Ticker Reports for March 27th

5 April Buys With Double-Digit Year-End Targets

2026 stock price action faces headwinds but remains on track for S&P 500 stocks and others to move higher by year’s end. While headwinds persist, so too do bullish fundamentals centered in labor markets, consumer demand, and business spending. The bulk of business spending is on tech, specifically data centers and AI, but extends to other industries and segments. The stocks on this list have numerous things in common, including positions in tech, improving outlooks, and potential to reach high double-digit gains by year’s end.

NVIDIA: Too Cheap to Ignore

There are many reasons to buy NVIDIA (NASDAQ: NVDA) stock in April, but the one summing it all up is the deep-value opportunity. Value is present in the price-to-earnings multiple and analyst trends, which together suggest a high-double-digit upside is the minimum to expect. Trading near 21X projected fiscal year 2027 earnings, the stock is nearly 50% off relative to where blue-chip tech stocks tend to trade, and its own long-term trends—and the forward outlook is robust. Long-term forecasts, which have so far proven too low, suggest NVDA stock trades at only 6X the 2035 forecast, implying 400% to 600% upside over the next five to ten years.

NVIDIA catalyst include its upcoming earnings release, which will affirm the trends and potentially accelerate them. There is competition, but NVIDIA’s first-mover advantage is unprecedented, and it has the funds to capitalize on it. Investors should expect to hear more about acquisitions and investments in the coming months. Until then, 53 analysts rate the stock a Buy, with a 96% Buy-side bias and a consensus forecast for 50% upside.

Advanced Micro Devices: Expensive Today, Super Cheap Versus Tomorrow

Advanced Micro Devices (NASDAQ: AMD) trades at a premium relative to current-year earnings, but current-year earnings don’t matter for this stock. The company is at a critical pivot point, on the cusp of launching rack-scale solutions for hyperscale AI datacenters and unleashing a torrent of demand. Its MI450 solutions provide superior performance for some tasks, including inference, and offer a lower cost of ownership, making them a viable choice when available. As it is, the analysts forecast revenue and earnings acceleration, but far below the potential. Based on demand trends, AMD’s revenue growth could reach triple digits within the first few quarters of the MI450 launch.

Analyst trends are only slightly less bullish for this stock than for NVIDIA. The consensus of the 40 tracked by MarketBeat is a Moderate Buy; coverage is increasing, sentiment is firming, and the Buy-side bias is 75%. The consensus price target offers around 30% upside, and the high-end range, where the trend leads, doubles it.

Nebius Group: Building Capacity as Fast as Possible

Nebious Group (NASDAQ: NBIS) faces headwinds, including a swelling debt load, but its growing backlog, driven by deals with Meta and Microsoft, offsets them. The likely scenario is that this data center business, which has close ties to NVIDIA, continues to execute its strategy and capture its backlog. As it stands, the backlog is nearly $50 billion, with revenue recognition expected to accelerate significantly in the subsequent fiscal year as new projects come online.

Only 13 analysts cover NBIS stock, but the trends are robust. Coverage is up more than 100% on a trailing 12-month (TTM) basis, and sentiment is firming, with 11 ratings pegged at Buy. Up nearly 200% TTM, the consensus price target forecasts more than 30% upside and recent targets align with the high-end, another 20% higher.

Amprius Technologies: Winners Keep on Winning

Amprius Technologies (NYSE: AMPX) is a textbook bull market driven by an emergent technology, validation through contract wins, ramping capacity, rising demand, and results and guidance. The likely outcome is that this story continues to advance boldly, with expanding revenue, margins, and profitability.

The technical action says it all: the Q4 2025 earnings release triggered a buying event that lasted four weeks, pushing price action to long-term highs and keeping it there. The rally turned to consolidation, the consolidation smacks of continuation, and even higher prices are likely.

