|

|

|

Hey Folks, Brandon here. |

The math is ugly right now. Any positive news this week probably won't be received as positively as negative news gets punished. |

That's not market opinion - that's what institutions are pricing. The skew index just dropped from nosebleed levels of 160 to 145 on Friday. |

Still high. |

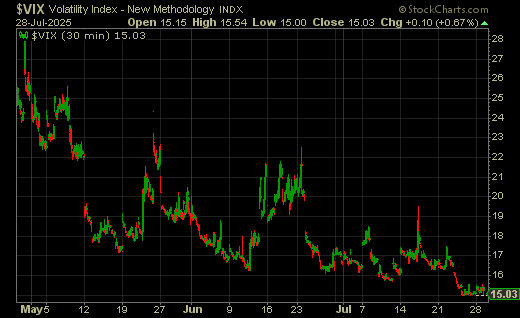

The three-month VIX is 22% higher than spot VIX - highest level since December 24th and February 14th. |

Translation: Big money expects volatility. Soon. |

|

|

|

The Asymmetric Risk Problem |

Look at Google's earnings. Good numbers, not rewarded. Tesla missed, big gap down. We've got Microsoft, Meta, Amazon, and Apple all reporting this week - four of the MAG 7 representing massive S&P 500 weight. |

Add the FOMC statement Wednesday and potential China tariff news August 1st, and you've got a perfect storm where beating expectations might get you flat while missing gets you crushed. |

When risk is this asymmetric, you need to position accordingly. |

The Volatile Stock Reality Check |

Take SIDU - down 40% today. Not even earnings. Just Monday. |

Rocket Lab could drop 30% tomorrow on any headline. These stocks trade with 92% implied volatility while the S&P sits at 15%. Their beta says "two times more volatile" but reality is five to six times. |

You can't hedge these individually. Portfolio-level hedging won't help when the S&P drops 5% and your speculative names drop 50%. |

What I'm Doing About It |

First step: Take 30% profits. Not losses - profits. Raise cash in the volatile names that have run on short squeezes. |

Second: Hedge the correlated positions with a specific strategy. |

Here's the exact mechanics on a $100,000 S&P-correlated portfolio: |

The Trade: |

Portfolio: 157 SPY shares (157 delta exposure) Reduce by 30%: Target ~50 delta reduction Buy: 2 SPY puts, 30-delta, 39 days out (currently 621 strike) Sell: 4 SPY calls, 40-delta (currently 644 strike) Net cost: Approximately break-even (put cost offset by call premium)

|

The Result: |

10% market decline: Down only $269 instead of $10,000 10% market rally: Capture $7,600 instead of $10,000 Portfolio delta reduced from 154 to 63

|

You give up some upside to eliminate most downside. |

The Management Strategy |

If SPY drops below your long put strike (621), roll it down. Sell the 621 put, buy a new 30-delta put. You've just booked roughly $1,000 profit while maintaining your hedge. |

Close the call spread for about 10% of premium - maybe $100 total. Now you've got a profitable put hedge in place and cash to deploy. |

One client just captured $50,000 using this approach during the recent selloff. That's real money that can be redeployed when opportunities emerge. |

The Bigger Picture |

We're sitting with VIX at low levels, skew high, and forward volatility expectations at extremes. This has been a timely indicator historically. |

If you're not taking profits now, when? If you're not hedging now, when? |

Waiting for the correction makes everything harder and more expensive. You'll end up buying in-the-money puts or using futures - much messier strategies. |

The Choice |

|

QuantumScape went from $4 to $15. Virgin Galactic from $2.75 to $4.60 (after hitting $6.50 before the last decline). |

These could be down 40% tomorrow. With earnings season ramping up and multiple risk events converging, this seems like as good a time as any to book gains and reduce risk. |

The market is telling you through options pricing that volatility is coming. The skew is telling you downside risk exceeds upside potential. |

That, my friends, is significant information you can act on. |

Don't wait for the correction to make everything harder and more expensive. |

Watch the full video breakdown where I walk through these exact hedge mechanics step-by-step - CLICK HERE |

Take Care, |

Brandon Chapman |

|

|

0 Response to "The Math is Ugly Right Now"

Post a Comment