“If it keeps on raining, the levee’s going to break.”

– Led Zeppelin, 1971

That might sound like rock poetry.

But it’s also one of the sharpest ways I’ve heard to describe the way financial collapses unfold… right up there with Ernest Hemingway’s famous line about going broke: “Gradually, then suddenly.”

Make no mistake, it’s raining right now.

In July, the U.S. Treasury announced something most Americans will never see on the front page:

They’re planning to borrow $1.01 trillion this quarter alone.

That’s nearly double what they forecast just months ago… a record surge in government borrowing as they scramble to refill depleted coffers.

This isn’t normal. It’s not prudent.

And it’s certainly not what Trump promised when he returned to power.

It’s panic-level fiscal behavior. And if you don’t have a plan to protect your money and move to safer, smarter ground you could be swept away by what’s brewing.

That’s why I’m reaching out today.

Because I believe we are now entering America’s breaking point – and the time is going to come far sooner than most people are ready for when the cracks tear wide open.

I take no pleasure in revealing that the process has already begun. And I believe the aftermath will divide America into two camps: rich and poor.

I’ve just recorded a new emergency briefing to help you understand what’s happening and how to get on the right side of it.

You’ll discover:

- Why this new wave of panic borrowing is even more dangerous than it appears

- How Trump’s policies are accelerating the crisis

- And what I believe you must do now to prepare… including three investments that could benefit as capital rotates aggressively into safer, harder assets

Zeppelin wasn’t writing about national debt, but the sentiment is on the money…

“Crying won’t help you, praying won’t do you no good…”

Sitting back and hoping for the best is the worst thing you can do right now.

You’ve got to get ahead of this and take serious preparatory action.

Let me show you how my team and I are doing this, before the levee breaks:

Good investing,

Porter Stansberry

DraftKings Posts Record Quarter, Eyes Profitability

Written by Chris Markoch. Published 8/8/2025.

Key Points

- DraftKings beat Q2 estimates with record revenue and GAAP EPS of 30 cents.

- Management raised full-year revenue and adjusted EBITDA guidance.

- Technical setup and a golden cross suggest a potential breakout ahead.

DraftKings Inc. (NASDAQ: DKNG) reported record revenue and earnings in its second-quarter 2025 earnings report. This was expected, as DKNG stock was up approximately 11% in the month before earnings, and analysts had been raising their price targets.

But even investors may have been surprised at the magnitude of the beat on the top and bottom lines. In fact, DraftKings set records in both generating earnings per share (EPS) of 30 cents on revenue of $1.51 billion. The top-line number was 37% on a year-over-year (YOY) basis.

A highlight of the report was DraftKings' acknowledgment of higher sportsbook-friendly outcomes. The translation is: more customers lost their bets in the quarter. That worked to the company’s favor.

The company also raised its full-year guidance for both revenue and earnings:

- The new full-year 2025 revenue guidance is for $4.95 billion to $5.05 billion (previously $4.8 billion to $5.0 billion).

- The new full-year 2025 adjusted EBITDA guidance is for $460 million to $540 million (previously $410 million to $500 million).

Investors should focus on the company’s results, which the company believes put it on track for sustained profitability. Supporting that outlook was a 29% increase in average revenue per user and the YOY growth in iGaming revenue.

Seasonal Factors Impacted Profit

One reason DraftKings was able to book such a substantial profit is that the last quarter didn’t involve football. That may seem counterintuitive, but as the company's CEO remarked to CNBC’s Jim Cramer, DraftKings typically reduces its advertising and marketing spending after the Super Bowl in February. Therefore, more of its revenue can go directly to the bottom line. This has been true for the company since it went public.

The second quarter has been profitable, but the challenge is reaching full-year profitability. Like its competitors, DraftKings relies on heavy promotional spending, particularly during the American football season. That results in cash burn, which has held back the company’s share price. The company is seeing continued growth in the number of unique customers on its platform, so the strategy is working.

To that end, management is guiding to full-year profitability on an adjusted EBITDA basis. However, that doesn’t mean the next two quarters will be profitable on a GAAP EPS basis.

Is Growth Slowing or Stalling?

DraftKings continues to see slower growth in iGaming and active users as it expands into more markets. On the one hand, that's typical for any maturing growth company. However, investors may be concerned that the slowdown will show up in weakening engagement numbers.

