End of The Quarter: What If I'm Wrong?We conclude this quarter's Postcards Theme with an important note about these markets.Editor’s Note: As you know, our momentum signal is deeply negative.

I’ve explained in recent weeks all of the problems linked to private credit, banking reserves, valuation compression, and more. So, I don’t have a real investment recommendation for you this week that I find to be something long-term and linked to the traditional chokepoints. If anything, I would recommend that you buy Archer Daniels Midland (ADM) as a momentum play and then set your trailing stop right back at the stop’s 20-day exponential moving average.

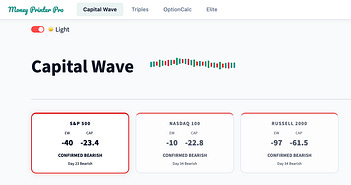

Our momentum names right now are HEAVY in agriculture, upstream oil and gas, refineries, and fertilizers, what I laid out in the Iran presentation on March 8. Meanwhile, the extraction names in Visa (V) and Mastercard (MA) are ranked the worst momentum stocks in our model. What does this mean? When the Federal Reserve or the Bank of Japan or the Treasury comes up with new policies that accomodate this economy… they will be screaming buys. Until then. Now then…

To Whom It May Concern (You): For 17 weeks, I sat down and wrote you a letter about how the system works... the extraction, the waterfall, the containers, the debasement, the collateral chains, the political constraints that guarantee the printing never really stops. I believe and hold convication behind every word I wrote. But… I owe you something I haven’t given you yet. I owe you the other side. I’m going to wrap up this quarter on this topic before the pivot comes. I felt that it makes sense to bring this all to a conclusion… I don’t owe a retraction or a hedge dressed up as humility, so I can claim credit regardless of how things unfold. I owe you an honest accounting of what would have to be true for the thesis to break... It bothered me for a week that I never really talked about these things… I want to talk about what would need to happen for the framework I’ve built across this entire series to be wrong in a way that matters. Because if I can’t name the failure conditions of my own argument, then what I’ve written isn’t analysis… It’d be religion. Religion doesn’t protect your portfolio. Our current portfolio is flat for the quarter now… but recall that I recommended a few weeks ago to be on the fence. This is not a time to start buying for the sake of buying… but this portfolio has to exist in the face of pressure… This portfolio was great before the momentum signal turned negative… We were up 12% on the year for March 2… our signal turned negative, however, the previous month, and we saw severy monetary policy worries kick in on March 3. The Ways They TakeThe core thesis of this series is simple… The global financial system is built on debt that must be continuously refinanced, collateralized by assets that must hold their value, and governed by a political system that can’t tolerate deflation. That’s it… Those three constraints leave only one available path... occasional liquidity expansion. Each round of expansion hinders the currency, inflates the containers that absorb it, and extracts purchasing power from anyone who doesn’t understand how to hedge against it... That’s the argument. I laid it out across 17 volumes... from the Debasement Index in Volume 11, to the regulatory theater of Volume 15, to the healthcare extraction in Volume 16, to the collateral crisis unfolding in Volume 17. For it to be wrong, at least one of those three constraints would have to break in a direction I haven’t considered. The first way I could be wrong is if the debt burden becomes manageable without expansion. This would require either sustained economic growth well above the rate of debt growth… or a political consensus around fiscal consolidation that holds for years, not quarters. It’s happened before... America ran surpluses in the late 1990s, and the debt-to-GDP ratio declined meaningfully through the second half of the decade. But… And I stress… BUT. The conditions that made that possible were very different… The Cold War had just ended, releasing a massive “peace dividend.” An internet revolution drove productivity gains that showed up directly in tax receipts. And… perhaps most importantly on the divide we live in today… the baby boom generation experienced their peak earning years, generating contributions to Social Security and Medicare that exceeded withdrawals. None of those conditions exist today. Zero. The defense budget is rising. The technology revolution of 2025 is producing efficiency gains that divert primarily to capital owners rather than wage earners… That matters, because the end results compresses the tax base rather than expanding it. Oh, and the demographic structure is inverted... the dependency ratio is climbing, not falling. The annual debasement rate I discussed in Volume 11 hasn’t slowed. If anything, the compounding has accelerated since 2020. I’d need to be wrong about all of that at the same times…. for the debt constraint to ease on its own. I don’t think I am... What’s Beneath the NoiseSo, what’s the second way I could be wrong? A simple question. What if the collateral system evolves in a way that makes it more resilient? A large share of global lending is collateral-backed, the collateral multiplier is fragile, and when bond volatility rises, the whole chain tightens at once. That’s not my point... It’s from the World Bank, via Michael Howell. It’s confirmed by the structure of repo markets, the Fed’s own supervisory data, and the MOVE index dynamics I wrote about in Volume 17 when Howell’s “Four Horsemen” note landed at 5:51 in the morning and I realized all four inputs to his Global Liquidity Index were dominoes falling the same way... But there’s a version of the future that may make my thesis incorrect… So, let me try to explain…. If central banks and regulators successfully implement real-time collateral tracking, if the tokenization of Treasury securities improves settlement efficiency and reduces the opacity that makes rehypothecation dangerous, and if the shift toward central clearing for Treasuries (which the SEC has been pushing since 2023) meaningfully reduces counterparty risk in repo markets... then the collateral chain could become stronger, not weaker. I know that’s a mouthful. But this is exactly the level of thinking that seperates the policy maker from the retail investor… It matters. In that world, the multiplier still exists. So does the leverage... But the plumbing would likely, according to people I follow, be better. The haircuts would be more rational, and the system could absorb shocks that would have caused seizures under the old setup... This is the strongest argument against my thesis… The technology to build this exists, and the regulatory intent exists. Plus, the incentive structure points in the right direction, because every major participant in the system... central banks, primary dealers, and clearinghouses alike... would benefit from a more transparent collateral setup... The reason I don’t believe it’s sufficient is timing. The improvements I explaind are being built while the crisis is already in motion. And we’re in a new crisis… that we just moved to from the previous one… You can’t rewire the electrical system of a building that’s already on fire. The March 2020 Treasury market dysfunction happened in a system that already had central clearing for many instruments and already had overnight reverse repo facilities. The plumbing was better than 2008, and it still broke. It broke faster because the system had more leverage and more speed than ever before. The technology argument is real, and over a long enough horizon, it may prove me wrong. But it doesn’t solve the problem on the timeline that matters... which is the next 12 to 24 months.

