| |

February delivered a powerful reminder of how emotional markets can become when a dominant trend like artificial intelligence emerges. |

| In the span of a single trading session, a former $3 million karaoke-machine company wiped $17.4 billion off the Dow Transports – an index tracking 20 key U.S. transportation stocks, like airlines, railroads, and trucking giants. |

| No, that's not a typo. |

| A microcap stock with negative EBITDA issued a press release about its AI logistics platform… and shares of stable, multibillion-dollar trucking companies collapsed. |

| That tells you everything you need to know about the environment we're in. |

| I want to make two points. They may seem contradictory at first, but both are true… |

- First, the AI infrastructure buildout is accelerating

- Second, the "AI Fear Trade" has gone too far

|

| The company at the center of the panic is now called Algorhythm Holdings (RIME). Until recently, it sold consumer karaoke systems… But in February, its SemiCab unit claimed its AI platform could reduce empty freight miles by as much as 70% and help customers scale volumes 300% to 400% without adding headcount. |

| Impressive claims. However, the announcement left us with many questions… |

| Most importantly, who are these customers? What do these contracts look like? And does this technology work at scale? |

| None of that mattered to the market, though. Trucking logistics companies plummeted on the day. |

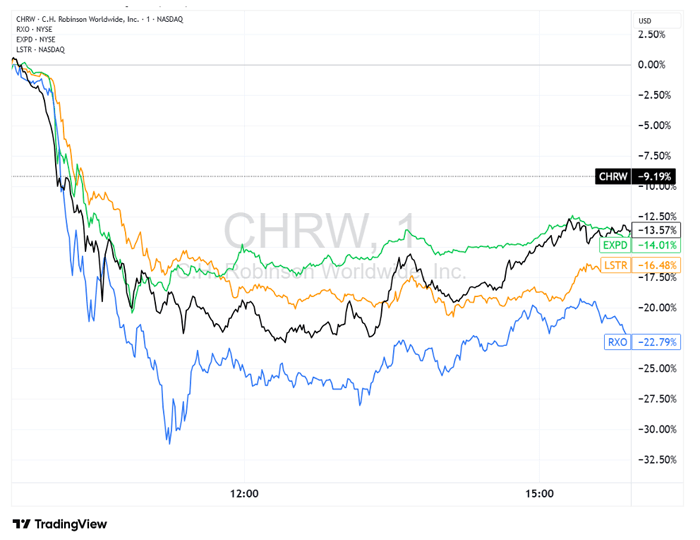

| C.H. Robinson (CHRW) and Expeditors International (EXPD) both fell 14%. |

| Landstar Systems (LSTR) fell 16%, its worst day ever. |

| And RXO, Inc. (RXO) fell the most, ending down 23%. |

| |

| These are all stable, profitable, multibillion-dollar businesses with decades of operating history. |

| And they were pummeled because a microcap with $1.7 million in quarterly revenue and negative EBITDA issued a press release. |

| Now, most of these have already bounced back, but be prepared for more volatility. |

| It's probably just a matter of time until a scare hits a majority of publicly traded companies. For many companies, the drawdown will be temporary, but it will likely feel scary holding those companies at the time. |

| With the market stalling for the past few months, large institutions and hedge funds are using these headlines to scare the weak hands out of their positions. This allows them to enter positions at lower prices and generate alpha in a flat market. |

