You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. Charts. Soccer. And the Week in Review...I prepare for Under 8 soccer playoffs by looking at financial charts...

Dear Fellow Traveler: Greetings from the breakfast bar. We’re an hour from the Dolphins’ first-round match today against the mighty… Green team? We lost to them 3-1 earlier in the season, and we enter as the 7 seed. I have chosen my best tracksuit for the game. Last year, Amelia’s team started as the six seed and advanced to the finals, only to lose in overtime. Her team had improved greatly during the year. And then just blew the doors off everyone and made it into the playoffs. We’ll see if we can go on a heater again. Speaking of heaters… the stock market is back at an all-time high after a complete reversal of momentum. The wild swings at the top of the S&P 500 continue. For example—Micron (MU)—our volatile momentum highlight from last week—traded back to the low $190s, only to finish the week near $220… Tomorrow, I’ll send a note to our Capital Wave Report readers with a list of stocks to keep their eye on - and highlight a simple trading strategy to take advantage of any weakness in the top of the S&P 500. Simple strategy - and a new feature of membership to the letter… See what else you get as a member of as well… right here… Now… let’s dig into the weekly Chart Party. Chart No. 1 - Is This REALLY a Gold Rally?This chart from Bank of America shows that the ongoing gold rally is still in its early stages.

Since COVID, we've seen $4.5 trillion flow into cash (money markets), versus $100 billion into gold since 2020. That’s not investors watching from the sidelines. This is actually a ton of investors funding Wall Street’s leveraged bets through money market accounts while thinking they’re being conservative. The real gold buyers were central banks quietly accumulating 1,000+ tons. Retail is still asking their compliance departments for permission to own real money while their “safe” cash gets lent to hedge funds at 4% so they can make 15% in leveraged equity trades. Gold’s pullback this week has everyone asking if they should “finally step in.” Finally? Where the hell have they been? Chart 2: Steal This Chart from ZerohedgeI read that ZeroHedge is the most-stolez source of charts in finance. That’s gotta be true, and it’s not hard to tell if they made the chart… This is CLEARLY a ZeroHedge chart. Plain and purposeful…

