Dear Reader,

Dr. Mark Skousen here.

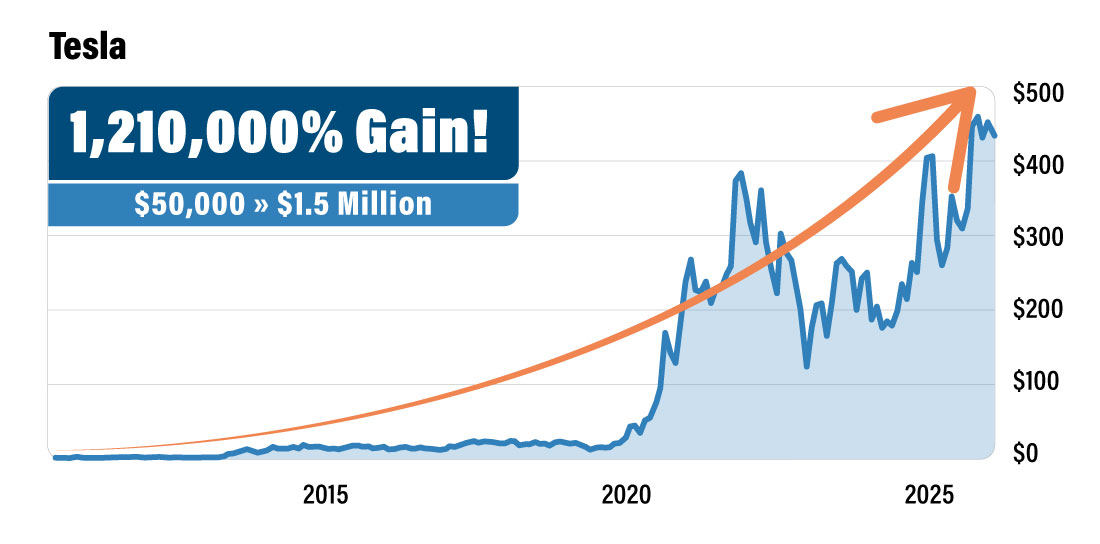

Remember Tesla's IPO?

It launched at $17 a share….

Most people laughed.

Electric cars? That quirky guy who built PayPal?

No chance.

Of course, not getting in on Tesla was a huge mistake…

Today those $17 shares are worth over $250.

Early investors who got in pre-IPO and held on could’ve turned a $50,000 investment into $1.5 million over the next decade.

|

How many people do you know who actually bought?

Almost nobody, right?!?

Well, I was one of the lucky few.

I got into a Tesla-heavy fund back when everyone thought Elon's car company would never make a dime. That early bet added nearly seven figures to my net worth over a decade.

Now I believe Elon's doing it again. This time with SpaceX.

The stakes couldn’t be higher…

And I'm betting on him again.

Industry experts are calling the SpaceX IPO a "seismic event" — a $1.5 trillion valuation that could be the biggest listing in Wall Street history.

Based on my meeting with Elon — combined with my own research — I'm convinced he'll announce the IPO on March 26th.

That's less than two weeks from today.

If you missed getting in on Tesla pre-IPO... don't make that same mistake twice.

And don’t worry. Normally, non-accredited investors are locked out of these types of Pre-IPO opportunities.

But…

I've found a backdoor that lets you grab a pre-IPO stake before Elon makes the big SpaceX IPO announcement.

And I'm sharing the ticker for free.

Just click here to see how to get positioned before the big SpaceX announcement.

Yours for peace, prosperity, and liberty, AEIOU,

Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club

P.S. Bloomberg just reported that S&P is considering a rule change, which could fast-track SpaceX into the index after the IPO. That means billions in forced buying. Get in before that happens. [Click here.]

Costco Wholesale: Buy Now, Get Paid Later as Cash and Returns Build

Reported by Thomas Hughes. Published: 3/6/2026.

Key Points

- Costco’s bull case rests on steady comp growth, store expansion, and strong operating execution that supports cash flow and returns.

- Strong institutional inflows and analysts’ reaction to fiscal Q2 results reinforce the view that Costco can push back toward record highs.

- The special dividend thesis remains intact, supported by balance sheet strength and Costco’s history of periodic special payouts.

