Ticker Reports for October 6th

Top Streaming Companies: Who's Winning the Battle?

Though wildly popular with consumers, streaming companies have long struggled to achieve and maintain profitability. Over time, this has led providers like Netflix Inc. (NASDAQ: NFLX) and Paramount Global (NASDAQ: PARA) to experiment with tiered subscriptions involving advertisements, bundle offers, and a crackdown on password sharing, among many other strategies. Critics of streaming firms say that the massive price increases for most plans and the structural changes—combined with the proliferation of streaming platforms and the subsequent need for households to subscribe to multiple services to have the same breadth of viewing options—means that streaming has become increasingly like cable television.

NFLX: Big Earnings Growth Amid Shift to Ad-Supported Plans

Shares of streaming titan Netflix are up an astounding 87% in the last year. The company reports earnings in mid-October, and analysts again have an optimistic view, including an estimated 36% year-over-year improvement in earnings per share.

For Netflix, outperformance has become a norm to the extent that the company's share price sometimes reacts negatively, even following a strong earnings release. For example, after its second-quarter earnings release over the summer—when Netflix notched a 16.8% increase in quarterly revenue based on more than 8 million new subscribers—shares fell by about 1.5% based on lackluster third-quarter guidance.

Still, Netflix offers a strong return on equity of 32.9%, meaning that it able to efficiently use investments to generate profit. And the company has so far been successful at enticing users to its ad-supported plans, which helps to drive revenue growth.

DIS: Profitability and Price Hikes

Unlike Netflix, the Walt Disney Co. (NYSE: DIS) includes a great deal of other entertainment-related business lines in addition to streaming through its Disney+ platform. Since 2023, the company has eliminated several thousand positions in a cost-cutting measure aimed, in part, at combating a poor environment for ad sales.

Disney's efforts to trim costs have benefited its streaming business, which posted a notable first profit in the most recent quarter. Like Netflix, Disney has also cracked down on password sharing among members and is now offering a paid sharing option as a way of further boosting revenue.

Finally, Disney will increase prices on many of its streaming subscription plans and bundles in October, which will likely measurably benefit its bottom line now that it has achieved profitability in this space.

WBD: Significant Partnerships, But Declining Share Price

Warner Bros. Discovery Inc. (NASDAQ: WBD) is best known in the streaming space for Max (formerly HBO Max), as well as the lesser-known platform Discovery+. This firm has also engaged in multiple rounds of layoffs in recent months in an effort to limit costs.

WBD shares have lost about a quarter of their value in the last year and analysts remain cautious, rating the company a "hold" overall despite a consensus price target implying more than 40% upside potential. Weighing on the price of shares is the company's large pile of debt following the 2022 merger of WarnerMedia and Discovery.

On the plus side, Warner Bros. Discovery's streaming business is growing and now includes well over 100 million subscribers globally. The company's recent partnership with All Elite Wrestling could corner a sizable market for years to come. And Warner Bros. Discovery surprised the streaming world when it announced that subscribers of Spectrum, the cable TV offering of Charter Communications Inc. (NASDAQ: CHTR), would also receive access to WBD streaming platforms, another bid to grow the user base.

Subscriber Growth Remains Key

The long-term metric by which investors have judged streaming platforms is the rate of growth of subscribers to these services. Given the intense competition among a large number of rivals, the ability to quickly capture a sizable share of the market is essential to any successful streaming company.

There is no doubt that subscriber growth remains an important factor to consider when looking at streaming firms. However, now that an increasing number of these companies are becoming profitable—or their streaming segments are becoming profitable—investors might also look to more traditional signs for clues as to the sustainability of these profits over time. Besides top- and bottom-line growth, debt loads, price/earnings and price/sales ratios, and other gauges of fundamental financial health are increasingly important.

They laughed when he picked Nvidia in 2016…

Everyone's talking about AI right now, but I've been talking about it for years.

And now I've just released my latest prediction and believe it or not, I'm advising NOT pour all your money into Nvidia right now

The Outlook for Interest Rate Cuts Got Blown Out of the Water

The September NFP was so smoking hot that it blew the outlook for interest rates out of the water. The headline figure alone was enough to alter the outlook, signaling healthy, resilient labor market conditions, and the revisions sealed the deal. Revisions averaged 72,000 higher monthly in July and August, belying fears that a recession was near. The takeaway for investors is that the FOMC is unlikely to continue with aggressive interest rate cuts and may even pause due to labor market health. Their dual mandate is in balance with labor markets showing strength, inflation trending quickly toward 2%, and the risk of inflationary acceleration back on the table.