How Power Really WorksThe third way I could be wrong is brutal and would define black swan territory in terms of political shifts... What if the political system somehow suddenly tolerated deflation? My statements rest on the assumption that no democratic government can sustain a policy of allowing asset prices to fall, credit to contract, and unemployment to rise without eventually intervening. That assumption is backed by decades of evidence. Every administration since at least Ronald Reagan has responded to financial stress with some form of fiscal or monetary expansion. The pattern is so consistent that markets have priced it in... the so-called “Fed put” (a David Tepper production) is not a conspiracy theory, it’s a measurable feature of option pricing. But what if this time is different? I’ll consider it… There’s a scenario in which a government, whether by ideology or by accident, allows a deflationary episode to run its course. It happened in the U.S. in the early 1930s, when policy mistakes and banking failures contributed to a deep deflationary collapse. It happened in Japan in the 1990s, when the Bank of Japan was slow to respond to the bursting of the asset bubble and allowed a decade of stagnation to becomea structural condition. If a political leadership decided... or was forced by circumstances... to absorb a deflationary shock rather than print through it, the entire framework I’ve described would play out differently. The waterfall would drain and stay drained. The containers (like the insane crypto ETFS) wouldn’t fill. The extraction mechanism would shift from debasement to something older and more direct... asset seizure, tax increases, capital controls, or outright default. Yes… that’s what your alternatives are… That world is darker than the one I’ve been describing. In Volume 15, I showed you how the banks extract through managed misconduct. In Volume 16, I showed you how healthcare absorbs $5.3 trillion a year through a subsidy-inflation grift... Those are the mechanisms of a system that prints. The alternative is a world where it takes from you directly, because it no longer has the political will or institutional capacity to print. I don’t think we’re headed there. The institutional infrastructure of central banking is too developed, the political consequences of sustained deflation are too severe, and the precedent of intervention is too embedded for any major government to simply stand by. But I want you to understand that my thesis depends on that assumption. If it breaks, the outcome is not “the system was fine all along.” The outcome is worse. The extraction just takes a different form. The Everyday HustleThere’s a fourth possibility, and it’s the one I’ve heard most often from readers who push back on this series. What if technology solves the problem? Let’s entertain this too… The argument goes something like this. Artificial intelligence is about to produce productivity gains on a scale we haven’t seen since electrification. Those gains will grow the economy faster than the debt grows. They’ll generate tax revenue that brings deficits under control. They’ll reduce the cost of goods and services in ways that offset debasement. And they’ll do all of this without requiring any change to the monetary structure at all. I take this argument seriously because history supports the general principle. Technology-driven productivity growth has, in prior eras, been sufficient to outrun debt accumulation. No doubt about it… The railroad, the telegraph, electrification, the automobile, the internet... each of these waves created enough surplus to allow the system to deleverage, at least partially, before the next expansion. But there are two problems with applying this idea to the current moment. The first is distributional… and you should know this by now. The productivity gains from AI are real, but they are not evenly distributed. They accrue disproportionately to capital... to the companies that own the models, the infrastructure that runs them, and the financial instruments that fund them. If AI increases GDP by 2% but the gains flow to the top decile of asset owners while the wage base stagnates or shrinks, the tax arithmetic doesn’t change. You get a richer economy on paper and the same structural deficit in practice. So… that just leads us to more political charged diatribe… The second is temporal (an underrated word.) Even if AI produces the kind of broad-based productivity revolution that its advocates discuss, the timeline required to restructure the labor market, retrain the workforce, rebuild supply chains, and see those gains reflected in government revenue is measured in decades. The liquidity crisis I’ve described is measured in quarters. The collateral chain doesn’t wait for a productivity revolution to mature before it seizes. So could AI eventually make the debasement thesis obsolete? Over a 20-year horizon, maybe… perhaps… Over the horizon that matters for the positions I’ve recommended... no. I’ll add one more thing that the technology optimists don’t address... something that connects back to the waterfall structure I mapped in Volume 17. Every prior technology revolution happened while the monetary system was also expanding. The internet boom of the 1990s coincided with the Fed cutting rates and expanding credit. The post-war industrial boom coincided with Bretton Woods and a deliberate architecture of managed expansion. Technology doesn’t replace the monetary system. It runs on top of it.

