Dear Reader,

Pull up Tesla's most recent SEC filing. Page 5.

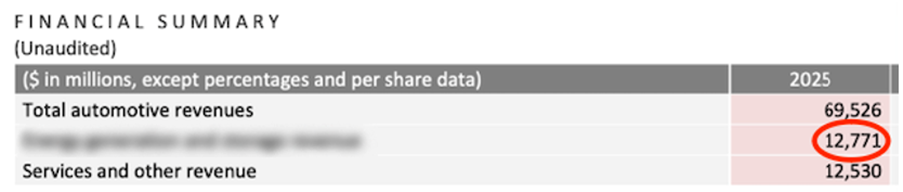

And you'll see a single line showing $12 billion in revenue from a brand-new "super startup" Elon Musk has been quietly incubating inside Tesla.

This new "super startup" has nothing to do with cars, or robots, or space or AI…

But it sits at the center of what Blackstone calls "a $23 trillion investment opportunity."

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he's building.

But former hedge fund manager Adam O'Dell already knows… and he reveals it all in this urgent video.

Adam believes this will go down as Elon's greatest ever invention, and his biggest ever disruption…

And that investors who position themselves before this becomes front-page news could walk away wealthier than they ever thought possible.

Go here to watch Adam's full briefing now... And he'll even give you the name and ticker of one of his top picks to play it — completely free.

Regards,

Adam O'Dell

Chief Investment Strategist, Money & Markets

The Quantum Bubble Is Real Enough to Take Seriously

Authored by Nathan Reiff. First Published: 6/30/2026.

Key Points

- Quantum computing stocks have rallied sharply, but investors still need to weigh valuations against current revenue, profitability, commercial demand and cash burn.

- D-Wave and Rigetti both trade at extremely high sales multiples, with Rigetti’s revenue decline making future contract wins especially important.

- IonQ shows stronger revenue growth and commercial traction, but high R&D spending and potential dilution remain key risks across the sector.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

As with the AI industry, investors often dismiss quantum computing as a potential "bubble." In both cases, however, it is important to understand what that label really means. Quantum technology, like AI, is undoubtedly real and evolving quickly, even if the eventual end goal and practical use cases are not yet fully clear to those outside the field. As a result, concerns about a potential bubble have less to do with the technology itself and more to do with whether current market valuations for quantum companies have become too rich, too quickly, given the state of the underlying technology.

A balanced approach to evaluating a potential quantum bubble must consider valuations relative to revenue, profitability, commercial demand, cash burn, and external threats.

The Valuation Growth Issue

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidMany pure-play quantum computing companies have seen rapid share price appreciation in recent years: D-Wave Quantum Inc. (NYSE: QBTS) is up 68% over the past year, for instance, while Rigetti Computing Inc. (NASDAQ: RGTI) has climbed about 65% during that time.

Investors will want to see revenue rising in a way that supports those valuation gains. In D-Wave's case, full-year 2025 revenue increased 179% year over year (YOY), while Rigetti's full-year 2025 revenue declined from the prior year. Despite D-Wave's impressive growth, revenue remained low in absolute terms, with the company reporting about $25 million for all of 2025.

To keep an eye on how valuation and revenue line up, investors will want to watch metrics like the price-to-sales ratio. Both companies recently traded at extremely high sales multiples, with D-Wave above 700 times sales and Rigetti even higher.

That gives investors reason to question whether those stock prices have moved too far ahead of current revenue.

Rigetti illustrates why that concern is not merely theoretical. Unlike D-Wave, its 2025 revenue declined from the prior year, making future contract wins and revenue conversion especially important for the stock.

Profitability and Demand Concerns

It is not just sales that determine the viability of quantum computing firms. Profitability is essential as well. Many firms in this space still share similar traits, including negative operating margins and free cash flow, heavy R&D spending, and continued reliance on outside capital. While this is typical for companies in their early stages or in a nascent industry, investors will want to know whether valuations are already pricing in profit levels that may still be years away.

IonQ is a good example, particularly because it has some of the largest revenues of any firm in this industry. In Q1 2026, the company reported almost $65 million in sales, up 755% YOY. Beyond strong sales growth, IonQ also has an advantage in that it is quickly building commercial traction—something not all quantum firms have achieved so far.

Even so, with GAAP R&D costs more than tripling YOY to almost $126 million in Q1 2026, IonQ faces a significant hurdle on the path to profitability. Like many other pure-play quantum names, it will need additional funding sources to keep supporting technology development.

