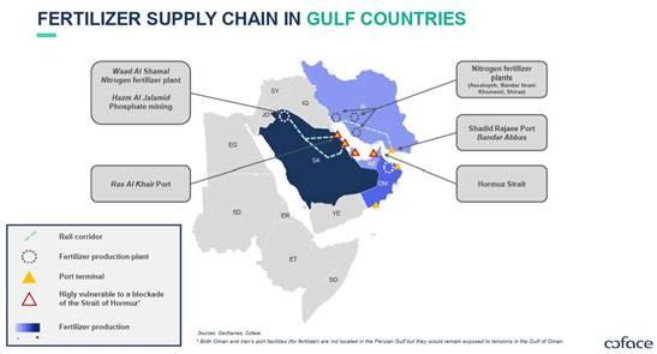

| DAILY ISSUE One Stock to Buy on Oil’s Wild Swings… and Two More in the Wings VIEW IN BROWSER Tom Yeung here with today’s Smart Money. In mid-2022, Eric added Liberty Energy Inc. (LBRT) to Fry’s Investment Report, his flagship stock-picking service. It’s what people will now call “a totally obvious investment.” And it is… at least in hindsight. Eric wrote to his readers… Liberty offers an innovative suite of completion services and technologies to onshore oil and gas exploration and production companies… including next-generation all-electric fracking fleets. Within two years, shares of the fracking company had surged 70% – even as oil prices dropped below $80 per barrel, down from $90. That’s because companies like Liberty don’t rely on sky-high oil prices to make money. The Colorado-based firm earns money from completing new wells, regardless of energy prices. In addition, many of America’s top shale producers are now so low-cost (in part from Liberty’s technologies) that they can remain profitable even if oil falls below $50 per barrel. These are the types of bets we like making: one-sided “heads-I-win, tails-I-don’t-lose” wagers. Markets are once again learning the importance of one-sided bets as the war in Iran turn oil markets into a guessing game. On Tuesday, oil prices continued their double-digit decline after the White House said that “the war is very complete, pretty much.” The Pentagon soon painted an entirely different picture by stating, “We will not relent until the enemy is totally and decisively defeated.” Crude futures soon jumped double digits again. Most speculators are playing the volatility the obvious way. They’re piling into oil ETFs and large-cap energy names… watching the WTI price ticker like it’s a scoreboard and hoping for the best. But oil prices are unpredictable. Speculators win if prices go up… and lose equally if they go down. They might as well make money from guessing coin flips. That’s why I want to look at companies with far better odds. These are investments that should do well, no matter where oil prices go. So, to help protect your portfolios during this Middle East conflict, I’d like to highlight a Fry’s Investment Report holding that should do well, regardless of whether oil surges to $120 or falls back to Earth. The company is dealing with a fertilizer crisis that has barely registered on Wall Street's radar, even as the signals are already flashing. Then, I’ll share where you can find two additional plays that are benefiting from high oil prices. Let’s take a look… | Recommended Link | | | | “I predict OpenAI will go public this year… and I’ve found a little-known way for you to get in BEFORE its shares go public—with as little as $10.” That’s the prediction of Silicon Valley insider Luke Lango. He says this single investment is your best chance to achieve the biggest gains this year… and set yourself up for even bigger gains in the years to come. Best of all, he’s sharing a ticker symbol which you can use to claim a stake right now – for FREE. Click here to learn more. |  | | Winning Wager Buy No. 1 The Middle East isn’t just an oil and gas hub. It’s also a critical supplier of nitrogen-based fertilizers. Since 2020, six countries in the Persian Gulf have exported $50 billion of these crucial agricultural inputs. That means roughly 25% to 30% of global fertilizer exports pass through the Hormuz Strait. Put another way, the Gulf states have a bigger share of the fertilizer market than they do of the oil and gas market.