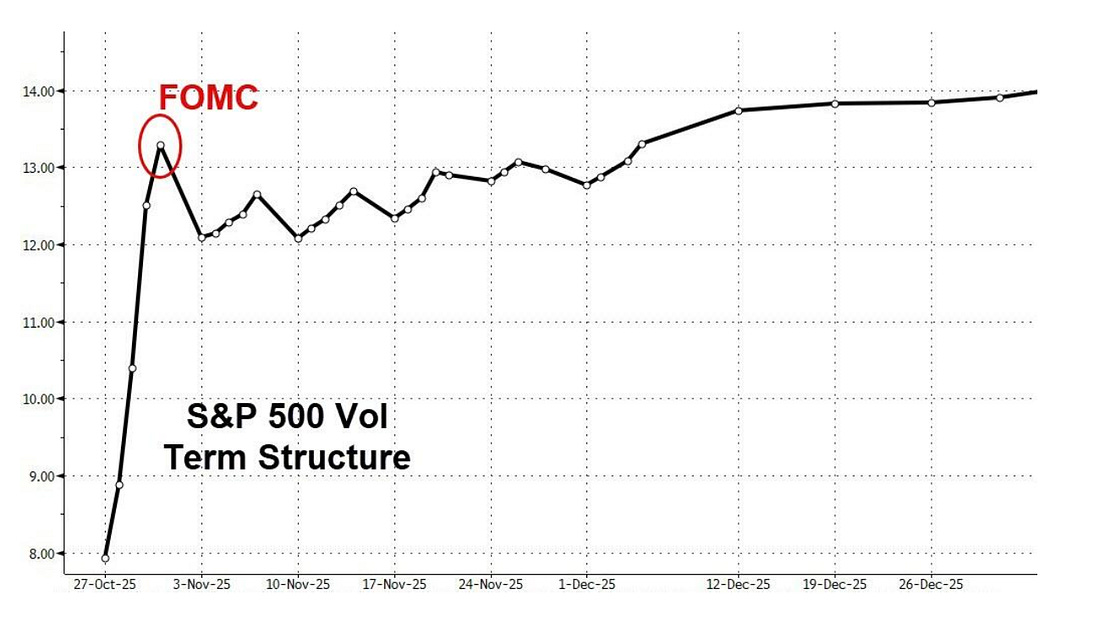

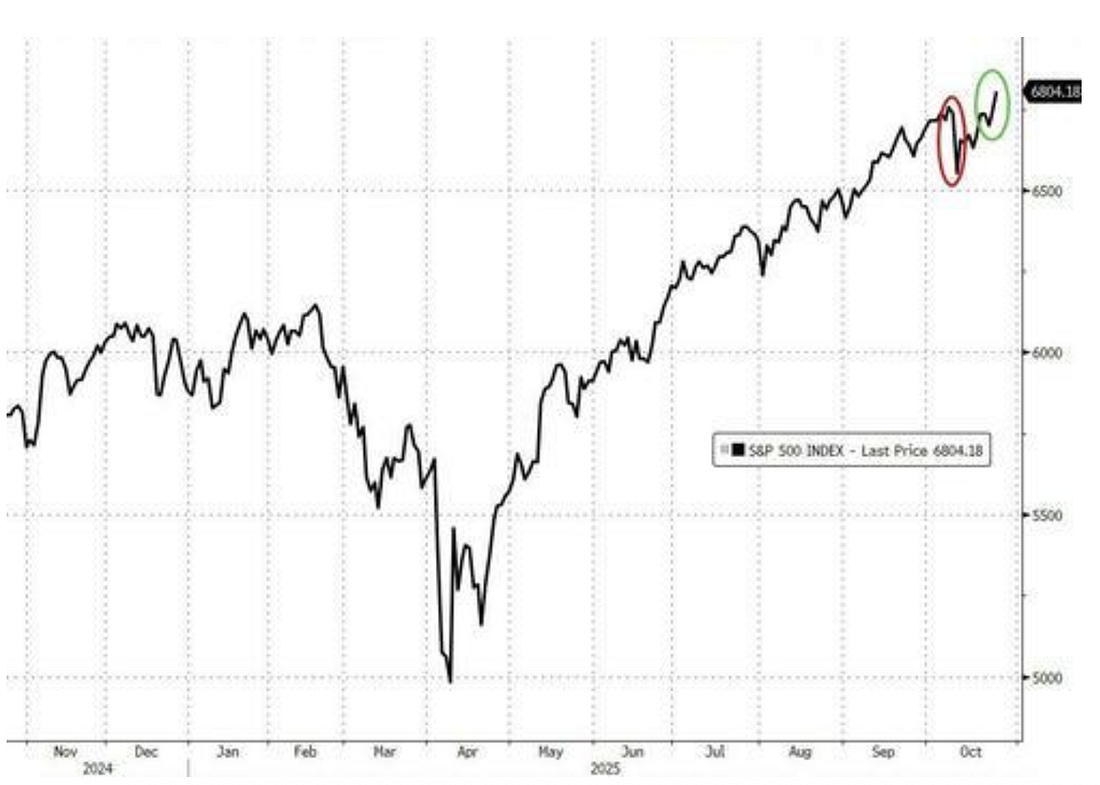

This chart predicts volatility ahead of the upcoming Fed meeting. The reality is that this probably isn’t fear. It’s really the market saying that no one knows what Jerome Powell and the Fed will do. And the people who don’t know what Powell will do… include Jerome Powell. We’ll hear the term “data dependent” - even though we aren’t seeing any data now. That term means they’re making it up as they go. A skeptic would say that this volatility term structure, which has climbed to 14, tells you that professional traders expect chaos around policy decisions because they’ve figured out the Fed’s credibility is shot. Chart 3: More Record HighsWe’ve hit 34 record highs in one year. Some people claim it’s because the U.S. economy is strong… Hold on… I just spit out my water… Remember, all that “cash on the sidelines” is funding leveraged speculation through the repo market. Global liquidity hit an all-time high again last week. Asset prices are divorced from economic reality.

