| WEEKLY ROUNDUP There’s a Limited Window to Buy This AI Play – and I’ve Pinpointed When That Is VIEW IN BROWSER Hello, Reader. In 1440, Johannes Gutenberg introduced the movable type printing press. This was a watershed moment for democratizing knowledge. Suddenly, books no longer had to be copied by hand. The printing press could do so by the thousands. Today, AI is facilitating a similar push to democratize knowledge. It’s a tool that lets non-coders create workable software… non-writers to generate novels… and non-artists to produce paintings. Now, over the next several years, we’re going to see AI replace some of the most crucial jobs that allow ordinary Americans to keep food on the table. And once that starts happening, mass unemployment could quickly follow. So, to keep up with the AI Revolution, it’s essential to buy into the firms that will rise with this new technology rather than be replaced by it. That is why I like to look at every perspective investment through the lens of AI. Specifically, I look for the best-of-breed companies that… - Provide essential components or infrastructure for AI technologies.

- Apply AI in cost-effective and/or market-leading ways.

- Possess some sort of durable immunity to the destructive powers of AI.

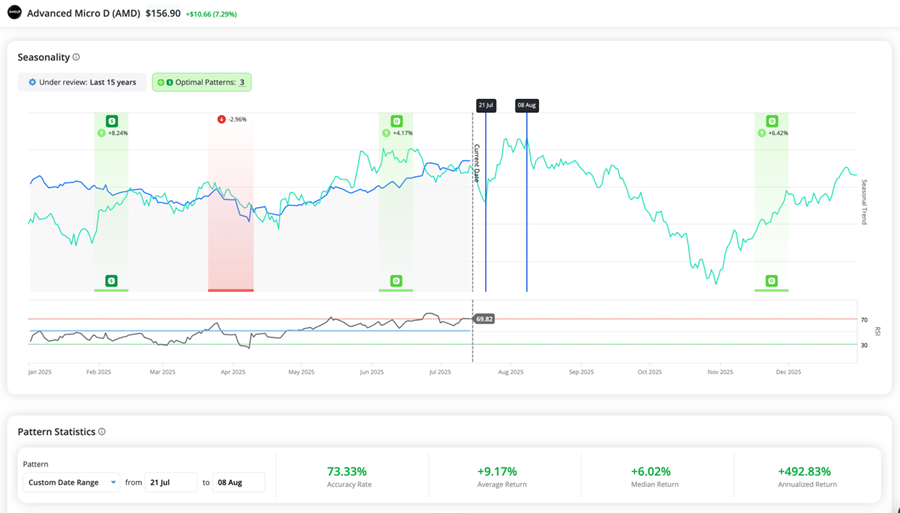

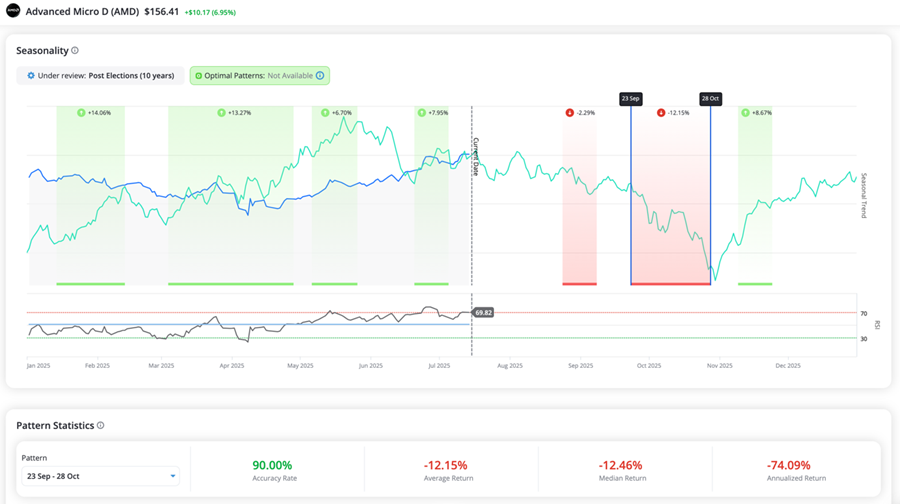

One particular company falls squarely into the first category. It is a major supplier of cutting-edge semiconductors that has become a major player in many facets of AI technologies, and it is doing so very profitably. The company has scored some impressive recent successes, boosting its share price nicely. The company I’m talking about is Advanced Micro Devices Inc. (AMD). During the early phases of the AI boom, AMD seemed to operate in the shadows of its high-profile, and widely adored, competition. Most folks viewed the company as an also-ran compared to the AI-chip leader, Nvidia Corp. (NVDA). However, AMD is making major strides toward becoming a worthy competitor to Nvidia in the data center chip sector. While Nvidia still dominates the AI chip market, AMD is quickly gaining ground. The company’s latest data center GPUs – the Instinct MI350 series, set to launch in the third quarter of 2025 – offer greater memory capacity and better or similar AI performance compared to Nvidia’s top-tier Blackwell chips, which AMD describes as “significantly more expensive.” This value proposition is key to AMD’s strategy of disrupting Nvidia’s high-margin dominance. That pricing advantage could be the key to eroding Nvidia’s AI chip margins – which have already shown signs of softening. As Nvidia’s margins decline, AMD’s are trending higher, creating a clear opportunity for margin expansion and profit growth. AMD’s data center segment is already delivering strong results. In the first quarter of 2025, it posted 69% year-over-year growth and contributed 57% of total gross operating income – a major shift toward high-value enterprise AI workloads. AMD is an outstanding long-term play on the exponential – growth of AI technologies. I first recommended it to my Fry’s Investment Report subscribers back in March. In the four months since then, the company has achieved a 60% gain. As I stated in my initial trade alert… Anyone who bought the shares of today might not be happy about that purchase one week from now, or even one month from now, but I believe they would be very happy about it one year from now. So far, so good. But it gets better… I plugged AMD into the seasonality pattern-spotting tool created by our partners at TradeSmith – and it tells me that a new window to buy this company is coming soon. I’ll share the “Green Day” chart that the tool generated – and when exactly it tells us to start buying AMD – below. But first, let’s take a look back at what we covered here at Smart Money last week… |

0 Response to "There’s a Limited Window to Buy This AI Play – and I’ve Pinpointed When That Is"

Post a Comment