You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. Money Printer 204: The Liquidity MismatchFun with the financial crisis that no one is taking seriously...

Dear Fellow Traveler, If we go back to Money Printer 101… we discussed “liquidity.” There are two different definitions of this term, and confusing them is how people get wiped out. I’m usually not talking about the textbook definition… I’m always talking about the Permission definition, which underlies something called “funding liquidity.” That’s the ability to take an asset and borrow money by using it as collateral. Today, we want to talk about the textbook definition of liquidity… The Investopedia one that explains, “The ease and speed with which an asset can be converted into cash without materially affecting its price.” Textbook liquidity or “Market liquidity” is what separates the feeling of “I own this” from “I can sell it and get my money back…” Sometimes, what happens is that someone’s short-term liabilities (like a bank’s depositor withdrawals or a fund’s redemptions) are drawn upon faster than its assets can be converted to cash to meet those demands. This is usually caused by a bank or a fund holding illiquid long-term investments - things like underwater bonds or assets like houses or businesses that can’t just be sold right away without incurring some financial damage. This is known as a “liquidity mismatch.” It has nothing to do with whether the asset is ‘good’ or ‘bad.’ It’s about timing. And this concept has destroyed more funds, banks, and portfolios than fraud ever could. A liquidity mismatch doesn’t need a criminal. It just needs someone to be optimistic about something at the wrong time, or to be overexposed to an asset they can’t sell, or would take serious losses to try to meet their short-term obligations. And if you need a simple equation to explain this… it’s simple… Overconfidence + Capital or Bank Runs = Volatility and Chaos. What’s a Liquidity MismatchI’ll bet this sentence is the first time you’ve thought about your bank savings account today. This subtle reminder doesn’t affect you much, because you know it’s there. You could withdraw the money from your account tomorrow, cover an unexpected cost, or even walk away from a bad job if you have enough money. (That’s the feeling of funding liquidity or “permission” to borrow and spend, as I’ve explained.) It’s there when you need it. That availability is what makes YOU liquid…

Liquidity gives you permission to operate. That money can quickly be converted into a purchase or the repayment of a debt. You could do this in the next 10 minutes… Now, consider owning a rental property. If your tenant stops paying, you might have the cash to cover the associated mortgage. But if they stop paying for a few months or declare “Squatter’s Rights,” as in California, you now have an issue. That property might be worth $400,000 on paper. But you can’t convert it into cash by Friday, regardless of how badly you need that money. That’s “market liquidity…” To convert it into cash, you need to list it, find a buyer, negotiate a price, and go through the absolute joy that is the closing process. That process could take weeks or months, depending on the market, buyers, and, of course, the inspections. The value of the house is very real. But its “illiquid” nature means you won’t capture that value until someone shows up with a check. That’s where this mismatch can occur. Let’s say you have $10,000 in savings… but you suddenly owe $50,000 because you bet against U.S. hockey in the Olympics. The only way you can get that money is to sell that house… which means you’re highly illiquid at the moment, and your creditor is now not going to receive their money. And if they owe someone else money… that creates a ripple effect across a capital chain. Well, let’s move from sports gambling to something more vulgar… Private credit. Private credit doesn’t usually fail because loans default. It fails when investors ask for their money back at the same time. That distinction matters because low default rates don’t protect you from illiquidity. In finance, a liquidity mismatch occurs when an investment fund takes your liquid money (the savings fund that represents freedom) and uses it to buy many illiquid assets. They’ll purchase properties, private loans for companies, stakes in businesses that don’t trade publicly, and assets whose “value” is whatever the spreadsheet says it is. The fund will tell you that you may politely request a refund every quarter through a “redemption window.” It’s very formal. You can’t just call the manager, start dropping F-bombs, and tell them “I want my money back…” In periods of ample credit and market liquidity, most investors aren’t going to ask for their money back because they’re aware that private equity and other alternative strategies typically have a multi-year timeline. More importantly, investors usually aren’t all scrambling to get their money back at the same time - something we compared previously to a run on a traditional bank. The investment fund should maintain a small cash reserve to accommodate occasional redemption requests, and everyone will remain happy. But we have to think about group happiness on a bell curve. Sometimes, like 2008 or 2020, a lot of people get nervous at the same time. They’ll all line up at the quarterly redemption window like they’re trying to buy concert tickets to a once-in-a-lifetime event… Think the Rolling Stones have another Farewell Tour, but this one’s for real this time. You have all those people line up… hours… days… however long it takes, and they come to realize that their money isn’t there. In fact, it never really was there. It was gone the moment the fund started buying illiquid assets. The “quarterly redemption” was just a fairy tale that they hoped no one would use, and they just hoped no one would notice. Well… that’s exactly what’s happening in the private credit markets right now. Say Hello to Blue Owl CapitalDoug Ostrover helped build Blackstone’s credit business… Marc Lipschultz had more than 20 years at KKR. And Craig Packer worked at Goldman Sachs, because it’s always important for one of your founders to have worked at Goldman Sachs… so someone can brag about the résumé. The three of them launched Blue Owl Capital. These men helped build the modern machine that runs private credit. By the end of 2025, they managed more than $300 billion across their platform. Blue Owl ran an unlisted BDC (business development company), OBDC II, that offered periodic liquidity while holding long-dated private loans.