It’s been a straight line up since April… Let’s turn to Michael Howell from Tuesday…

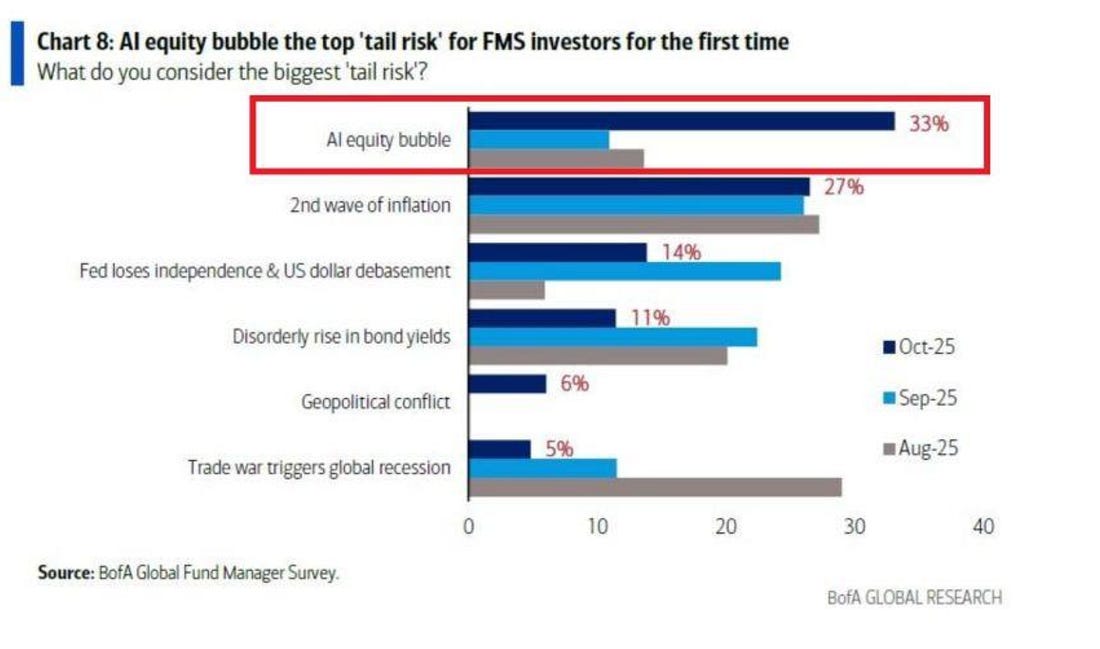

When markets move up in a straight line for months, that’s not investing… We have monetary and fiscal policies on steroids. And people still don’t see it. Chart 4: AI Bubble RecognitionThirty-three percent of fund managers calling AI the biggest tail risk isn’t bearish sentiment - it’s professional liability insurance.

There’s a hive mentality here, one that says, “Don’t blame me - it was a bubble…” The biggest threat to this market is the same as it ever was… A credit freeze and an overwhelming event similar to 2008, 2020, and 2025, where collateral quality goes to hell. Technically, they have this here in “Disorderly rise in bond yields…” But the reality is that AI isn’t the Bubble. America is the Bubble because of the sheer size of the domestic liquidity stock. We’ve gone from 33% of the global MSCI Index to more than 70% in a little more than a decade. That liquidity stock could go away fast. It’s why banks are now suggesting $6,000 gold if there’s just a small reallocation of foreign investment in U.S. equities into the yellow metal. Chart 5: One More Time for the People in the BackPeople keep saying that $7 trillion is sitting in the money markets, waiting to go somewhere… to gold… to bitcoin… to stocks… That money isn’t sitting anywhere. That money is already deployed through the repo market, funding the exact leveraged positions retail thinks they’re avoiding. Your “safe” money market fund is lending to hedge funds at 4% so they can make 15% in the stocks you’re afraid to buy directly.

