This promotional message is sent on behalf of Base Camp Trading, located at 5540 Centerview Drive, Suite 204, Raleigh, NC 27606

Today's editorial pick for you

3 Stocks with Earnings Growth to Support a High Valuation

Posted On Nov 19, 2025 by Chris Markoch

In a perfect world, we'd only buy stocks with low valuations and above-average earnings growth. But spoiler alert…the market doesn't care about our ideas of perfection. That presents the question of what to do with stocks with a lot to like except for that pesky valuation thing.

Table of Contents

As with most things in the market, the answer depends on the stock. The market is slumping because investors are concerned about the lofty valuations in many stocks, particularly those having to do with artificial intelligence (AI).

Is it time to move away from growth stocks? That seems extreme. Look, your portfolio needs growth. And the good news is that you can find growth without investing in AI stocks. There are companies that deliver strong revenue growth backed by equally strong earnings growth.

In this article, we're looking at three companies that command premium valuations. However, the key difference is that their fundamentals are catching up. Strong unit economics, expanding operating margins, and disciplined cost management are giving investors renewed confidence that these high-multiple stocks can grow into and potentially exceed their current market prices.

Shopify: Earnings Growth from High-Margin Commerce Infrastructure

Shopify Inc. (NYSE: SHOP) is transitioning from a hyper-growth e-commerce platform into a more mature, highly profitable infrastructure business for online merchants. The company has streamlined operations after divesting its logistics unit and is now focused on high-margin software and payments revenue.

The company's merchant solutions, particularly Shopify Payments and Shop Pay, continue to grow rapidly as merchants consolidate more of their digital operations onto the platform. Operating leverage is improving, and recurring subscription revenue provides stability even in uneven retail environments.

As of this writing, SHOP stock had a forward price-to-earnings (P/E) ratio of 126x. That's a premium to the S&P 500, certainly, but it's also a premium to its historic average.

However, analysts are forecasting earnings growth of over 30% in the next 12 months. With e-commerce penetration still far from saturated globally, Shopify has a long runway to grow earnings well above current estimates, supporting its elevated valuation.

Where the Thesis Could Be Wrong

A slowdown in consumer spending would weaken e-commerce trends. That could pressure merchant volumes and limit Shopify's operating leverage. Additionally, Shopify faces competition from Amazon.com Inc. (NASDAQ: AMZN) as well as niche e-commerce platforms that could make it harder for the company to maintain its current pace of margin expansion.

DoorDash: Scaling Earnings Growth Through a Broader Delivery Ecosystem

DoorDash Inc. (NASDAQ: DASH) has evolved far beyond a food-delivery app into a broad-based last-mile logistics platform. Its expanding marketplace now includes groceries, retail, convenience, and even small business delivery, capturing a larger share of consumer spending.

The company continues to deliver strong order growth while simultaneously improving contribution profit per order. This is clear evidence that its unit economics are stabilizing.

DASH stock has a forward P/E ratio of around 96x. However, analysts project 69% earnings growth in the next 12 months. If that's the case, the source of that growth may come outside the United States. DoorDash's international expansion is underappreciated by the market and could become a major long-term source of earnings growth.

Where the Thesis Could Be Wrong

DoorDash's path to profitability depends on maintaining order volume growth and disciplined spending. Increased competitive pressure, regulatory shifts around gig-worker classification, or slowing consumer demand in key markets could delay margin improvements and challenge the valuation.

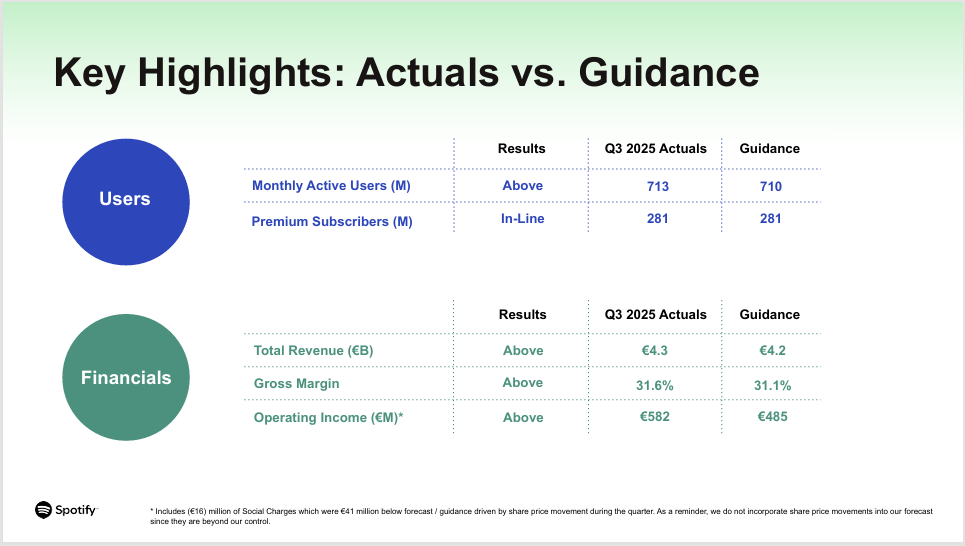

Spotify: Earnings Growth Powered by Pricing and New Content Streams

Spotify Technology (NYSE: SPOT)has entered a new phase where revenue growth and profitability are moving in tandem. The company's shift toward marketplace tools, price increases, and higher-margin podcast and audiobook offerings is driving improved gross margins.

Spotify's scale advantage, over half a billion users globally, gives it tremendous data and pricing power. Its expanding suite of creator tools deepens engagement and encourages more monetization across both music and non-music audio as operating expenses grow more slowly than revenue.

Spotify has a forward P/E ratio of around 62x. However, the company is solidly profitable, and the bottom line is expected to grow around 30% in the next 12 months. With management targeting sustained margin improvements, SPOT's valuation looks justified and potentially conservative if execution continues.

Where the Thesis Could Be Wrong

If licensing costs rise faster than expected or user growth slows, Spotify's margin expansion could stall. Competitive pressure from Apple Inc. (NASDAQ: AAPL), Amazon, or emerging global platforms could also limit SPOT's ability to push through future price increases.

Conclusion

Even in a market increasingly focused on valuation risks, some high-multiple growth stocks still offer compelling upside because their projected earnings growth supports further expansion.

Shopify, DoorDash, and Spotify have each reached key profitability milestones while strengthening their long-term competitive positions. For investors willing to look beyond the usual suspects, these three names offer a more durable path to growth.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

0 Response to "Trade this between 9:30 and 10:45 am EST 🕒"

Post a Comment