The Real EconomyI’ve identified four ways I could be wrong. The debt burden could become manageable on its own. The collateral system could become resilient enough to absorb shocks without seizing. The political system could tolerate deflation. Technology could produce enough productivity growth to outrun the debasement. None of these are impossible. All of them require conditions that don’t exist though... Now… Before I close the case for my own thesis, I owe you something else. Because if I’m going to be honest about the failure conditions, I also need to be honest about the other thing I’ve spent 17 volumes mostly not saying. The system works as designed. Judge a system by its outcomes… not by its intentions. The system isn’t perfect or fail or without extraction… But it works in ways that have produced material benefits so extraordinary that most Americans have no idea how unusual their daily life actually is. I want to be honest and humble about this… There’s a line in the movie Margin Call... Paul Bettany, playing Will Emerson, a trader staring down the barrel of the 2008 collapse, says it plainly…

That speech bothers people because it’s supposed to be a villain talking. But Will Emerson to me is the hero of the movie… There’s no character in film history that I align with closer than this guy. He sees the whole thing for what it is, and he participates because… what else are you going to do? So let me tell you when that speech hits, it speaks volumes about how good things are… and I’m willing to admit it… So much so that I did some research… The U.S. has the highest average disposable income of any country on earth... $62,722 per capita as of the most recent OECD data. Luxembourg comes second at $47,336. Switzerland at $47,124. That gap isn’t an accident. It’s a structural feature of a system built on the dollar’s role as the world’s reserve currency... what Valéry Giscard d’Estaing famously called America’s “exorbitant privilege.” That privilege means the U.S. government can borrow at rates 10 to 30 basis points lower than it otherwise would. That sounds small until you apply it to $39 trillion in debt and realize it translates to tens of billions of dollars a year in savings that get passed through the system as lower interest rates for consumers, cheaper mortgages, and a financing architecture that no other country on earth can match... The 30-year fixed-rate mortgage is the clearest example of our privelege... It’s a uniquely American product... About 90% of U.S. homebuyers use it, and it exists nowhere else in anything like this form. In Canada, the standard is a five-year fixed. In the UK and Australia, variable rates dominate. The reason Americans can lock in a fixed rate for three decades is that the secondary market for those mortgages is backstopped by government-sponsored enterprises... Fannie Mae, Freddie Mac... which are themselves backstopped by the same Treasury that borrows at privileged rates because the rest of the world holds dollars in reserve. The 30-year mortgage is not a free market product. It’s a downstream benefit of the monetary architecture I’ve been complaining about. The privilege doesn’t stop at borrowing. The dollar’s reserve status means that roughly 58% of global central bank reserves are denominated in dollars, which keeps the currency stronger than it would be on domestic fundamentals alone. A strong dollar makes imports cheaper. It’s why you can walk into a store and buy consumer goods at prices that would be unthinkable in most of the developed world, let alone the rest of it. The cars, the electronics, the cheap energy (at least until recently)... all of it is subsidized, indirectly, by a monetary system that forces the rest of the world to hold and transact in the currency we print. I’m not stupid enough to pretend I don’t benefit from this. I do. You do. Every American who has ever financed a home, filled a gas tank, or ordered something that shipped from overseas has benefited from the system I’ve spent eighteen volumes critiquing. So why am I still writing these letters? Because the question was never whether the system provides benefits. It does. The question is whether the extraction eventually outweighs them. And the answer depends on where you sit. If you own assets... if you hold real estate, equities, or anything else that inflates with the money supply... the system has been very good to you. The annual debasement rate I discussed in Volume 11 is also, by definition, the rate at which asset prices tend to rise over time. If you’re on the right side of that equation, the privilege compounds in your favor. But if you don’t own assets... if you rent, if you earn wages that don’t keep pace, if you save in dollars rather than deploy them into the containers the system builds... then the extraction compounds against you. And it does so silently, year after year, in the gap between what your paycheck says and what your grocery bill confirms. The system gives you cheap mortgages and takes back the purchasing power to service them. It gives you affordable consumer goods and takes back the industrial base that used to make them. It gives you the appearance of wealth and takes back the substance of it, one round of printing at a time. Will Emerson was right. They want what