This wasn’t sold to pension funds or sovereign wealth funds. It was sold to people who were all amped up about the “democratization” of private credit for ordinary investors… Of course! They sold it to people who might be dentists, your neighbor’s financial advisor, and people who were promised quarterly liquidity on assets that don’t trade quarterly. I need you to read that last sentence again… because that’s my entire article. And… why bars are open on Monday. What HappenedOver the first nine months of 2025, OBDC II investors demanded about $150 million in withdrawal requests. That was roughly mid-teens as a percentage of the fund’s net asset value (NAV). That’s a lot of people getting into line at that ticket window all at once. Blue Owl tried to change course to prevent a liquidity mismatch... They first tried to merge the OBDC II funds into their publicly traded fund, OBDC. The problem was that the public fund was trading at… about a 20% discount to its stated NAV. That merger would have immediately vaporized about 20% of every retail investor’s position in that fund. Advisors who had worked with their investors… they went insane over this. So, Blue Owl eliminated that deal and told everyone it was “in the best interests of shareholders.” (Translation: everyone screamed, and they panicked.) Then, last week, Blue Owl did that thing that everyone was afraid of… but no one really thought they’d ever do… They ended quarterly redemptions for OBDC II. And then issued this statement… “Contrary to what has been reported, we're not halting redemptions, we are simply changing the method by which we're providing redemptions," Craig Packer said in a conference call. Oh that makes it better… I suppose. This was not a collapse of the loans themselves. It was a collapse of the promise of liquidity layered on top of them. Oh bother…

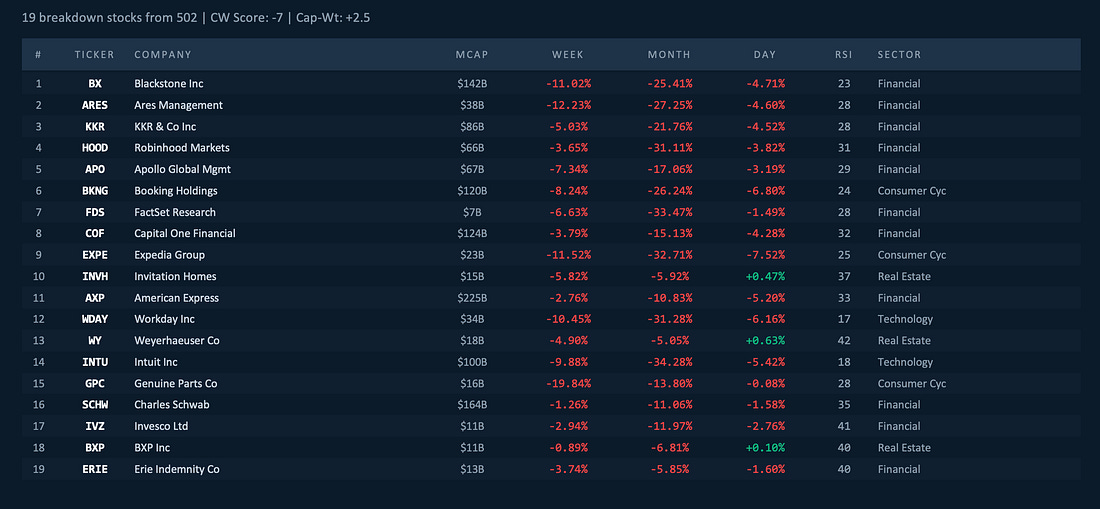

That exit door for redemption was always supposed to be there… Well… it vaporized too. They sold $1.4 billion in loans to institutional buyers at roughly par, which tells you the assets weren’t ‘toxic’… just illiquid. Then they planned to return about 30% of investor capital by March, but the other 70% stays locked inside the fund for... well, nobody knows exactly how long. They called this “accelerating the return of capital…” That’s a wild phrase when you think about it, because what they actually did was lock people’s money in a building with no exit and put a positive spin on the padlock. Blue Owl’s stock cratered 10% intraday on the news. Private equity/alternative asset managers like Ares, Blackstone, and Apollo all fell by more than 5% in sympathy… and they’ve been on our Capital Wave negative momentum list for the better part of a week… with another brutal day on Monday.

