Warren Buffett is sitting on $325 billion in cash – his largest hoard ever.

Not because he wants to – but because he can’t find value in the usual places.

Now, as US government spending spirals out of control, Buffett knows he’s losing billions of dollars to inflation.

That’s why I predict Buffett’s next investment will catch millions of people off guard.

It’s not another bank… railroad company… or more shares of Apple.

It’s a gold company. How do I know?

Because the math doesn’t lie:

You can buy the average gold developer for $30 and get back $13 a year —

That’s a 43% ROI annually.

Over 10 years, that’s $130 on a $30 investment.

Tell me where else Buffett can get that.

But there’s one specific miner Buffett likes best:

- It’s the best-managed major gold miner in the industry…

- Has massive cash flow…

- Is trading at a deep discount to fair value…

- Positioned at the heart of Trump’s new mining push…

Don’t wait for Buffett to reveal his position in his 13F filing on November 15th…

Right now, you have the chance to front-run the greatest investor of all time. Go here and I’ll give you the name and ticker – along with details on my top four small miners.

To your wealth,

Garrett Goggin, CFA, CMT

Chief Analyst & Founder, Golden Portfolio

P.S. A lot of investors write in to tell me how much they’ve made in Bitcoin. My reply? Good for you. First off, gold investing is cyclical. You really only want to own gold at one specific time in the cycle. That time is now. Second, the world’s governments are not buying Bitcoin. They’re betting on gold. All of them. Bitcoin (does anyone really know for sure the US government didn’t create it?) will be a good bet… until it isn’t. It may end up doing great. Or it may be eclipsed by any number of tech developments.

Meanwhile, gold will continue to do what it’s done for almost 6,000 years of recorded human history: Protect wealth through chaos. Go here if you want the name and ticker of Buffett’s likely gold play… and details on my top four miners

Resideo Technologies: Institutional Activity Signals 30% Upside

Written by Thomas Hughes. Published 9/16/2025.

Key Points

- Institutional investors are heavily backing Resideo Technologies, signaling strong confidence and potential for upside.

- Recent technical breakouts and bullish analyst upgrades support a target price increase of 30% or more.

- Despite short-term risks like debt and rising short interest, long-term growth is supported by tech innovation, housing market trends, and operational clarity.

