Few startups have revolutionized the world as quickly as OpenAI, the company behind ChatGPT.

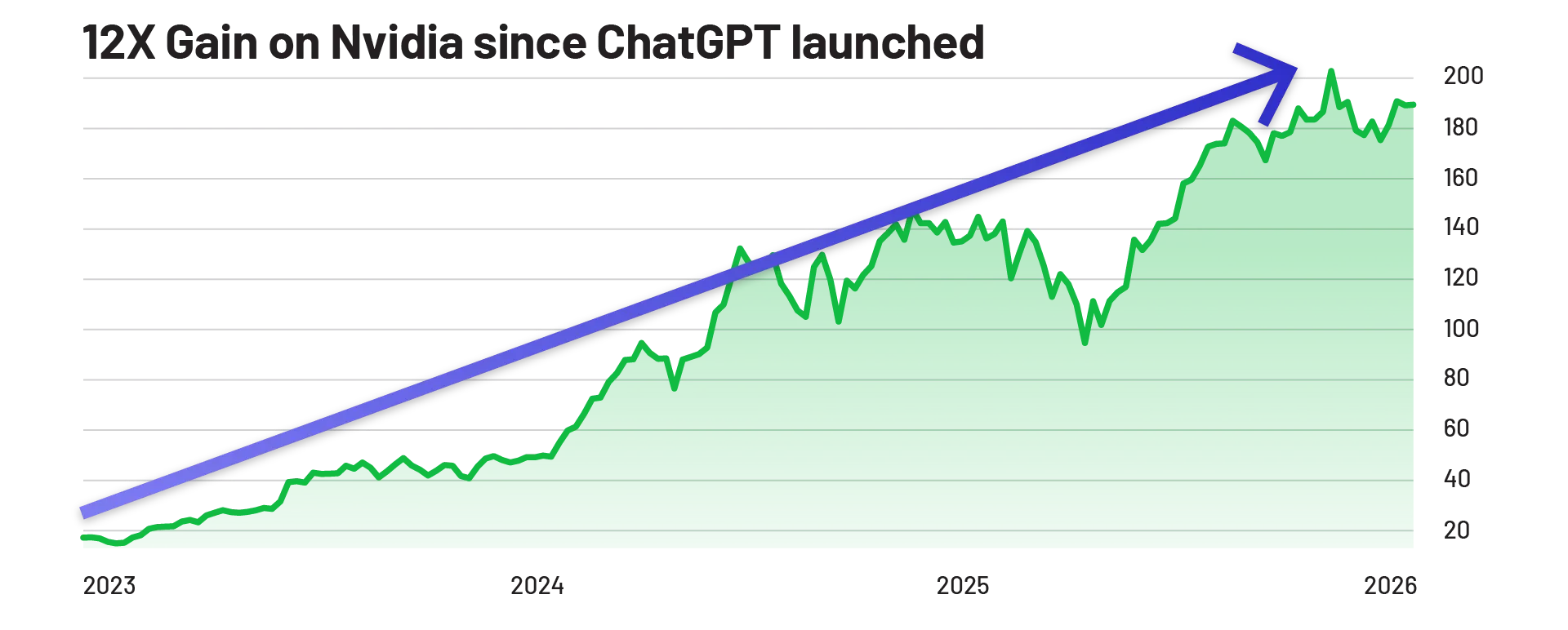

Especially when you consider that investors have ALREADY used its early growth to capture a 12X gain on Nvidia.

An even more lucrative, pure-play way to invest in AI...

Which I'm convinced will capture nearly ALL the attention and money the market has thrown at AI "picks and shovels" stocks like Nvidia.

In short, I predict OpenAI will go public THIS YEAR...

And that this IPO will shatter ALL previous Silicon Valley records... dominate this year's headlines... and create thousands of new millionaires...

This is hands-down the best chance for you to achieve the biggest gains this year... and set yourself up for even bigger gains in the years to come.