That’s particularly true of iGaming, which has higher margins than sports betting, so any slowdown there could impact DraftKings’ path to profitability. Slowing monthly active user growth can also signal that the company is reaching saturation in early-entry states, putting more pressure on new markets to deliver.

DraftKings still trades at growth-stock valuations, so while some deceleration is expected, the company will have to show that this is a natural plateau and not an early sign of deeper issues with market penetration or user engagement.

No Prediction About Prediction Markets

The 2024 presidential election introduced many consumers to prediction markets, allowing them to wager on outcomes ranging from political races to major economic events.

DraftKings has since launched its own prediction markets in select states and jurisdictions. However, management has acknowledged that these products may fall under the oversight of the U.S. Commodity Futures Trading Commission (CFTC), which has some investors concerned.

In that scenario, the best-case situation would probably require a more complicated licensing process for such wagering. In a worst-case scenario, it would have to shut down these products.

To be fair, wagering in prediction markets makes up a small amount of DraftKings' revenue. However, investors were enthusiastic about the company's opportunity to expand beyond sports betting as this kind of innovation would help provide growth opportunities in a highly competitive market.

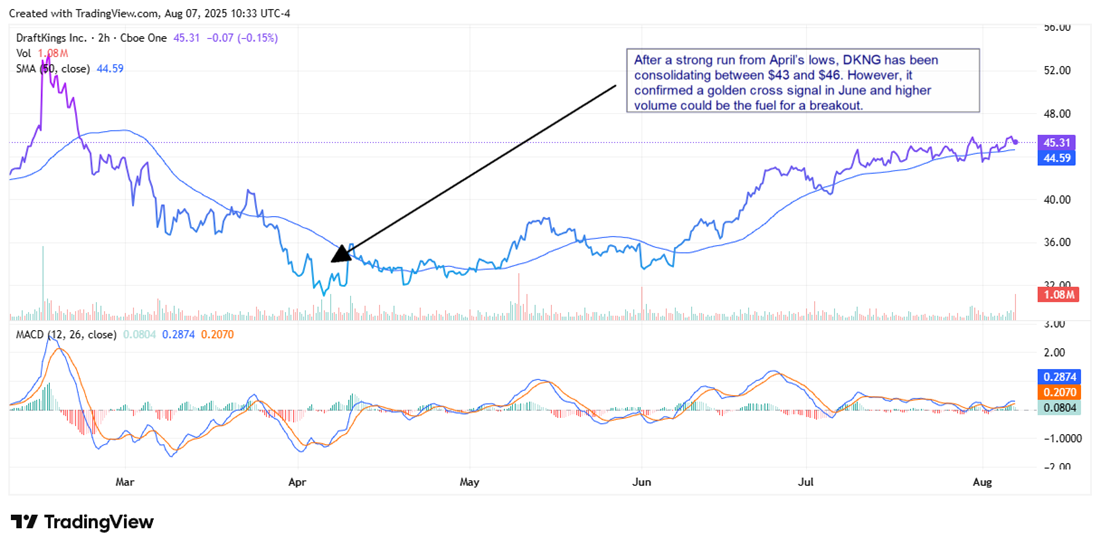

A Golden Cross Signal Could Be a Bullish Setup

DraftKings stock is up more than 20% in 2025, easily outpacing other consumer discretionary stocks.

It's also trading above its 50-day simple moving average (SMA) at $44.59. That line continues to slope upwards after the stock formed a golden cross signal in May that was confirmed in June, reinforcing the idea that a longer-term uptrend may be underway.

However, after a strong run from April’s lows, DKNG has been consolidating between $43 and $46. These earnings results, if supported by strong volume, could be a setup for a move higher.

Analysts have given DKNG stock a consensus price target of $54.48, which is 22% higher than its closing price on Aug. 6.

This email is a paid sponsorship provided by Porter & Company, a third-party advertiser of MarketBeat. Why was I sent this email message?.

If you have questions about your newsletter, don't hesitate to contact our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2025 MarketBeat Media, LLC. All rights protected.

345 N Reid Place #620, Sioux Falls, SD 57103. United States..

0 Response to "When the levee breaks"

Post a Comment