You’re not conservative, you’re an unwitting wholesale lender to Wall Street’s speculation machine. The “great rotation” has already happened… you just funded it without knowing it. When rates drop, that funding becomes cheaper, and leverage multiplies. You think you’re on the sidelines, but you’re actually the fuel for the fire. Chart 5: The Cure for High Commodity Prices Is…Egg prices have collapsed by 86% since March. This proves supply shocks work both ways. While economists obsess over core inflation excluding everything that matters, food commodities show what happens when actual supply-demand economics override monetary policy. This is what real price discovery looks like when markets aren’t manipulated by central bank intervention.

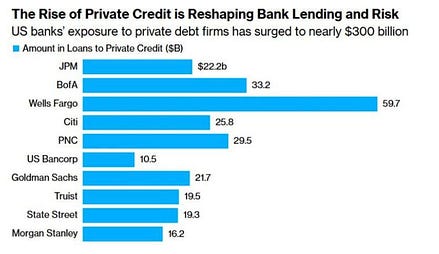

Unfortunately, the Fed can’t print chickens, though they’d probably try if eggs were included in their dual mandate. This collapse shows that when actual economics takes over, prices can move quickly in both directions. This lesson applies to everything. Chart 6: Cockroaches…Remember when guys like Jamie Dimon and Larry Fink complained about Bitcoin, calling it a danger to the financial system? And then they went in and basically took over the entire ecosystem… now controlling it and turning it into a fee-profit machine? Good times. Well… we’ve heard similar gripes about private credit and the dangers in the opaque world of the financial sectors. And yet… banks like JPMorgan are doing all they can to help fuel the private credit world…

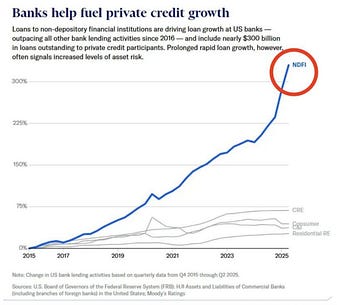

Bank lending to private credit funds has surged 300% since 2015, while everything else stayed flat. Banks are literally funding the shadow banking system they’re publicly worried about. This isn’t innovation. This is regulatory arbitrage with extra steps and higher fees.

Consumer loans, commercial real estate, and residential lending are all flat. The only growth is banks lending to other lenders who then leverage that money 10x into the riskiest credits available. It’s like a financial pyramid scheme where banks provide the base layer while warning about the structure they’re building. The cognitive dissonance is stunning even by banking standards. When your business model depends on funding the thing you publicly worry about, maybe you’re the problem, not the solution. These banks are warning about “cockroaches” while literally feeding them. Chart 7: The Fantasy WorldWhy are stocks at all-time highs? Have we looked at economic conditions and considered that markets are constantly front-running liquidity expectations?

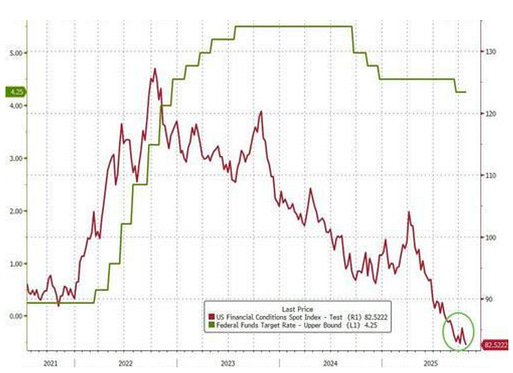

Conditions are at their easiest ever (since tracking while the Fed supposedly fights inflation. This isn’t monetary policy… It’s performance art. It’s the result of what I explained in August. The CENTRAL BANKS AREN’T INDEPENDENT. They have to worry about economic conditions abroad and the interconnectivity of their post-2008 system. I know this is foreign to many people, but it comes directly from the Bank for International Settlements' annual report for April 2025. When credit is easier than during QE infinity, yet officials call policy “restrictive,” we’ve entered Orwell territory where words mean their opposites. The gap between what the Fed says and what financial markets experience is an ocean. They talk tough about fighting inflation while presiding over the loosest financial conditions in history. It’s like claiming to be on a diet while eating cake for every meal. Just a reminder… if you take the Chicago Fed’s National Financial Conditions Index (NFCI) since COVID and flip it over… it basically tracks the performance of the S&P 500 since the COVID crash.