| Don't be a panic seller. |

| |

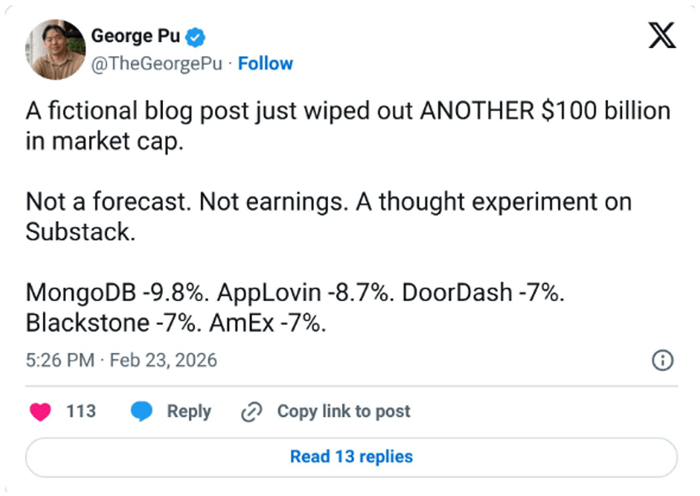

| And it should be noted that this firm is known for its short reports and was positioned to profit if the companies whose business models were questioned fell. This tweet sums up the results the best. |

| |

| This story is stranger than fiction… And it's the kind of reaction that occurs at the end of a large move. |

| Sell First, Ask Questions Later |

| Here at Brownstone Research, we deeply understand that AI advancements will transform the global economy. Entire business models will be dismantled. Middlemen will disappear. Labor productivity will surge. Margins will compress in some areas and explode in others. |

| That part is not up for debate. |

| However, what we're seeing now isn't disciplined forward-looking analysis. It's panic. |

| The "AI Fear Trade" has turned into a sell-first, ask-questions-later stampede. Investors are dumping anything that might be exposed to automation risk. |

| We saw this first in software. The financial media recently labeled it the "SaaS-pocalypse." |

| Personally, I've been calling for the death of SaaS since the summer of 2023. At that point, it was clear that the traditional per-seat SaaS model was vulnerable. If one AI system can do the work of five employees, why keep paying for five licenses? |

| That's rational. And the market has responded accordingly. Former high-fliers like Adobe (ADBE), BILL Holdings (BILL), and HubSpot (HUBS) have all fallen more than 50% since then. |

| Now, many of these names trade at multi-year or even all-time low valuation multiples. And that's despite still generating real cash flow and maintaining strong customer bases. When fear pushes valuations to extremes, it usually signals we're closer to the end of a move than the beginning. |

| And we're already seeing early signs of that shift. |

| Friend of Brownstone Research Jason Bodner has pointed out that institutional capital has quietly started flowing back into select software names. Not indiscriminately, but selectively. |

| The market is beginning to realize that not all software is created equal. |

| Jeff and I have had many conversations about this dynamic. Jeff told me that right now, "Institutional capital is struggling to understand the differences between distinct kinds of software companies and the impact of AI on those businesses' free cash flows." |

| That confusion is creating opportunities. Yes, legacy per-seat SaaS models will face pressure, but AI-native platforms like Palantir (PLTR) will thrive. Companies built with proprietary datasets like Tesla (TSLA) will have a competitive moat. And infrastructure and optimization layers that enable AI adoption, like Snowflake (SNOW), will also thrive. |

| Now, I'm not saying these are necessarily buys right now. But as examples of business models that can thrive in the AI age. These are very different businesses from a generic workflow automation tool charging per user. But the market is currently pricing them with the same brush. |

| That's a mistake. |

| And now the fear is spreading beyond software. |

| We've seen sharp selloffs in real estate platforms, private credit firms, insurance brokers, and wealth managers. All simply because AI might streamline parts of their operations. |

| Yet many of these companies remain profitable, cash-generative, and in some cases, positioned to benefit from AI-driven efficiency gains. |

| This is how thematic panics evolve. First, investors identify real disruption. Then they price it rationally. Then they overshoot. |

| The S&P 500 sits just a couple of percentage points off its highs. But underneath that, the AI Fear Trade has created deep pockets of mispricing. That's where we're focused. |

| Because when investors are selling first and asking questions later, disciplined capital can step in and buy quality businesses at a discount. |

| And that's exactly what we're doing. |

| Because we are more confident than ever about the growth of the AI infrastructure buildout. |

| Recommended Links

Thursday, March 12, at 2 p.m. ET

Jeff's Urgent Nvidia Warning "I believe a March 16 announcement from Nvidia will send hundreds of popular companies crashing… But if you're prepared, you could use it to make up to more than 10 times your money. I'm sharing the details on Thursday, March 12, at 2 p.m. ET. You'll get the name of a bullish pick and a bearish pick, just for attending." – Jeff Brown Click here to register with a single click >>>

(When you click the link, your email address will automatically be added to Jeff's guest list.)