- Special Report: Elon's "Hidden" Company

Costco Wholesale (NASDAQ: COST) presents a buy-now, get-paid-later opportunity, with its share price poised to move higher and the special dividend thesis remaining intact.

Shares, up significantly from late‑2025 lows, could rise at least another 20% to reach fresh all‑time highs — and potentially more given current trends.

3 Signs It May Be Time to Switch Financial Advisors… (Ad)

3 Signs It May Be Time to Switch Financial Advisors…

Your goals aren't being heard, you're making costly tax mistakes, or your portfolio strategy may not be aligned with market conditions. This free quiz matches you with vetted fiduciary advisors who serve your area — each legally bound to work in your interest. No cost, no commitment.

Find your matches today.These trends include sustained growth from comps and new stores, strong operational execution and cash flow, growing capital returns, and positive analyst sentiment.

Bullish Analysts and Institutional Flows Point to Fresh Highs for Costco

Analysts play an outsized role in Costco's stock performance by shaping broader market sentiment. The response to Costco's Q2 fiscal year 2026 (FY2026) earnings release was constructive, with multiple ratings and price targets reiterated toward the high end of analyst ranges. As it stands, COST is rated a consensus Moderate Buy with roughly a 5% upside from the pre-release close; the underlying trends, however, point toward a move into the $1,200 area, and other factors support the thesis.

Institutional inflows are also bullish. Institutions own nearly 70% of the stock and have accumulated on balance, buying more than $2 for each $1 sold on a trailing twelve‑month (TTM) basis. Activity accelerated in early Q1 2026, producing about a $4‑to‑$1 buying balance and providing solid support and a strong market tailwind. If that trend continues, Costco likely will retest its all‑time highs by early Q2 2026 and move higher through the year.

Costco Capital Returns and Special Dividends Attract Investor Interest

Capital returns are a key reason analysts and institutions like Costco. Buybacks are incremental, trimming the share count gradually each quarter, while the regular dividend yield is modest but reliable. Accelerated returns remain possible. Costco has paid special dividends every few years and appears well‑positioned to do so again. Although management has not signaled a special distribution, the balance sheet resembles the conditions that supported prior special payouts — which could be in the neighborhood of $15 per share or more.

Costco’s balance sheet underscores its strong capital position and cash generation. Q2 FY2026 highlights include a 22% year‑to‑date increase in cash to more than $17.3 billion, higher assets, reduced long‑term debt, ultra‑low leverage, and rising equity. Equity increased about 10%, which supports the stock outlook. All else equal, a 10% rise in equity can help translate into a similar increase in market capitalization and share price relative to six months earlier. As of early March, the stock price is relatively flat while the share count is slightly lower.

Costco Falls After Solid Report, Signs of Acceleration

Costco delivered a solid quarter, with revenue up a peer‑leading 9.1% to $69.6 billion. The top line beat MarketBeat's consensus by roughly 40 basis points, driven by new‑store openings and comp sales. Comps were 6.7%, with Canada and International up about 7% and U.S. comps up 6.4%. Digital comps rose 21.7%, and membership fee revenue increased 13.6%, all of which suggest comp momentum can continue into future quarters.

Margin performance was strong: improved efficiency and favorable mix helped operating margin expand and net margin strengthen. GAAP EPS of $4.58 rose by nearly 14%, and the company's commentary and February sales figures indicate further improvement in the current quarter. Costco does not provide formal forward guidance, but the disclosed sales trends point to acceleration versus the prior quarter.

The chart's price action was muted after the release. COST shares slipped roughly 0.5% but remained above key support levels and aligned with the stock’s 2026 rebound. There is always the risk of additional selling in early trading, but any decline is unlikely to be severe. The more probable path is for Costco to consolidate around its early‑March levels before moving higher later in the year — either catalyzed by upcoming events or quietly as continued accumulation absorbs available shares and gradually lifts the price.

Energy Vault Electrifies Market With Accelerated Growth

Reported by Thomas Hughes. Published: 3/19/2026.

Key Points

- Energy Vault’s latest quarterly update showed sharply higher revenue and improving profitability metrics alongside a larger contracted backlog.

- Management’s 2026 outlook calls for continued top-line growth, but margins and cash generation remain key execution tests.