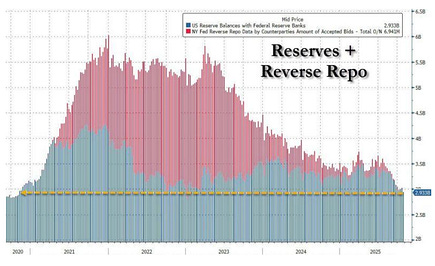

Again… it’s tracking liquidity expectations… Chart 8: Get Ready to BRRRRR…Goldman, JPMorgan, and BofA see QT ending “this month” as a flashing red warning light. Bank reserves below $3 trillion, with reverse repo at zero, signal the Fed’s about to blink again, because they always do when the machine starts breaking.

The reverse repo facility, which acted as a $2.5 trillion liquidity buffer, is empty. With more Treasury settlements on the way and no cushion left, the Fed faces a choice: let the system seize up or pivot back to money printing. They’ll choose money printing because they always do. QT was just an intermission between acts of monetary madness (though the Treasury Department was the star of the half-time show). Chart 9: We Are Building Our Own BankruptciesRemember… We’re not a market. We’re a casino. Not only have the number of ETFs in the U.S. now surpassed the number of U.S. equities… but the number of LEVERAGED ETFs just keeps surging…

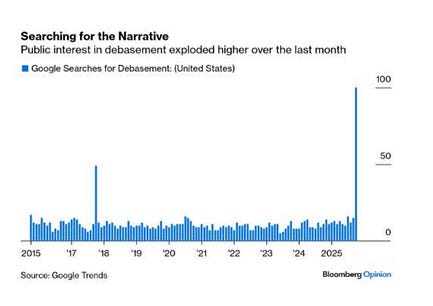

This is what our engineers are doing instead of building bridges. We have hundreds of ETFs with 3x and 5x leverage products filing. We’ve democratized financial destruction. When retail gets institutional-level leverage through their phone apps, we’ve weaponized stupidity at scale. Assets in these products doubled since 2023, reaching record highs. This isn’t innovation. This is socialized gambling disguised as investing. The same retail investors who think money markets are “safe” can now blow up their accounts with 5x leverage on whatever meme stock is trending. What could go wrong when everyone has access to weapons-grade financial destruction through their brokerage app? Oh.. a bunch of money managers get fees… Guys… seriously… what the hell? Finally: Chart 10: Everyone Everywhere Now an Expert on Debasement…A yes… here we go… everyone is now an expert on debasement… All you need is your cell phone… Google searches for “debasement” hitting record highs mean people are finally asking the right questions about money.

When the general public starts using monetary policy vocabulary, it’s either peak awareness or peak desperation. Either way, confidence in the current system is cracking. This search trend shows people are waking up to the fact that their purchasing power is being systematically destroyed by design. The fact that “debasement” is trending on Google tells you more about monetary policy effectiveness than any Fed speech. This week, one of my favorite finance writers penned an article stating that debasement is not the reason the U.S. M2 monetary base is expanding… He argues this because loans create deposits through legitimate economic activity. I argue that the financial system has changed from that banking reality… and that debasement is real - just not in the hyperinflation scenario that many voices share for clicks. Instead, I argue that debasement is far more structural and ongoing—in the shadows where most people don’t see it… And I’ll answer it tomorrow. Stay positive… and Go Dolphins. Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "Charts. Soccer. And the Week in Review..."

Post a Comment