You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. How To Nail A Job Interview on Iran and Oil MarketsAn answer to a reader's question as if it were part of a McKinsey interview...

Dear Fellow Traveler: Are you a self-appointed expert on oil markets and the Strait of Hormuz today? Great… step on up… We’ve been looking for you… Where have you been hiding? There are consulting companies that might be hiring… and the first step would be a case study-style MBA interview that dives deep into real world shipping problem… It’s my job to help you get that dream job of making PowerPoint presentations… So… let’s go… Time to prep… A reader asked me a question yesterday that kept me up half the night. To simplify it… It asked:

As I noted yesterday, I’m a big fan of midstream oil-and-gas companies. I own Energy Transfer (ET) and several other stocks through investments in various midstream and infrastructure ETFs or closed-end funds. At the same time, I’m deeply concerned about the future of maritime shipping of oil and gas in the Persian Gulf… Insurance costs are surging, Iran has threatened the Strait, and reports tied to mine-laying activity have spooked shipping. The bottleneck will likely create even more problems for Asian nations that need oil to function. The reader took those two things and asked a financial question that deserves your time and energy. A lot of people assume all shipping routes and pipelines are basically the same in terms of returns, risk, and geopolitics... They’re not. That’s why pension managers and institutional investors allocating billions right now have to think very carefully about this exact question. Re-assessing risk and reward is the whole game right now. Entire portfolios are being repriced around that reader’s question. Around 2 a.m., I realized the answer comes down to three things… And we should explore them together… since your interview is in a few hours. Part One: What It Costs to Move a BarrelAs I started to think this through, it dawned on me that this is exactly the kind of question consulting firms like McKinsey or BCG ask in interviews. It goes…

What? You don’t get questions like this all the time? No problem… Let’s do some math. I’ll keep this back-of-the-envelope, but focus on the framework rather than the exact figures… just like I’m talking to some Harvard grad at this made-up Bain interview.

So, if you want to move oil today through the Strait of Hormuz, you need to pay for war-risk insurance. Recently, this cost was about 0.25% of the ship’s value. But as I noted yesterday, premiums have jumped toward 1%, so says the Insurance Journal. (And in some cases as high as 3%, according to Reuters). If a Very Large Crude Carrier (VLCC) - the fanciest of oil tankers - is valued at $200 million, the insurance a 1% for just one trip has increased from $500,000 to $2 million. Assume that premium rolls over every seven days, so you need to get in and out fast. And remember, that’s just insurance for one trip through the Strait. I’m also not including crew hazard pay, additional security costs, or losses due to failure to deliver. Now, what’s the cost of moving oil over land from Texas to Cushing, Oklahoma? Roughly $1 per barrel, let’s say (I don’t have MPLX contracts at my disposal… so we continue out the back of this envelope and make assumptions in this exercise). You move oil through an in-ground pipeline that has no drone threats, no naval escort, and no foreign political premium because it’s located in America, not 7,000 miles away. The shipping route yields to pipelines when surging transit costs crush profit margins. Insurance, rerouting costs (maybe $1.5 million to go round-trip around Africa… the maritime version of “take the long way home”), and risk discounts all make shipping investment less attractive than boring old pipelines. We probably haven’t reached that point for crude oil yet because Brent prices remain high enough to deliver attractive margins, and demand for crude is strong in the U.S. Gulf Coast refining network and in energy-starved places across Asia. But when it comes to LNG contracts, fertilizer, and refined products, the margins are much thinner. And insurers don’t care what’s in the ship’s hull… just that the ship is going through the Strait and that it needs the same insurance policies... Margins are the first thing that cracks. Part Two: Where the Big Money Goes I wish that I had the good problem of running a pension fund and having to decide where to allocate $1 billion. There’s a reason why these managers are selected to run massive amounts of capital. They think of everything… Most people might stop at the cash flow analysis when considering investing in energy midstream infrastructure. But the next question isn’t about the cash flow… It’s about the associated risk of that cash flow. And investors adjust the price they’re willing to pay based on the answer. If you bought a rental house, what matters in real estate? Location… location… LOCATION! A house that generates $2,500 a month is worth your investment if the neighborhood is safe. But that same house generating the same rent in a war zone isn’t worth the same… because the rent might stop flowing in the door. That’s exactly the problem for investors looking at these ships right now. That pipeline to Oklahoma will deliver reliable cash flow in a nation with virtually no geopolitical risk (sometimes environmentalists will beat drums and scream at you). No one is shooting missiles at the pipelines, and no one is flying drones into them. But a giant ship drifting through a narrow passage, with drones buzzing around and mines floating beneath the water, faces a very different situation and risk assessment. The entire global oil trade now has to worry about a guy with a $2,000 drone, PlayStation controller, and a YouTube tutorial. That’s the “asymmetry” (a fancy way of saying that either risk or reward can vastly outweigh the other depending on conditions) that changes everything. Now we’ve done the math on the houses in the two neighborhoods… But here’s the number that matters for the pipeline. It’s somewhere between 5.5% and 8% (back-of-envelope). That’s the range of dividends paid by U.S. midstream companies each year. And the guidance by companies and their expected capital expenditures is easy to track. Kinder Morgan (KMI) already guided adjusted EBITDA of up to $8.7 billion (and a $10 billion backlog) for 2026, with almost all of it driven by natural gas. Enterprise Product Partners (EPD) will invest $2.5 billion to $2.9 billion entirely in the U.S. this year. Investors know exactly what they’re buying. You can generate 7% a year on a pipeline with no geopolitical risk. Why would you chase that same return overseas, where a drone can sink your investment? To justify that risk, you might need to generate 50% to 100% more return than pipelines. All while you get phone calls from clients asking about their exposure to these conditions… what you’re doing about it… and questions from the press as well. You get to answer the same questions again tomorrow… then new ones from the clients you’ve already comforted and reassured the day prior. For the rest of your life. My point is that conversations aren’t coming about asymmetric risk. They’re happening right now across investment offices in America. Part Three: Build New vs. Insure Old Forget whether international shipping gets more expensive. The real question is: when does it become cheaper to build and allocate capital to new infrastructure in America than to keep investing in and insuring the old shipping routes? This third part is what will get you the consulting job if you can stick the landing… Because it’s what really matters - changing incentive structures in a global market. The U.S. already has a massive infrastructure network. About 2.4-3.0 million miles of natural gas pipelines, and 250,000 miles of oil/hazardous liquid pipelines. And we have massive export terminals across the nation… Cove Point, Sabine Pass, Cameron, and Freeport. The U.S. can do the same as the Gulf State nations. We can ship natural gas to Asia across the Pacific Ocean without crossing the Strait of Hormuz. Rather than depending on that chokepoint for energy moving from the Gulf to Asia, you could invest in shipments of natural gas from Louisiana, through the Panama Canal (or alternate global routes), and then across the Pacific to Asian markets. Your ships pass through an open ocean instead of traveling through the Strait with all of its insurance costs and threats from the Iranian Guard. Every new dollar of risk insurance makes that substitution more attractive. Each month that passes, and the Strait faces more pressure, the U.S. natural gas export infrastructure builds faster. The market responds to bottlenecks and incentives. If premiums remain elevated, the math could quickly swing in favor of building new infrastructure over insuring old routes. This is the kind of analysis where small changes move billions of dollars. Three Signals to WatchThe three things you want to assess to reach those breaking points are simple.