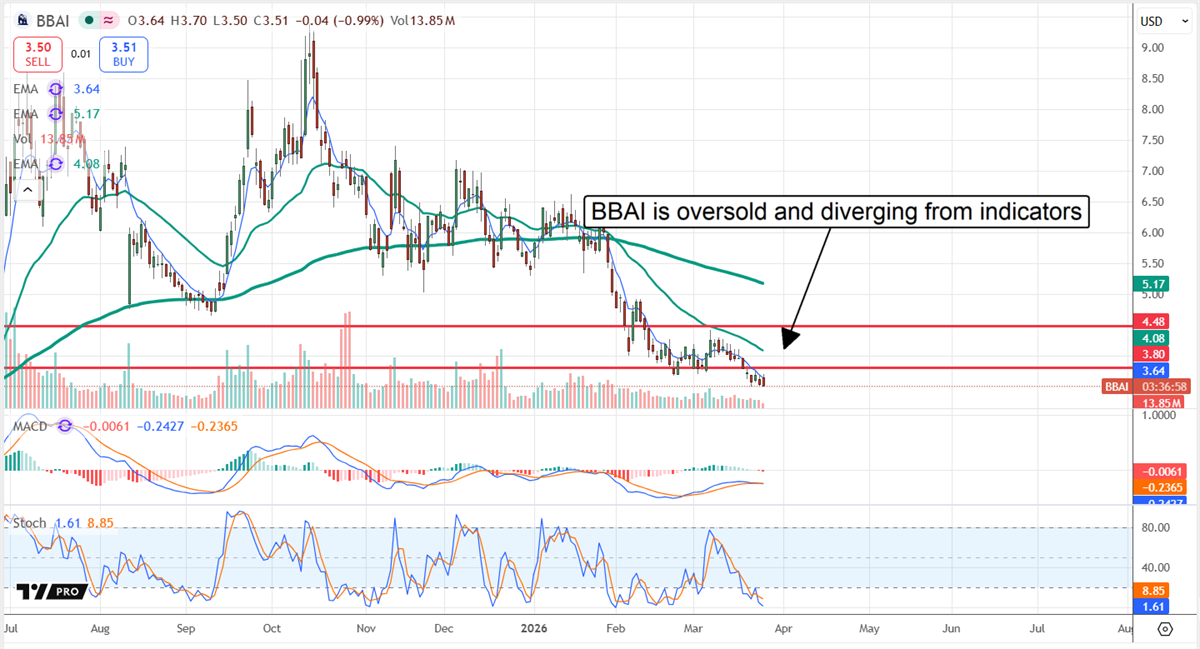

BigBear AI: Sell-Off Exhausted, Rebound in the Works

BigBear AI (NYSE: BBAI) isn’t out of the weeds yet, but its fiscal 2025 report revealed its aggressive repositioning is over. The dilutive capital raising is over, the company’s balance sheet is healthy, new acquisitions position it for growth, and business is improving. The likely outcome is that momentum accelerates in upcoming releases, triggering short-covering and a complete reversal in the stock price action.

At 27% short, the market is ripe for reversal. Analyst coverage is tepid but forecasts a greater than 50% upside; institutional activity is more pronounced, with them actively accumulating in Q1 2026.

Ticker Revealed: Pre-IPO Access to "Next Elon Musk" Company

Ticker Revealed: Pre-IPO Access to "Next Elon Musk" Company

Ondas Inc. Flywheel Gains Momentum, Vertical Liftoff Imminent

Ondas Inc.’s (NASDAQ: ONDS) price action following its fiscal 2025 earnings release suggests its stock price may drift sideways or even lower in the near to mid-term. However, as tepid the price response was, the results were robust, pointing to accelerating business and a timeline to profits, causing analysts to cheer. It is the analyst response to focus on in Q2 2026, as they are bullish on this stock, have increased their coverage, and are driving the forecasts higher.

MarketBeat tracked a handful of revisions immediately before and after the release, including numerous price target increases and affirmations that extended the trend. Targets from Needham & Company, H.C. Wainwright, and Lake Street Capital put ONDS stock in the $19 to $23 range, above the consensus at the low end, with consensus price target forecasting more than 60% upside. A move to $23, the high target as of late March, is more than 125% upside and potentially a low target, given the improving outlook.

Ondas Holdings Accelerates in Q4: Guides for Acceleration in FY2026

Ondas Holdings had a robust quarter in Q4 2025, driven by new clients and increasing orders for its drone, counter-drone, unmanned, and surveillance systems. Revenue grew by 629% to just over $30 million, accelerating sequentially by nearly 5,000 basis points as the company transitions to its operating phase. The only bad news was an increase in operating expenses, which widened losses. However, the increased expenses were tied to growth and acquisition activity, not core operations, and are expected to produce accretive results in fiscal year 2026 (FY2026).

Guidance is a reason to be bullish on this stock. Not only is the forecast robust, expecting $39 million in Q1 revenue and at least $375 million for the year, but it also expects sequential acceleration in Q1, year-over-year acceleration, and significantly outpaces the consensus estimate. Consensus for Q1 is approximately 5,000 bps or 50% shy of company expectations, and there is a chance the company was cautious in its forecasts.

The Mistral merger and follow-on acquisitions and partnerships expanded the company’s access to government contracts and capacity to fill them. The result is a swelling backlog, up 240% sequentially in Q4 to $68.3 million, worth nearly double the Q1 forecast and pointing to continuing strength this year.

Ondas Strengthens Balance Sheet: Dilutive Headwinds Abate in 2026

Among the headwinds for Ondas' stock price in late 2025 and early 2026 was the need for capital. Capital-raising activities resulted in approximately 200% shareholder dilution and significant warrant liability on the balance sheet, but it is over for now. Ondas is now well-capitalized, has a multi-year operating runway, and is unlikely to need additional capital except in the event of an acquisition.

Even so, the approximately $1.5 billion in cash and equivalents raised is sufficient to drive growth, including acquisitions, in the near term, leaving the market free and clear to advance absent other bearish forces.

Short interest is a concern, but it presents as much opportunity as risk. At nearly 35%, short interest effectively caps the market in early 2026 but may not keep it down for much longer. The FY2026 guidance and the potential to outperform it may catalyze short covering and underpin a price rebound. Institutional activity aligns with this outlook, as institutions own more than 35% of the stock, are accumulating aggressively, and ramped activity to record highs in Q1 2026.