A Bright Spot: Cash Reserves

While cash burn remains high, one bright spot for some pure-play quantum companies is their cash reserves. IonQ ended Q1 2026 with $3.1 billion in cash, for instance, while D-Wave has been able to use its cash holdings to make an aggressive acquisition earlier in the year. That suggests these companies have decent runways and are not in immediate danger of collapse. Still, investors will want to see signs that they can eventually generate enough free cash flow to support their expenses.

Another question for investors is whether these companies are building cash reserves in a way that dilutes shareholders. The industry has become known for capital raises through the sale of additional shares, a move that provides near-term cash but can reduce investor appeal and signal longer-term issues.

The Looming External Threat

A final factor for investors to watch is the external threat posed by larger tech firms in the quantum computing space. Companies like D-Wave and Rigetti are tiny compared with rivals that have growing quantum initiatives, such as Intel Corp. (NASDAQ: INTC) and IBM Corp. (NYSE: IBM), both of which have recently signaled plans to double down on their quantum operations.

Interest from legacy tech companies is likely to benefit quantum technology as a whole. However, it may be detrimental—or even catastrophic—for small firms already facing the pressures described above. All of this contributes to the risk profile of these companies, which investors must keep in mind.

Alcoa's $4.1 Billion South32 Deal: Opportunity Behind the 9% Drop

Submitted by Jeffrey Neal Johnson. Article Posted: 7/6/2026.

Key Points

- Alcoa shares fell 9% to $47.41 after the company announced a $4.1 billion agreement to acquire South32 Limited's bauxite, alumina, and aluminum assets.

- The deal, financed through $3.1 billion in cash via a Goldman Sachs bridge loan and 17 million new shares, carries roughly 6% equity dilution but leaves Alcoa's pre-deal debt-to-equity ratio at a conservative 0.36.

- A $750 million contingent value right tied to alumina and aluminum prices through 2030 limits downside risk, while acquired assets are projected to deliver $50 million in annual run-rate cost savings within 12 months of closing.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

When an industrial sector powerhouse announces a multibillion-dollar acquisition, the market's first reflex is often to sell.

Institutional investors are notoriously wary of aggressive mergers and acquisitions in cyclical sectors unless they see immediate, verifiable free cash flow accretion.

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidInvestors are seeing that reaction play out with Alcoa Corporation (NYSE: AA) right now. After executing an agreement to acquire South32 Limited's bauxite, alumina, and aluminum assets for an upfront consideration of $4.1 billion, the market responded.

Shares of Alcoa Corporation plummeted 9%, slicing through an established 50-day range to close at $47.41.

Unearthing a Generational Upstream Aluminum Monopoly

Wall Street is intensely focused on the immediate financing burden, prioritizing balance sheet preservation over asset expansion. A deeper look into the mechanics of this deal reveals a very different reality. By absorbing tier-one bauxite and alumina operations just as structural supply deficits loom, Alcoa may have engineered a generational upstream monopoly at a deep discount.

Bauxite is the primary ore used to produce alumina, which is then smelted into aluminum. Controlling that entire pipeline from dirt to metal gives Alcoa immense pricing power. Investors willing to look past the bridge-financing noise are being presented with a rare opportunity to accumulate shares at heavily compressed multiples.

Sifting Through the Slag: Debt, Equity, and Market Fear

To understand the 9% haircut, you have to look at how institutional block traders model risk. The $4.1 billion upfront price tag requires $3.1 billion in cash and the issuance of 17 million new Alcoa shares. That stock issuance guarantees immediate equity dilution of roughly 6%.

Compounding the dilution is the debt load. To quickly secure the cash requirement, Alcoa tapped a $3.1 billion bridge commitment from Goldman Sachs (NYSE: GS). Bridge loans are temporary, highly expensive financing tools used to lock down a transaction before permanent capital can be raised. The market is arguably pricing in the weight of this short-term paper as a permanent leverage overhang, pushing the maximum enterprise value of the transaction toward $5.6 billion when accounting for assumed lease obligations and contingent payouts.

Investors also have to factor in the existing sentiment surrounding Alcoa. During the most recent earnings report on April 16, Alcoa delivered a slight miss. Earnings of $1.40 per share trailed consensus estimates by 20 cents, while revenues declined 5.2% year over year. That earnings miss created a fragile psychological environment.