- Analyst sentiment has been cautious, while institutional ownership remains significant and short interest is notable.

- Special Report: Elon's "Hidden" Company

Energy Vault (NYSE: NRGV) faces risks and hurdles but appears on track to sustain high growth, improve profitability, and deliver value for investors. The Q4 release and guidance update not only reaffirm the company's trajectory but also show its flywheel generating cash flow faster than expected. A key highlight: the bottom line. The company's revenue surge and operational execution produced a surprise adjusted profit, positive cash flow, and stronger capitalization — trends management expects to continue into 2026.

What is Energy Vault? It is a utility-grade energy storage company focused on colocated storage for renewable projects. A differentiator is a gravity-fed system for long-duration storage: towers and cranes lift and lower heavy blocks to store potential energy, similar to the weights in a cuckoo clock. That approach enables long-term storage without degradation, unlike conventional batteries. The company also offers lithium-ion, hydrogen, and hybrid solutions for municipalities, industries, and major utilities.

Energy Vault Outperforms and Issues Hot Guidance for 2026

Elon Musk already made me a "wealthy man" (Ad)

I Met Elon Musk "Face-to-Face"

During a private gathering of Wall Street elites, I was one of two people selected to speak with Elon personally.

As a result, my research now leads me to believe Elon will announce the SpaceX IPO on this date:

March 26, 2026. Circle it on your calendar.

I'm sharing an "access code" that lets anyone grab a pre-IPO stake before it happens. This is your invitation to the biggest wealth-building event of the decade.

Click Here to See how to Get Your "SpaceX Access Code"Energy Vault reported a robust quarter driven by a massive capacity ramp. The company increased operating and contracted capacity by 8.3x on a trailing-12-month (TTM) basis, helping Q4 revenue surge 358% to $153.3 million — roughly 50 basis points above consensus. Revenue strength and execution quality are accelerating the path to profitability.

Q4 2025 showed a sharp improvement in GAAP gross profit, with gross margin expanding by more than 1,000 basis points, alongside positive adjusted EBITDA and positive adjusted net income. In short, Energy Vault returned to positive adjusted earnings in the quarter, giving management confidence to issue stronger guidance and an improved profitability outlook.

As strong as Q4 and 2025 were, 2026 could be better. The company forecasts 30% revenue growth at the mid-point, well above MarketBeat's consensus. That outlook is supported by the TTM capacity ramp and a backlog that grew 42% sequentially and 300% year-over-year (YoY) to more than $1.3 billion.

Cash flow is another important detail. Energy Vault improved its cash position in Q4 through operations and capital raises, and expects to build on that in 2026. That suggests the company is better capitalized for the year ahead, reducing the near-term threat of dilution or increasing debt and moving closer to sustained profitability.

Energy Vault Analysts at Odds With Results: Institutions Indicate Accumulation

MarketBeat did not track any analyst updates in the immediate hours after the release, but revisions are likely. The Q4 results and update run counter to recent trends of price-target cuts, downgrades, and concerns about capitalization and growth.

Those results may not immediately change the sell-side's stance, but they should prevent sentiment from deteriorating further. The stock currently carries a consensus Reduce rating from five analysts, reflecting a 60% sell-side bias; the group views the stock as overvalued near $3.80. Institutions, however, appear to disagree. Institutional data show this cohort owning roughly 40% of the market and accumulating in early 2026, buying more than $2 for every $1 sold.

Institutional activity coincides with a reversal in the share price. NRGV hit a low in 2025 and subsequently moved above a pair of moving averages, signaling potential for a higher rally. During 2026, a pullback found support at a critical pivot point, which has begun to shift market sentiment.

In this scenario, the bearish tide appears to be shifting toward a more bullish one and could gain momentum as the year progresses. The pace of any move depends on upcoming news, continued institutional buying, and how analysts revise their views. If analysts adopt a more constructive stance, the stock could retest the $6 level and perhaps move higher. A key risk is short interest: short sellers increased positions before the report and could cap gains around that level.

to bring you the latest market-moving news.

This email is a sponsored email sent on behalf of The Oxford Club, a third-party advertiser of TickerReport and MarketBeat.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103-7078. United States..

0 Response to "Remember Tesla?"

Post a Comment