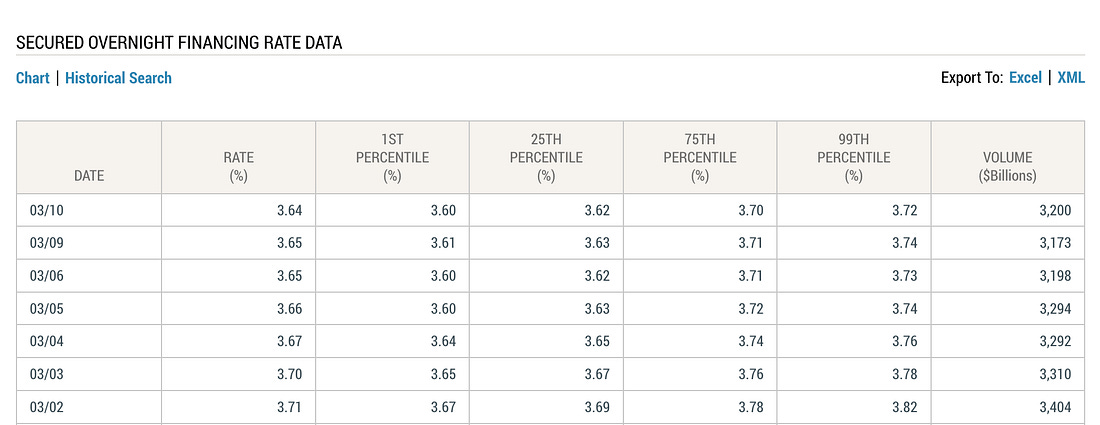

Signal two feels like it’s flashing. Signal one is close. Signal three is the 5-year bet that will start to play out over time... The PunchlineWhen a $2,000 drone can take out a $100 million tanker, the insurance spreadsheet starts looking like a horror movie. That permanently changes the economics of the Strait of Hormuz. Meanwhile, on the U.S. infrastructure side, our pipelines are built and secure. If this trend continues, the winners are not tanker companies. The winners are the boring toll booths. Companies like Energy Transfer (ET), Enterprise Products (EPD), Kinder Morgan (KMI), and the LNG exporters that own the terminals on the Gulf Coast. They collect the toll no matter what happens 7,000 miles away. Many managers are looking at this situation right now and deciding where they want to be in five years. Chevron (CVX) and Exxon (XOM) are already deciding how much future capital to commit to Iraq and other Gulf State nations. Things could change very quickly in the coming months. In conclusion,  Stay positive, Garrett Baldwin Preview for TomorrowThis is the chart you should be watching… The Secured Overnight Financing Rate (SOFR), something I usually called “Funding Rate” because I read too much… This is a problem, as secured lending should not cost as much as unsecured lending does…

I’ll explain what’s going on with SOFR and why it matters as we accelerate toward tax season… a time that money will flow out of money markets and banking reserves. In Case You Missed ItEach morning, I’m doing a quick daily recap called The Morning BRRRR… taking readers through what’s happening in the markets. It’s posted on my Substack for free. What Do You Mean by “Momentum?In recent weeks, I’ve written articles that dive into the key factors driving markets… Money Printer 102 is called “What Do You Mean, Momentum?” Today, I shot a quick video to explain what we’re talking about… So, if you’re new here and just want to listen, here’s the video. Or see the article above.  Please share on social media… And, if you’re not a member, get 30% off your subscription… today. About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "How To Nail A Job Interview on Iran and Oil Markets"

Post a Comment