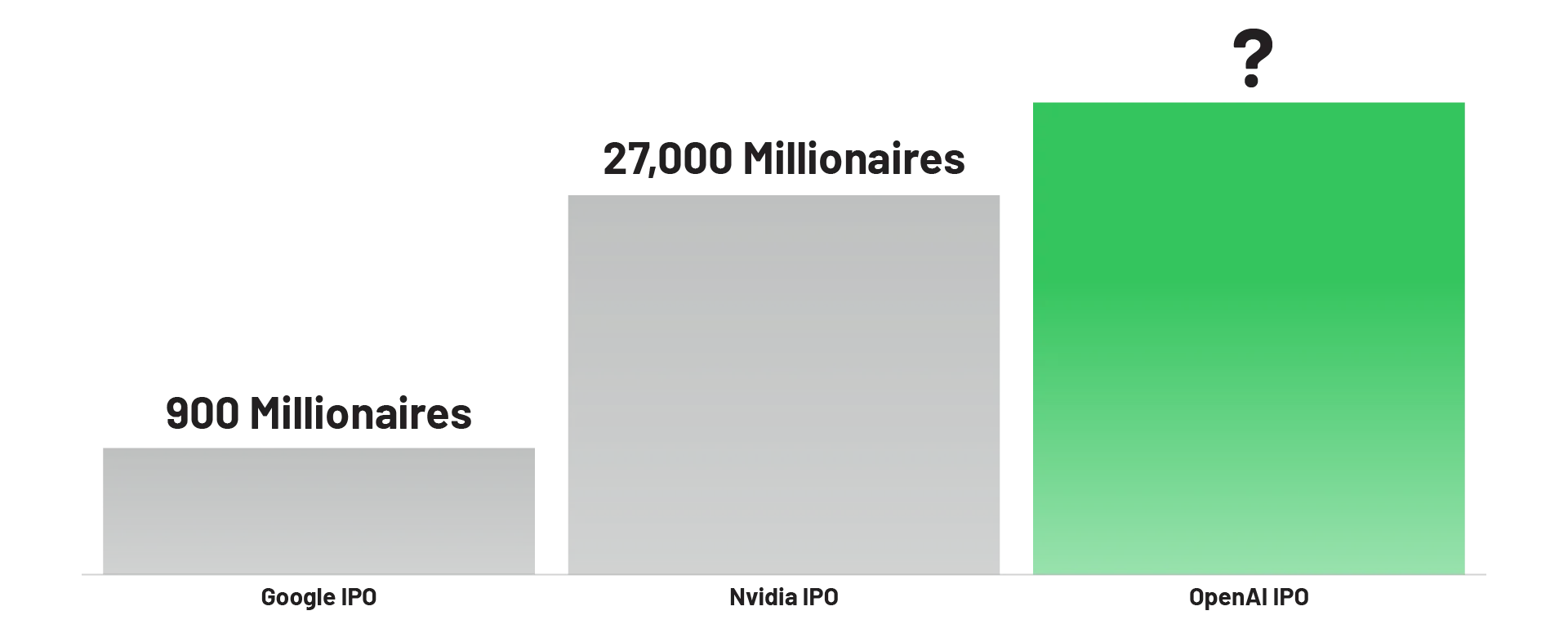

Don't forget, Google's IPO instantly created 900 millionaires.

Nvidia minted over 27,000 millionaires—just among its employees.

I believe OpenAI has the potential to launch even more million-dollar fortunes.

Key Points

- Salesforce is acting quickly to buy back its stock, announcing a huge accelerated repurchase program.

- DocuSign's buyback capacity now exceeds 25% of its market capitalization with shares down nearly 50% from recent highs.

- As the memory shortage delivers blows to Qualcomm, the company just pushed its buyback authorization above $20 billion.

- Special Report: Do this before SpaceX IPOs or be sorry

Stock buybacks are generally bullish for shareholders. Besides signaling that management may view its stock as undervalued, repurchase programs reduce the number of shares outstanding and can increase earnings per share.

Recently, Salesforce (NYSE: CRM), DocuSign (NASDAQ: DOCU), and Qualcomm (NASDAQ: QCOM)—three well-known tech names that have all seen dramatic drawdowns this year—announced large buyback programs that should catch investors' attention.

All three have fallen at least 30% from their 52-week highs, and their management teams are signaling confidence by committing significant capital to buybacks at prices they appear to view as depressed and likely to rebound from.