The most direct beneficiaries have already seen the news reflected in share prices. CF Industries Holdings Inc. (CF) has surged over 45% since the start of the year, while Nutrien Ltd. ( NTR) is up 20%. These companies are major nitrogen-based fertilizer makers and compete most directly with Middle Eastern imports. However, one company has barely risen 7% since January: The Mosaic Co. (MOS). The Florida-based firm is North America’s largest producer of potash and phosphate. In fact, it produces roughly 12% and 10% of the global output of these two nutrients. Now, these two fertilizers are slightly different from the nitrogen-based types that the Gulf states export. So, the stock has barely risen since January. Think of fertilizers like a three-legged stool. Each type represents a different leg, and you need all three to produce a stable crop. It’s why you’ll often see the “N-P-K” acronym on fertilizer bottles, and why fertilizing a lawn without soil testing first is a recipe for disaster. In theory, these three nutrients are not interchangeable. However, different crops need different amounts of N-P-K. Corn requires more nitrogen, while soybeans rely on far less. So, high prices in one type of nutrient can often cause shifts in what farmers plant. That’s why shares of Mosaic should soon rally. Farmers are very sensitive to price inputs, and rising nitrogen fertilizer prices will trigger a stampede into crops like soybeans. One researcher at the University of Arkansas’ System Division of Agriculture is already predicting 3.5 million acres of soybeans this year – a level not seen since 2017. We’re also fast approaching the start of the U.S. planting season. So, even if nitrogen-based fertilizers are allowed past the Hormuz Strait within the next several weeks, many American farmers will have already locked in their potash and phosphate demand for the whole year. In addition, MOS shares are relatively cheap. The stock trades at just half of long-term, midcycle valuations, and so even a return to normalcy gives shares a 2X upside. A windfall from higher fertilizer prices will only add to that. In other words, even if Middle East conflict suddenly ends and we see a deluge of Gulf region products back on world markets, it would be too late for farmers in the Northern Hemisphere to switch back to nitrogen-based crops. MOS remains a top pick in Fry’s Investment Report, and you can get more ideas like this by clicking here. 2 Oil Stocks in the Wings The global energy crisis is real. The oil trade is obvious. And obvious trades are usually already priced in. This week’s wild reversals prove that point. Many speculators piled into oil futures at $120 per barrel… only to see prices fall below $80 within days. They’re now sitting back near $90, as if calling for traders to try again. But there are far better ways to invest in this market. Eric has two key picks in oil and gas in his Fry’s Investment Report portfolio. The first company is at the forefront of America’s shale revolution, and the recent jump in global oil prices now gives it another leg of growth. Here’s the fundamental case. Eric’s first energy pick is one of America’s largest shale oil producers. The firm completed a merger in early 2026 and now produces 1.6 million barrels of oil equivalent per day – enough to fill up 4.5 million cars with gasoline. It is also a relatively efficient producer, especially compared to global averages. The company’s breakeven oil price sits at just $44 per barrel and could reach the low-$40 range on post-merger cost savings. Even with oil prices pulling back, this means the company is still printing money and can still lock in $70-plus prices in the futures market. It’s a guaranteed profit either way. His second pick is in natural gas… and a company that’s quietly dominating the European landscape. Last week, Qatar was forced to shut liquefied natural gas (LNG) production after missile attacks from Iran began targeting energy infrastructure. The country makes up 20% of global LNG exports, and prices in East Asia and Europe have already spiked. What’s worse, sources say it would take at least a month to return to normal production volumes… which might not happen for a while. After all, LNG tankers are essentially floating bombs. That has had an immediate impact on European gas prices, which must compete with Asian buyers for supply. Dutch TTF Natural Gas Futures have spiked from $30 before the conflict to roughly $50… and could rise further as remaining winter stocks are depleted. Meanwhile, Eric’s top European gas pick sits at a valuation that doesn’t reflect its situation. Prices continue to trade almost 20% below their 2022 peaks. That gives it a solid double-digit upside from here. I must also note that the company is astonishingly well run. Production grew 3.4% to record levels in 2025, and management expects another 3% increase in 2026 with breakeven levels of $40/barrel equivalent. This represents a 25% rate of return at $65/barrel of oil. The company has a long history of managing windfall profits, and I expect shares to have double-digit upside from here. The Bottom Line No one can seem to agree where oil prices will go. Betting markets expect oil to retest the $110 level by June, while futures markets expect a steady decline to around $80. But Eric and I are not interested in making these kinds of 50-50 bets. Instead, we’re looking for investments with a greater guarantee of success, or those with such lopsided upside that the risks are worth taking. (With those sorts of speculations, Eric has made 41 stock recommendations that went on to gain 1,000%+… 14 that gained 2,000%+… seven that gained 5,000%+… and two that gained 10,000%+. It’s why he’s often been called “Mr. 1,000%.”) That’s why I think it’s so important that you learn more about these two winning-wager companies at Fry’s Investment Report. If you join, you’ll also get immediate access to all of Eric’s research and portfolio picks, as well as his latest trade alerts and company updates. You can click here to learn more. And in the meantime, be sure to keep checking your email. We’ll be sure to think outside the box when it comes to oil stocks. All of Wall Street’s attention is now fixated on crude oil prices and every word the White House is saying about them. Take that opportunity to hedge with companies beyond their focus. Click here to become a member of Fry’s Investment Report today. Until next time, Tom Yeung |

0 Response to "One Stock to Buy on Oil’s Wild Swings... and Two More in the Wings"

Post a Comment