Ondas catalysts include ongoing M&A activity, including the planned acquisition of World View Enterprise, as well as the expansion of the robot-as-a-service business. World View Enterprise is a high-altitude balloon-based surveillance platform providing services to the government and industries. It completes Ondas' surveillance-integration capability, providing high-altitude support for the lower-altitude and ground-based components. Additionally, the partnership with Palantir (NASDAQ: PLTR) is driving business. The collaboration integrates critical Palantir AI technology into Ondas drones and robots, enabling a scalable mission-critical capability.

Ondas Is Trending Higher: Winding Up in March for a 2026 Rally

Tepid as Ondas’ post-release price action was, it isn’t all that bearish, despite falling by 3.4% the day of the release.

Price action is winding up within a range aligning with its uptrend, setting up for another run higher. Short-sellers continue to influence the action, but long-term buy-and-hold activity offsets it. Volatility is likely to continue, with subsequent peaks and troughs extending the bullish trend.

Have $500? Invest in Elon's AI Masterplan

Have $500? Invest in Elon's AI Masterplan

KB Home's Earnings Slump Puts Dividends and Buybacks at Risk

KB Home (NYSE: KBH) is a high-quality stock that can return significant capital to its investors. However, a combination of factors suggests that Q2 2026 isn’t the best time to buy this construction stock; rather, it's best to watch it and see what happens. What is expected is continued revenue and earnings contraction, though contraction could cease by year’s end.

KB Homes may be near its price bottom as March comes to an end; however, there is a significant chance of Q2 weakness and the stock price moving even lower.

The critical support level is near the 2025 lows at $48.90. This level has been supporting the market since Q2 2025 and is in jeopardy of collapsing. The stochastic and MACD indicators reflect weakened market conditions and susceptibility to decline, while the cluster of exponential moving averages is on the verge of a Death Cross.

The Death Cross is the opposite of a Golden Crossover, occurring when short-term EMAs cross under a longer-term EMA, signalling a bearish shift in market dynamics. The Death Cross often precedes major market sell-offs and could send this stock to the low end of its long-term range near $25.

Weak Results Signal Risk for KBH Capital Returns

KB Home struggled in fiscal Q1 2026, with revenue of $1.07 billion down approximately 23% year over year (YOY). Weakness was seen not only in the decline, but also in the underperformance, which topped 180 basis points (bps). The decline is caused by a 14% reduction in deliveries and lower prices, with forward-looking metrics indicating the weakness will continue. The company’s backlog is down by double digits in value and home count.

Margin news was also poor. The company experienced margin pressure at all levels, with costs rising and revenue deleveraging. The net impact was 52 cents in GAAP earnings, 2 cents shy of MarketBeat’s reported consensus, down approximately 65% YOY and compounded by weakened guidance.

Guidance was as poor as the Q1 results, with the company forecasting a nearly 24% contraction, accelerating its decline sequentially, and falling short of the consensus estimate. The only good news is that the margin is expected to hold steady, but even that isn’t that great. The critical takeaway is that margin compression and sales declines cut deeply into earnings power, leaving capital returns in jeopardy.

The capital return is significant as it underpins the stock price action. Returns include a dividend and share buybacks, which reduced the Q1 count by an average of 12.7% YOY. The problem is that cash flow is insufficient to cover the payments, leaving the company to lean on its cash pile. The cash pile is sufficient to sustain returns but not indefinitely, and the buybacks are already slowing. The Q1 pace is down 75% YOY, and the Q2 forecasts suggest the same for the current quarter. Looking forward, the pace of buybacks may slow to nil before the company reverts to growth and has the capacity to resume.

Analysts, Institutions, and Short-Sellers Present Headwinds for Investors

Analysts, institutions, and short-sellers, the three groups that investors need on their side, are not bullish on this stock. The analyst coverage remains firm, but the consensus rating has slipped to Hold, and the price targets are falling.

The existing low target of $25 suggests a price floor is in place, but it’s not firm. All it will take is another string of downgrades or price target reductions to send this market through the floor to lower lows, and there doesn’t appear to be anyone willing to buy.

Institutions, which own about 97% of this stock, have sold on a trailing 12-month basis and ramped their activity in Q1, capping gains and sending the market to long-term lows. There is no incentive for them to accumulate in the Q1 results or guidance update. Meanwhile, short interest is off its highs but remains elevated near 10%. It represents an overhang that may strengthen, given the weakened outlook and potential for underperformance. In this scenario, the KBH market is distributing shares and is likely to continue doing so.

The catalyst for higher prices is the built-to-order strategy. The company is working to reduce dependence on walk-in sales and build mostly as needed. The move is amplifying near-term weakness, but sets the company to return to growth in 2027 with stronger margins.

Elon Musk already made me a "wealthy man"

Elon Musk already made me a "wealthy man"

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

0 Response to "🌟 5 April Buys With Double-Digit Year-End Targets"

Post a Comment