we have to give them. And they don’t want to know where it came from. But you’re reading this letter, which means you do want to know. And now you do. The system works and has always worked. Why? Because of incentives and outcomes. As I said in the Wave Speech, judge a system by its OUTCOMES… It will tell you what it was designed to do… The question is how long the benefits keep pace with the cost... and whether, in a world of $39 trillion in debt, a collateral chain stretched to its mechanical limits, and a political system that can’t tolerate the only alternative to printing... we’ve already passed the point where they don’t. I think we have. I could be wrong about the timing. I’ve said that before, and I mean it. I could be wrong about the severity. The drain may be shallow, the response may be swift, and the next round of expansion may be orderly rather than chaotic. But I don’t think I’m wrong about the direction. The system must expand. And when it does, the people who understand the mechanism will be positioned on one side of the extraction, and the people who don’t will be positioned on the other. That means High Beta stocks first… but we wait until then… That has been the thesis of every volume I’ve written. And after spending the last several weeks honestly looking for the argument that breaks it, I haven’t found one that survives contact with the current data. The Back PageI started this series with a simple idea... that the financial system extracts purchasing power from people who don’t understand how it works, and that the best defense is to see the mechanism clearly enough to step out of its path. Here we are… I’ve mapped the mechanism from the bottom up... from the individual products that absorb your income, to the institutional structures that inflate them, to the regulatory apparatus that manages rather than prevents the extraction, to the monetary architecture that funds them, to the collateral chains that leverage them, to the political constraints that guarantee they continue. And now I’ve tried to break my own argument. If it survives this letter, it’s not because I’m smarter than the counterarguments. It’s because the structure of the system is what it is, and the constraints are what they are, and no amount of wishing otherwise changes the arithmetic. I told you exactly how I could be wrong... But the system still has to refinance $39 trillion in debt. The collateral chain still depends on bond market stability. And the political system still cannot tolerate what happens when the waterfall runs dry. Those three facts haven’t changed since I started writing these letters. And until they do, the thesis holds. The Sovereign MoveThe move doesn’t change… I don’t have a recommendation for you outside of where we started in the midstream where we started with Kinder Morgan (KMI) or in the pipelines that I’ve advocated forever in Energy Transfer (ET)… For now, with the war situation, we have to stay liquid and upstream. I can’t force anything… and I’ve said that you can look at names like Archer Daniels Midland (ADM) and Bunge (BG), but to set stops at the 20-day EMA. On the cash side… remember it’s a position… So…SGOV. BIL. SHV. UUP. Treasury money market funds. The people who built the system aren’t waiting for my permission to use the printer again. They’re waiting for the conditions that make it unavoidable. And those conditions are building in Howell’s data, in the MOVE index, in the repo markets, and in every barrel of oil that passes through a chokepoint under duress. When the printing starts... and it will start... the containers will fill. The question is whether you have capital available to fill them with, or whether you spent it trying to catch a falling waterfall. I’ve done my best to be honest with you across these letters. About what I see, about what I don’t, and now about what would prove me wrong. I’ll be ready to hit the bit when it’s time. For now… take a deep breath… We’re still in the early innings… This may not be what you want to hear… But it’s what you need to hear… Stay positive, Garrett Baldwin About Postcards from the Edge of the WorldThe Postcards Doctrine holds that wealth, power, and stability do not persist through innovation, morality, institutions, or financial sophistication, but through control of chokepoints that remain productive across regime change. Civilizations rise and fall. Ideologies rotate. Technologies obsolete themselves. Financial instruments are rewritten, repudiated, inflated away, or nationalized. What survives is not what performs best in good times, but what continues to function when systems fail, rules change, and authority resets. The doctrine begins with a simple observation: extraction always migrates toward what people cannot avoid. Early on, extraction flows through trade. Then finance. Then regulation. Then platforms. Then metered access. Eventually, it settles on inputs that cannot be substituted, deferred, or digitized. Postcards are sent from the edge of these transitions. Each one documents a moment when the system tightens, when optionality narrows, and when value stops flowing to innovation and starts flowing to ownership. Enjoy.

|

Subscribe to:

Post Comments (Atom)

0 Response to "End of The Quarter: What If I'm Wrong?"

Post a Comment