Salesforce Announces Record $25 Billion Accelerated Repurchase

Salesforce has become one of the poster children of the so-called "SaaSpocalypse," with CRM shares down about 35% from their 52-week high. "SaaSpocalypse" is shorthand some observers use to describe broad declines among many Software-as-a-Service (SaaS) companies, partly driven by concerns that new artificial intelligence (AI) tools could reshape software economics.

As AI lowers the barrier to coding, investors worry legacy SaaS growth could slow: customers might use AI to build similar applications, or AI-native vendors could create comparable tools at lower cost and pressure pricing.

Salesforce, however, views AI as an enabler. Its AI add-on AgentForce recently surpassed $800 million in annual recurring revenue, a 169% year-over-year increase.

Management remains confident and has backed that conviction with action. Salesforce announced its largest-ever $25 billion accelerated share repurchase (ASR), equal to roughly 14% of the company's about $180 billion market capitalization.

ASRs are a particularly strong signal because they represent the fastest way for a company to repurchase stock, indicating Salesforce likely views its shares as significantly undervalued—a view echoed by Wall Street.

Analysts see nearly 44% potential upside for CRM over the next 12 months. The consensus rating is Moderate Buy, with 27 of 39 analysts assigning a Buy.

DocuSign Lifts Repurchase Authorization to $2.6 Billion

DocuSign has faced many of the same AI-related questions that have pressured other software names.

The stock is down nearly 50% from its 52-week high, including a decline of about 30% in 2026. DOCU now trades at a forward price-to-earnings (P/E) ratio near 11x, only slightly above its all-time low.

Like many software companies, any negative impact from AI disruption hasn't yet shown up in DocuSign's results. The company posted 8% sales growth in 2025, in line with prior years, and expects similar growth and relatively stable margins this year.

But markets are forward-looking and are weighing whether results could deteriorate and whether guidance will hold up.

Still, DocuSign is signaling confidence through buybacks. Alongside its latest earnings release—its 13th consecutive quarterly earnings beat since Q3 2023—the company raised its repurchase authorization by $2 billion. That brings total authorization to $2.6 billion, or roughly 28% of DocuSign's approximate $9.5 billion market capitalization.

The firm spent about $269 million on buybacks in the latest quarter, up 66% year-over-year. The new authorization suggests that pace could accelerate. Analysts are bullish as well, forecasting more than 41% potential upside over the next 12 months.

Qualcomm Boosts Buybacks as Memory Woes Weigh on Shares

Shares of semiconductor giant Qualcomm are trading about 35% below their 52-week high.

Qualcomm has limited exposure to the AI data-center megatrend, which has contributed to underperformance relative to many large-cap chip peers in recent years.

Ironically, Qualcomm's largest market is being hurt by the AI buildout. Handsets—essentially smartphones—accounted for about 64% of revenue in the latest quarter. The company expects handset sales of around $6 billion next quarter, a 13% year-over-year decline, as smartphone makers cut orders because they can't secure enough DRAM to assemble complete phones.

Memory suppliers are reallocating DRAM capacity toward high bandwidth memory (HBM) needed for advanced AI systems, which offers larger and higher-margin opportunities. That shift has constrained smartphone assembly and left Qualcomm at a disadvantage in the near term.

Nonetheless, Qualcomm is confident in its long-term prospects, citing traction in automotive and a sizable robotics opportunity. The company announced a $20 billion buyback authorization, bringing total repurchase capacity to $22.1 billion, or about 17% of its roughly $137 billion market capitalization.

The timing of the buyback is notable: analysts forecast more than 29% potential upside over the next 12 months.

When Shares Slide, Buybacks Speak

Across Salesforce, DocuSign, and Qualcomm, the common theme is scale: each company is allocating substantial capital to repurchase shares after steep declines. Buybacks don't eliminate the fundamental risks that prompted the selloffs, but they do put real money behind management's view that valuations have become more attractive.

Among the three, Salesforce's accelerated share repurchase is the strongest statement, reflecting both urgency and conviction. The bigger test will be execution and whether upcoming results convince the market that the AI-related fears weighing on legacy software are overstated.

0 Response to "The IPO that could dwarf Nvidia's 27,000 millionaires"

Post a Comment