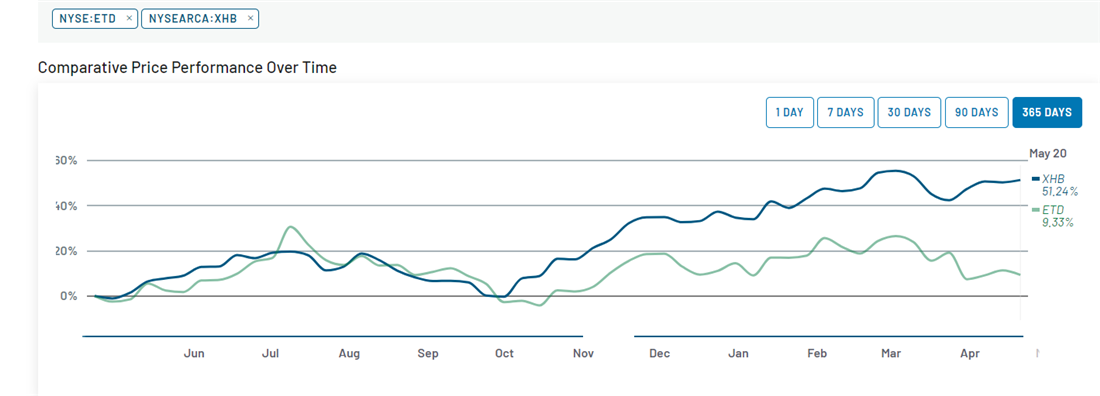

Homebuilding Catch-Up

The housing shortage in the U.S. is not news; it’s a chronic issue that’s been decades in the making.

Homebuilders are responding and rising to the challenge, unbothered by high mortgage rates.

According to FastCompany, the 10 largest publicly traded homebuilders brought in 18% higher new home orders in Q1 2024 than in Q1 2023, a period when builders were still adjusting to the 2022 mortgage rate shock.

Do you know what new homes mean? New furniture.

The chart shows what the market is missing—Ethan Allen and the furniture industry in general are due to catch up to the homebuilding boom.

Get Paid to Wait with Reliable Dividends

Despite recent underperformance, Ethan Allen’s financial health remains solid. The company has been paying dividends consistently for the past 29 years, through bull, bear, and sideways markets.

They posted a 61% gross margin in Q1 2024 and hold $181 million in cash with no outstanding debt. This solid financial footing has enabled Ethan Allen to increase their quarterly cash dividend from $0.36 to $0.39 per share, yielding 5.3% at current prices. This yield is higher than those of larger competitors like La-Z-Boy (NYSE: LZB) and RH (NYSE: RH).

A Challenging Quarter, But Bright Spots Shine

In the first quarter of 2024, Ethan Allen faced some hurdles. Net sales declined by 21% year-over-year, and net income dropped by 42%. These declines were largely due to a general dip in demand for home furnishings across the US.

However, the company’s resilience came through as gross margins (60%+) far surpassed the industry average of around 40%. The company is also in the process of re-designing its 175 design centers, partnering with influencers to increase their visibility and market reach.

In addition, the fact that 75% of the company’s custom-built furniture is made in the USA shields it from supply chain disruptions like those experienced during COVID-19. Manufacturing-heavy companies took note - manufacturing jobs listed went from 153k in 2020 to over 400k in 2023.

Conclusion: Ethan Allen Stock Forecast

While Ethan Allen’s sales and profits have declined recently, the potential for recovery is evident. The company’s strong financial position, strategic initiatives, and high gross margins provide a buffer against industry headwinds.

Adding Ethan Allen to your portfolio could be smart, capitalizing on tradition, innovation, and reliable dividends.

How to Trade Zero-DTE Options

Zero-DTE options are the newest (and hottest) options to trade. Professional traders have rushed into the market and are making a mint. Don't get left behind - learn all about these options, how to trade them, market setups to profit from, Plus much more.

Download Your Free "Zero-DTE Options Trading Secrets" report NOW!