This One Oil & Gas Stock Beat Every Member of the Magnificent Seven Get the name and ticker of this incredible stock here. Plus get details of a deceptively simple strategy with incredible upside and less risk than buying and holding stocks. Larry Benedict just went public with what he's calling "the best retirement play for 2026." Get the details here.

| |

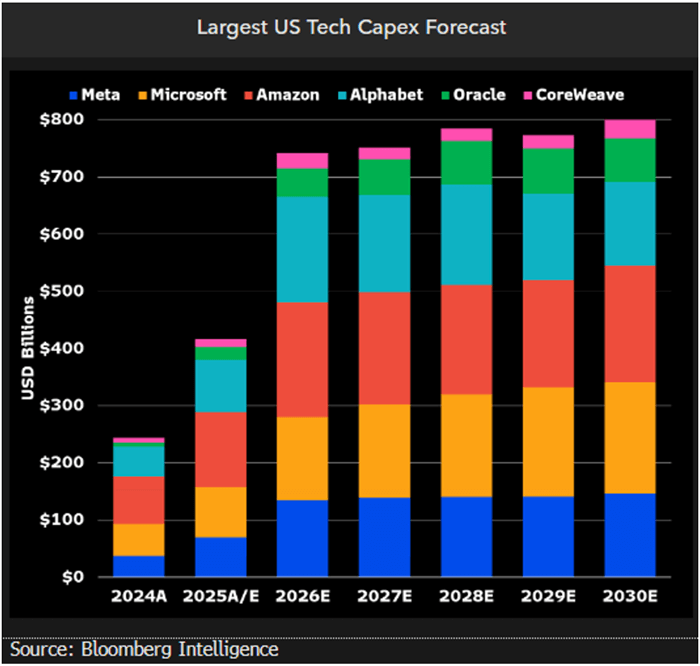

| Earnings Show Increased CapEx |

| Since the release of ChatGPT in late 2022, the world's largest cloud providers have been forced to revise their capital spending plans higher, again and again. Not because they want to, but because they have to. |

| The latest capital expenditure (CapEx) guidance from earnings makes this clear: |

- Amazon: $200 billion in CapEx projected for 2026, versus $125 billion last year

- Google: $175 to $185 billion, up from $91 billion in 2025

- Meta: $115 to $135 billion for 2026, up from $72 billion in 2025

- Microsoft: $110 to $120 billion in 2026, compared to $90 billion last year

|

| Google is effectively doubling its capital spending. Amazon and Meta are close behind. |

| And we haven't even included challengers like Oracle (ORCL), CoreWeave (CRWV), and Elon Musk's xAI. Each of those is pouring tens of billions into AI compute capacity annually. |

| Here's a chart of the growth of CapEx, as well as where Wall Street's future projections are. |

| |

| This clearly demonstrates how Wall Street remains behind on its projections of future CapEx spend. Do we seriously think that hyperscalers won't increase spending in 2027? |

| I fully expect companies and analysts to update 2027 expectations throughout the year. All told, it's reasonable to expect close to $1 trillion in spending next year as companies race to add data center capacity. |

| That number has rattled skeptics. |

| You'll hear the usual chorus from non-technical commentators: There's no guarantee of returns. This is speculative. It's a bubble. |

| But they miss the point. As NVIDIA CEO, Jensen Huang, said during the NVIDIA earnings call last month… |

0 Response to "The Truth About the “AI Fear Trade”"

Post a Comment