Wage Growth Soars in September: Labor Market at an Inflection Point

Not only was job creation strong, but wage growth was robust. The average hourly wage rose by $0.13 with revisions, up 0.4% monthly and 4.0% compared to last year. The data is trending higher, with YoY wage-level inflation back at 4.0%, sufficient to give the FOMC reason to pause. The not-adjusted as-reported data is more compelling, with monthly gains at 0.8% and 4.5% YoY, suggesting sustained consumer health through the holiday season.

As reported by Challenger, Gray & Christmas, hiring intent is also strong. The 403,891 job openings announced in September are seasonally expected and show sustained labor market strength. However, only some of the news is good. The Challenger, Gray & Christmas report also shows the labor market at an inflection point where Senior Vice President Andrew Challenger says it could begin to stall or contract.

The most telling data points are the surge in job cuts, hiring intent, and trends. The 72,821 job cuts announced in September are up 53% compared to September 2023, hiring intent is down compared to last year, and September is the first month 2024 figures surpassed 2023. The 2024 YTD total is only 0.8% above 2023, but it is trending in the wrong direction and could lead to labor market contraction. Regarding the GDP outlook, the Atlanta Fed’s GDPNow tool continues to track in the 2.75% range, well above the analyst consensus and the forecasts for the year.

Overly Optimistic Market Still Expects Two More Cuts By December

The outlook for FOMC interest rate cuts, as forecasted by the CME’s FedWatch Tool, has softened but continues to price at an aggressive pace. The market is pricing in 100% chance for 25 basis points in November and December and another 100 bps by the end of the following year. While cuts will likely continue, the pace will likely be slower than what is currently priced in. The next FOMC meeting is weeks away, with numerous data points still due, including a reading of PCE and the CPI.

Oil has reemerged as a threat to inflation. The oil price is trading near the bottom of its long-term range but showing a clear bottom driven by geopolitical tensions. The market is well-supplied, but there is a significant risk of disruption in the Middle East, and price action in WTI is set to move higher, given the catalyst.

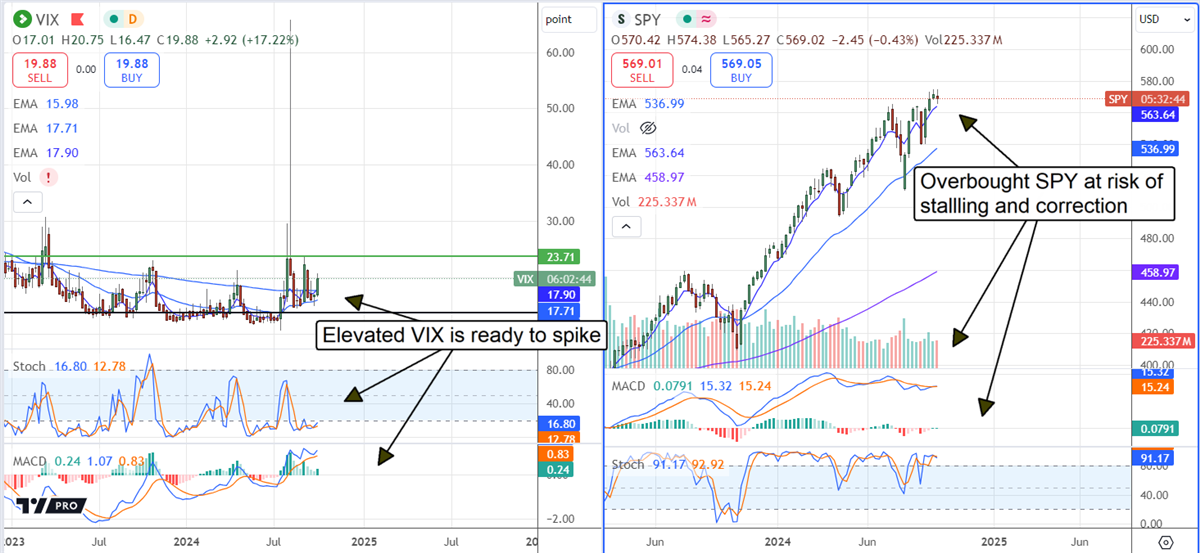

The S&P 500 Stalls Near Record Highs

The S&P 500 (NYSEARCA: SPY) responded favorably to the news, moving higher in early premarket trading, but could not hold the gains. Selling was equally tepid, leaving the market up daily but showing resistance at a critical level, just below the record highs. The takeaway is that market action remains mixed, with no clear indication of direction, and risk is skewed to the downside. As the VIX (CBOE: VIX) indicates, the risk of a major correction remains elevated, with the fear index trading well above the 2024 lows and indicated higher.