Every manager running a similar structure knew it could be them next… and the market is dumping these players left and right. Blue Owl’s problem caused a sizeable market-cap wipeout across the entire alternative asset industry. Fear is always bigger than the fund itself. Yahoo! also dropped this gem in the same report on Blue Owl.

BitMex CEO Arthur Hayes has already called for the Fed to start warming up the Money Printer. It certainly feels like we’re going to feel its glow in the next 12 to 18 months…

The Cantillon Effect... AgainRemember the Cantillon Effect from Money Printer 105? The people closest to the money creation always benefit first and suffer last, and the people farthest from the money suffer first and benefit last. There is a similar order to things when it comes to people getting out of investments. Did you ever stand in line all night for concert tickets? And then five minutes before the ticket window opened, a bunch of people would “join their friends” and claim someone was saving their spot the whole time? Yeah… that’s basically modern finance too. It’s just a guy screaming back to you… “But I’m with Goldman Sachs...” And you scream… “No, I was here first!” And they just say, “No, it’s fine. It’s fine. Shut up.” And you know how that goes…

So, people have to look for alternatives to get out, and that’s usually not good… Funds associated with Boaz Weinstein’s Saba Capital began offering to buy OBDC II stakes from trapped investors at a 20% to 35% discount to their stated value. That means the people who redeemed early got roughly $1.00 on the dollar while the people trying to sell now are looking at $0.65 to $0.80... Even though the underlying assets and the fund itself haven’t changed at all. The only thing that changed was how far some were from the exit when the music stopped. And while investors sit and wait for the wind-down, Blue Owl is likely still collecting management and incentive fees on the fund. Brian Moriarty, principal of fixed-income strategies at Morningstar, has said Blue Owl should reconsider those fees in light of the situation. He’s right, but I’m not holding my breath. The people who run the machine get paid first, always, and regardless. That hasn’t changed in 450 years of modern finance. Why This Matters to YouPrivate credit has been all the rage over the last few years… reaching $1.8 trillion, according to Bloomberg; $2.3 trillion, according to Preqin, and even more depending the models and type of whiskey you’re using…

Those asset totals look orderly. The flows underneath them do not. Wall Street banks loved private credit’s surge because they didn’t have to put any of it on their books. That gave them large origination fees and regulatory protection. Annual flows into semi-liquid private credit funds went from $10 billion in 2020 to $74 billion in 2025, according to MSCI. And the U.S. government has been helping it along, as the SEC lifted illiquid asset caps for registered funds and regulatory changes and policy proposals are actively working to expand private credit exposure inside retirement channels, including 401(k)-linked vehicles. Just a reminder… they want to put your retirement money into the same structures that just blew up at Blue Owl. They call this the “democratization of private equity.” Stanford professor Amit Seru calls it a “systemic risk machine.” I’ll let you decide who is more credible… The people trying to sell it… or the people who actively study their structure and have a deep understanding of financial history, mania, and panics. What To Do Right NowHere’s what you can actually do with this information. If, by chance, you own any “semi-liquid” or “interval” fund... any fund that offers quarterly or monthly redemptions on private assets... Go read the fund documents tonight. Look for the section on redemption limits. They’re sometimes called “gates.” Every one of these funds has a clause buried in its documents that allows the manager to suspend redemptions when too many people request money at once. When evaluating these products, focus on the liquidity of the underlying assets, not the wrapper's liquidity. If a fund holds private loans that take months to sell, the fact that it offers “quarterly liquidity” is marketing… I will remind you of something Tim Melvin and I discussed at a Thanksgiving dinner about 13 years ago… I’m not sure - thanks to the bartender - which person said it. But it goes like this… Yield is not compensation for liquidity risk. It’s often bait for it. That wrapper doesn’t change the asset. Wrapping a brick in gift paper doesn’t make it a present. It makes it a weapon… Then, understand where you sit in the redemption line. If you’re a retail investor in these products, you’re at the back, because the institutions, insiders, and early redeemers always get out before you... I’m not being cynical. That’s just the structure. The question is whether the yield you’re being paid is worth the risk of being last in line when the door closes. If you’re not sure about any of this... That’s the most important signal. The people selling you these products are very sure, and they’re getting paid whether you make money or not. Okay… that’s all for now…

Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

: r/bourbon")

Subscribe to:

Post Comments (Atom)

0 Response to "Money Printer 204: The Liquidity Mismatch"

Post a Comment