Zoom Stock's Earnings Volatility Picked Up a Lot of Buyers

After reporting its first quarter 2024 earnings report, shares of Zoom Video Communications Inc. (NASDAQ: ZM) shook markets by initially plummeting as much as 4.6% from their closing price and swiftly rising back to show a 2.5% premium to the day’s end. To put this price action simply, a significant amount of buying orders could have come in as Zoom stock hit its bottom in the after-hours.

While nothing regarding price action can be taken as fact, investors can dig into the quarter's actual results to find a more substantial—more justifiable—basis for considering adding Zoom stock to their watchlists today. As it will soon become apparent, investors should tread carefully around the business services sector and be pickier with their selected stocks.

Compared to peers like Workday Inc. (NASDAQ: WDAY) and Twilio Inc. (NYSE: TWLO), Zoom remains a top choice for Wall Street analysts. It’s got everything to do with the company’s fundamentals. Before investors jump into the details behind Zoom’s results (and future expectations), here’s why the company could still be relevant in the years to come.

A Shift in The Economy

After sending out expansionary readings consecutively monthly since 2020, the ISM services PMI index suddenly turned to the downside, giving markets a surprising contraction reading for April.

Now that the U.S. gross domestic product (GDP) growth rate slowed to 1.6% for the past quarter, investors could be worried that this contraction may become a consistent trend for the sector. However, not all hope is lost.

Because the services sector has been responsible for pushing out most of the economic growth since 2020, as the ISM manufacturing PMI index has been in contraction for the past 15 months, it is unlikely that the Fed will let it go down in flames.

The Fed’s proposed interest rate cuts could aid this sector, allowing cheaper – and more accessible – financing for technology stocks looking to grow. What better way to streamline the new hybrid work environment than to add Zoom’s services?

As one of the top choices in the market, Zoom now holds up to 57% of the video conferencing software market. Because of this wide adoption rate and market penetration, the company made it to the desks of a few Wall Street analysts.

Is there any Upside Left for Zoom Stock?

Those at J.P. Morgan Chase & Co. saw fit to boost Zoom’s price target to $80 a share, directly daring the stock to rally by as much as 25% from its current price.

As bullish and optimistic outlooks are often contagious, analysts at Mizuho Financial followed along with a $90 valuation for Zoom, a bolder stance calling for a 40.4% upside from today’s price. However, Mizuho went even a step further in their view of Zoom.

Over the past quarter, Mizuho doubled its stake in Zoom stock, bringing the bank’s total investment in the company up to $2.4 million today. Considering that the stock trades at 84% of its 52-week high, a bullish bet on top of already bullish momentum must be driven by fundamentals.

A Stellar Start to The Year

Zoom trades at a P/E valuation of 31.3x today, which offers investors a discount of up to 37.6% to Workday’s 50.2x P/E ratio.

Because Twilio has no net profit, investors can use its future earnings expectations, which trade at a forward P/E ratio of 19.6x today. Comparing this valuation to Zoom’s 12.9x forward P/E, investors get another 34% discount on Twilio’s.

Now, taking advantage of these discounts, here’s where investors can lean to get a solid footing. In the first quarter, Zoom generated up to $588.2 million in free cash flow (operating cash flow minus capital expenditures), a 40.6% increase from the previous year.

With this new free cash flow, management immediately looked to deploy up to $2.4 million into buying back stock, crystalizing that the stock seems cheap today even in the face of insiders themselves.

The company’s financials show a gross profit margin of up to 76.3%, which is characteristic of software companies. In this fashion, management has ample room to stay on track for further quarters of positive free cash flow, allowing for more significant shareholder returns.

Over the past 12 months, Zoom generated return on equity (ROE) rates of 5.2%, which grew from 2.5% by the end of 2023. Keeping this expansion rate, Mizuho could be proven right in their bullish bets on Zoom stock.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 TJX Companies Can Hit New Highs; Double-Digit Upside to Follow"

Post a Comment