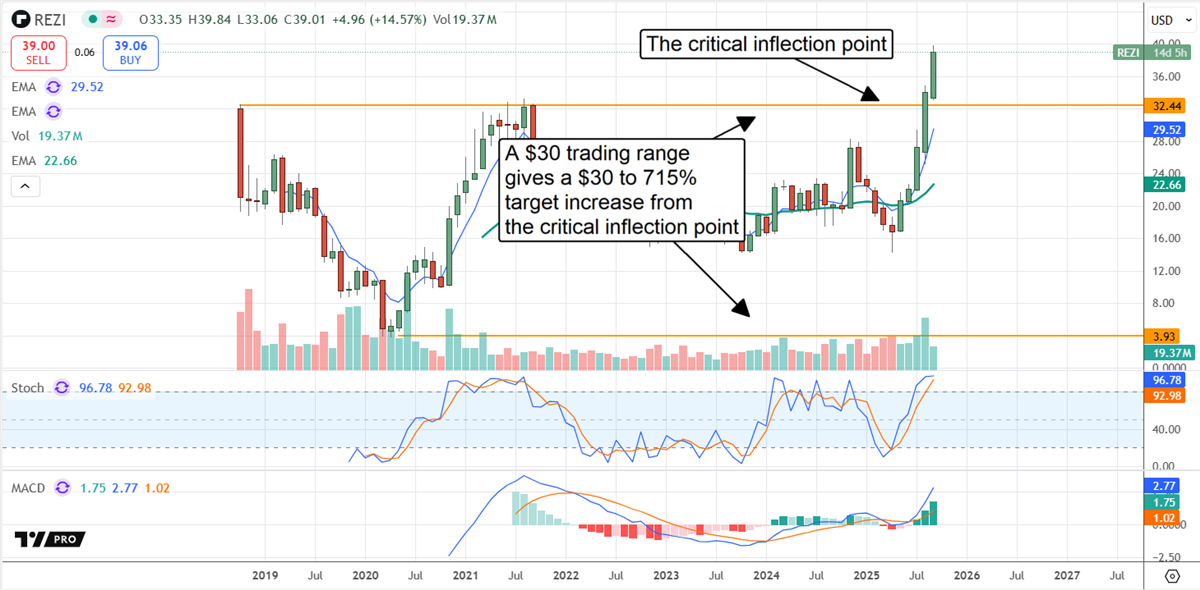

Resideo Technologies (NYSE: REZI) is attracting serious institutional interest, setting new records in Q3 2025 and underpinning a robust technical outlook.

The stock's recent breakout from a multi-year trading range lays the groundwork for a potential rally, with price targets suggesting an upside of roughly $28 from current levels.

$100 Trillion "AI Metal" Found in American Ghost Town (Ad)

Jeff Brown recently traveled to a ghost town in the middle of an American desert…

To investigate what could be the biggest technology story of this decade.

In short, he believes what he's holding in his hand is the key to the $100 trillion AI boom…

And only one company here in the U.S. can mine this obscure metal.

At the high end, shares could deliver a modest triple-digit percentage gain.

A Breakout Moment: Technical Indicators Signal Rally Potential

Technical analysis bolsters the bullish case. After years of range-bound action, Resideo has pierced its former ceiling—an inflection point that often precedes a rally equal to the range's dollar value or, in a bull‐case scenario, the percentage advance from trough to peak.

Both projections point higher, making the setup increasingly attractive for investors.

Activist Investors Influence Resideo's Strategy

The surge in institutional activity is driven primarily by Channel Holdings LP, the investment arm of Clayton, Dubilier & Rice (CD&R), one of America's oldest private equity firms.

After acquiring Snap One, CD&R took a 10% stake in Resideo and is now steering its operations with an eye toward bolstering market share, improving sales performance and enhancing operational efficiency.

Institutional interest extends beyond CD&R, with public and private wealth managers and other fund managers collectively owning about 92% of the float.

On the sell-side, coverage is sparse—only three analysts tracked by InsiderTrades include Resideo in their universe. Yet recent upgrades from Morgan Stanley (to Overweight), Oppenheimer (to Outperform in July) and a June price-target hike from JPMorgan underscore growing confidence.

In mid-September, the consensus forecast implies nearly a 30% gain over current levels, though price-target revisions continue to edge higher, particularly at the top end.

Morgan Stanley analysts highlighted the market's underappreciation of Resideo's indemnification termination. The company paid over $1 billion to exit that agreement, but with future obligations eliminated, it can focus fully on growing the core business.

Resideo resumed growth in 2025 and is expected to sustain it. With consensus estimates still conservative, investors may find further upside as analysts revise forecasts.

Looking ahead, falling interest rates are likely to stimulate housing demand, while advances in digital technology and AI offer additional tailwinds for Resideo's product portfolio.

Key Risks for Resideo Investors: Debt, Short Sellers & Market Timing

Resideo's balance sheet absorbed the one-time indemnification payment to Honeywell but remains solid. The resultant debt increase is manageable, and the company retains ample capitalization. The critical variable is future cash flow, which must support rebuilding reserves, funding operations and gradually reducing leverage.

Short sellers pose a notable risk. As of early September, short interest stood at nearly 4%, up markedly from historical levels and lingering near record highs.

Other uncertainties include the timing of interest-rate cuts and their transmission into housing activity—a lag that could extend into mid-2025 or beyond. Resideo's next earnings report, due in early November, should offer additional clarity on its growth trajectory and capital allocation plans.

This email is a paid sponsorship for Golden Portfolio, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you need help with your subscription, please feel free to email our U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2025 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Suite 620, Sioux Falls, S.D. 57103. United States of America..

0 Response to "[No Brainer Gold Play]: “Show me a better investment.”"

Post a Comment