Tim Sykes' Urgent Trade Alert: "Make this move now"

WARNING: 80 Wall Street banks are gearing up for MASSIVE D.C. shock

This $2 trillion D.C. shock is NOT about Trump or Biden dropping out of the race…

3 High-Risk, High-Reward Micro-Cap Stocks You Shouldn't Ignore

Micro-cap stocks are typically categorized as companies with market capitalizations between $50 million and $300 million. However, it’s not a hard-and-fast rule. Many small stocks can fluctuate massively in price over a short time. This can put their value inside or outside that range on a given day.

Picking micro-cap stocks can yield massive returns but can also be extremely risky. For example, when NVIDIA (NASDAQ: NVDA) went public in 1999, the company had a market capitalization of $279 million. Holding that investment from then to now would have generated a total return of over 300,000%. In other words, a $10,000 investment in 1999 would have turned into over $31 million.

However, micro-caps can also result in shareholders losing all of their investments. SunPower (NASDAQ: SPWR) is a recent example of this. The company traded in the micro-cap range for several weeks before the NASDAQ delisted it on Aug. 16. It filed for Chapter 11 bankruptcy and is now worth nothing.

Below are three micro-cap stocks with significant potential and significant risk. They sit within or just outside the $50 million to $300 million market capitalization range.

Can Rent the Runway Get Back on Its Feet?

Rent the Runway (NASDAQ: RENT) made a strong name for itself as one of the first entrants into the clothing rental space. The company allows customers to rent uber-expensive designer clothing, costing them much less than buying it outright.

It is improving its financial situation and expects to break even on cash flow this year. However, subscribers to its service are declining as competitors are seeing massive growth.

The rapid expansion in subscribers for competitor Nuuly shows that there is growth to be had in this market. Rent the Runway’s valuation is extremely low, but reinvigorating growth is essential to its long-term success. In August, the company saw a 20% increase in orders in its “reserve” segment, which helped create a flywheel effect to attract more monthly subscribers.

Additionally, the company says the improvements in its website have “almost doubled checkout completion rate compared to the first half of the year.” This means customers are buying products more often rather than leaving them in their cart. Lastly, the company hired a new Chief Marketing Officer in March to reignite customer interest.

374Water’s Hopes Lie in Central Florida

374Water (NASDAQ: SCWO) is a wastewater treatment company that is developing a new technology for this industry. It is currently at a crossroads as it tests its products with the City of Orlando.

If the tests are successful, the city said it intends to purchase multiple units from the company.

These purchases would mark the company's first significant revenue. The firm announced just last week that its systems are up and running in Orlando and should provide periodic updates about the project. The company will also use its Orlando operation to demonstrate the tech to potential federal and industrial customers. So, it may be able to parlay this into many more customers than just the city.

These updates will be key tests of the technology. They should greatly affect 374Water's chances of long-term commercial success.

Skye Bioscience: A Weight Loss Drug Boom or Bust?

Last on the list is Skye Bioscience (NASDAQ: SKYE). Skye is a clinical-stage pharmaceutical company that is developing a different type of weight loss drug. Recently, GLP-1 agonist drugs have seen massive commercial success. Skye’s drug, nimacimab, is a CB1 inhibitor. It is intended to have similar weight loss effects as GLP-1 drugs like Ozempic and Zepbound but works through a different mechanism.

The hope is that the successful development of a CB1 drug could open up a new market of customers who respond better to its mechanism of action compared to GLP-1s. CB1s could also possibly be used together with GLP-1s to compound their effects. However, CB1s have a history of inducing negative psychological effects. Novo Nordisk’s (NYSE: NVO) CB1 inhibitor was shown to have those same problems in recently released results, which caused the company’s shares to fall 5% in one day. However, the drug did show adequate weight-loss effects.

Skye released a statement about Novo’s results, stating that the weight loss results validate Skye’s drug. At the same time, Skye laid out a case for why its drug could mitigate the negative psychological effects. Skye could have a blockbuster drug if nimacimab gets through all Food and Drug Administration trials. But it still has a long way to go, having entered Phase 2 trials in August.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 3 High-Risk, High-Reward Micro-Cap Stocks You Shouldn't Ignore"

Post a Comment