When the South32 Limited deal crossed the wire, institutional patience for the long-dated realization of projected cost savings and operational efficiencies snapped. High off-exchange short volume ratios exceeding 62% indicate aggressive risk-off repositioning by institutional block traders rather than a coordinated short attack. Short interest remains benign at 2.48%, totaling roughly 6.5 million shares. Put option volume expiring in early July is clustered heavily around the $48 and $49 strikes, validating immediate downside hedging against the newly announced capital outlay.

Despite the panic, Alcoa's underlying financial health remains intact. Before this transaction, the debt-to-equity ratio was conservative at 0.36, supported by a current ratio of 1.48. Alcoa has a definitive roadmap to permanently replace the bridge loan using balance sheet cash and long-term debt financing well ahead of the anticipated closing in the first half of 2027. The company has the baseline balance sheet capacity to absorb these assets.

Locking Down the Vault: South32 Assets Transform Alcoa

Moving past the financing noise, the assets being acquired fundamentally reshape the global aluminum landscape. The transaction secures full ownership of the Boddington bauxite mine and the Worsley alumina refinery in Western Australia, alongside vital processing interests in Brazil and South Africa.

Alcoa models $900 million in net present value savings across the combined portfolio. While analysts often discount long-term acquisition projections, the immediate cost savings are highly verifiable.

The integration of the Western Australia operations alone is projected to deliver $50 million in direct run-rate cost savings. These savings flow straight into the cost of goods sold within 12 months of closing, countering fears of short-term margin compression.

The strategic alignment here gives Alcoa a commanding scale advantage. With a market capitalization above $12 billion, Alcoa dwarfs two direct upstream competitors, Constellium (NYSE: CSTM) and Century Aluminum (NASDAQ: CENX), which hover near $4 billion. Alcoa also maintains a 0.83% dividend yield, whereas both Constellium and Century Aluminum do not offer dividends, putting the newly expanded company ahead in shareholder returns.

Refining the Balance Sheet With 1 Clever Contingency Clause

One of the most misunderstood components of this buyout is the $750 million contingent value right attached to the deal. A contingent value right provides additional compensation to the seller only if specific performance metrics are met in the future.

In this case, the payout is tightly controlled and directly tied to alumina and aluminum prices through 2030. Alcoa only surrenders this maximum consideration if commodity pricing guarantees outsized free cash flow accretion. The company effectively neutralized downside risk, ensuring it only pays top dollar if the underlying London Metal Exchange commodities generate massive revenue. This keeps the balance sheet highly protected during cyclical downturns.

Institutional Money Anchors Alcoa's Ascent

Global analysts have recently raised their aluminum forecasts on the London Metal Exchange. Structural supply disruptions and geopolitical tensions are setting the stage for multiyear pricing highs. By aggressively acquiring raw-material capacity right before projected 2026 and 2027 supply squeezes, Alcoa is positioning itself to capture massive alpha when the commodity cycle peaks.

Smart money understands this positioning. While day traders focus on intraday block selling, heavy institutional anchoring remains firmly in place. BlackRock (NYSE: BLK) continues to hold a 9.0% stake, representing more than 23 million shares. This deep-pocketed positioning acts as a floor for institutional conviction, offering a layer of baseline support beneath the recent volatility.

The valuation metrics support a bullish outlook. The trailing price-to-earnings ratio for Alcoa is 12.3, while the forward multiple has compressed to an incredibly attractive 6.3. Alcoa is generating $6.05 per share in cash flow, providing ample liquidity to navigate the integration phase.

Melting It Down: Does Alcoa Merit Watchlist Status?

The market reaction to the South32 Limited asset acquisition highlights a disconnect between short-term institutional trading algorithms and long-term business fundamentals. The market is harshly punishing the execution risk and temporary debt load required to consolidate the industry.

The underlying data points to a well-timed expansion. By locking down tier-one mining and refining assets ahead of a global supply deficit, Alcoa is insulating its supply chain and setting the stage for aggressive margin expansion.

Investors willing to look past the bridge-financing noise are being handed a rare opportunity to accumulate shares at heavily compressed multiples. Cautious investors might consider adding this legacy materials producer to their watchlist as the market digests the realities of this newly formed upstream monopoly.

This email message is a paid advertisement from Banyan Hill Publishing, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you would like to unsubscribe from receiving offers for Strategic Fortunes, please click here.

If you need help with your newsletter, feel free to contact our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl. #620, Sioux Falls, S.D. 57103-7078. United States..

0 Response to "Hidden on Tesla's filing: A $12 billion "super startup""

Post a Comment