Sponsored content from WealthPress Hey, Lance here. Let’s say it. Tesla’s in the toilet.

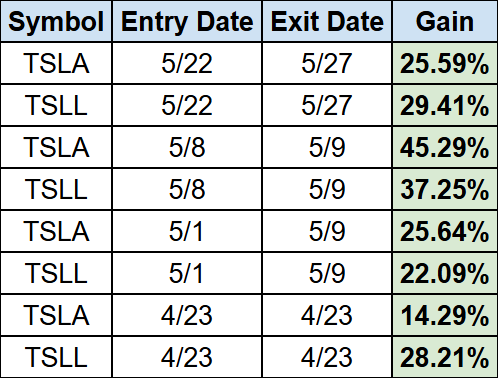

They dropped 13% in Q1… they’re pacing up to 90,000 units behind last year… and all while the rest of the market is booming. But Tesla? Rising competition… production setbacks… and Elon’s political distractions. Now, most traders are either backing away from Tesla or betting blindly on a bounce. But not me. I’ve been tracking a specific pattern in Tesla for over two years. One that allows me to not care whether the company beats expectations or crashes and burns. We’ve been able to make money either way. And lately, I’m on a run of 8 straight winners with gains reaching upwards of 45%.

While not every trade pans out, here’s the kicker: These setups don’t require Tesla to move in any specific direction. All I need is the kind of volatility Tesla brings to the table. And I know exactly how to trade it. I won’t promise results for you, but if you want to know how I do it, I’m sharing everything. The exact setup, key price levels, and how I plan to play the next big Tesla move. If you’re still trading based on headlines… you’re already late. Let me show you a smarter way.

By clicking the link above you agree to periodic updates from ProsperityPub and its partners (privacy policy) Lance Ippolito

Monday's Bonus Story 3 Retailers Poised to Outmaneuver Tariff and Recession ConcernsWritten by Nathan Reiff

Key Points - Retail stocks may be among the hardest hit by the Trump administration's tariffs, ongoing inflation concerns, and the risk of an impending recession.

- Still, a handful of retailers and companies serving the industry may have found ways to maneuver around these barriers.

- TJX, GLBE, and BOOT might be worth a closer look heading into the second half of 2025.

Several months into the Trump administration's unfolding tariff program, investors are still unlikely to have much clarity surrounding the impact of current and potential future levies. However, as inflation creeps upward once again and analysts continue to forecast a decent likelihood of an impending recession, it would seem to be an increasingly challenging time for companies dependent upon consumer spending. The SPDR S&P Retail ETF (NYSEARCA: XRT), an exchange-traded fund (ETF) and benchmark for the U.S. retail industry, has partially recovered from the initial April tariff shock but remains down more than 1% year-to-date (YTD). At the same time that some retailers are struggling to adapt to shifting economic conditions and tariff landscapes, others may be able to buck the trend and thrive thanks to their unique focus or business model. Below, we explore three companies—an off-price retailer, an e-commerce provider, and a specialty footwear firm—that analysts believe could outperform despite a challenging environment. Resilient Model, Top- and Bottom-Line Growth, Dividends...But Valuation Risks TJX Companies (NYSE: TJX), the company behind discount and closeout shops like T.J. Maxx, Marshalls, and HomeGoods, has only slightly outperformed the XRT since the start of the year. TJX has maintained brick-and-mortar strength even as shopping trends have shifted online, thanks to its distinguished model, in which customers search through stores for discounted finds. The firm also maintains its cost efficiency by focusing on overstocked inventory, which it can then turn around and sell below competitor prices. The proof is in TJX's earnings, and the company recently came out ahead of analyst predictions for both revenue and EPS. Revenue climbed by more than 5% year-over-year (YOY), a sign that both U.S. and, increasingly, international operations are growing well. TJX also offers the bonus of a solid dividend, with a yield of 1.41% and a healthy payout ratio suggesting continued long-term dividend sustainability. Management recently boosted the company's dividend payout, further solidifying optimism in the company's ability to withstand external pressures. Nineteen out of 20 analysts see TJX shares as a Buy, predicting that the stock could rise by more than 17% based on a price target of $141.06. Investors should keep in mind, however, that with a trailing P/E ratio of 28.7, TJX stock may not offer the most compelling value at this time. High-End Retail Platform and Major Revenue Improvement Global-e Online Ltd. (NASDAQ: GLBE) offers a cloud-based platform to facilitate international retail transactions. The company doesn't interface directly with consumers, but rather connects businesses via its services. GLBE's inclusion in a list of retail-focused firms able to successfully navigate a complex tariff situation may be surprising, given its international focus. However, the company's business clients are predominantly high-end and luxury brands, including Hugo Boss, Parisian shoe brand Carel, Iconic London, Loquet, and others. Customers seeking out the brands doing business with Global-e likely have significant flexibility on their discretionary spending, with or without tariffs. What's more, Global-e is expanding its partnerships in a big way—the company recently announced a major multi-year agreement with commerce platform Shopify Inc. (NYSE: SHOP)—a move that should help it continue to grow its top line. There is already noteworthy momentum there, as Global-e announced quarterly revenue growth of 30% YOY for the latest quarter, coming in above analyst predictions. Analysts are bullish on GLBE shares, with 12 out of 13 calling them a Buy. A consensus price target of $48 per share suggests 49% upside potential. Sales Growth and Realistic (But Positive) Projections Drive Boot Barn's Rally Boot Barn (NYSE: BOOT) is a footwear and apparel retailer that serves customers interested in Western-inspired fashion and those looking for durable workwear. Consolidated same-store sales growth for the latest fiscal year was 5% YOY, and the firm is looking to increase its store count by 14%. The company, which relies on products from China and Mexico, has taken a sensible approach to pricing and forecasting given the tariff uncertainty. Even still, it is projecting 13% growth in total net sales. Unlike the two companies above, BOOT shares are notably up in recent months. The stock has risen by almost 9% YTD and an impressive 27% in the last year. Analysts remain optimistic about future growth despite the recent rally; a consensus price target close to $174 means the company has over 5% in upside potential based on the latest predictions. Twelve out of 13 analysts say BOOT is a Buy.

|

0 Response to "Tesla Sales Plunge"

Post a Comment