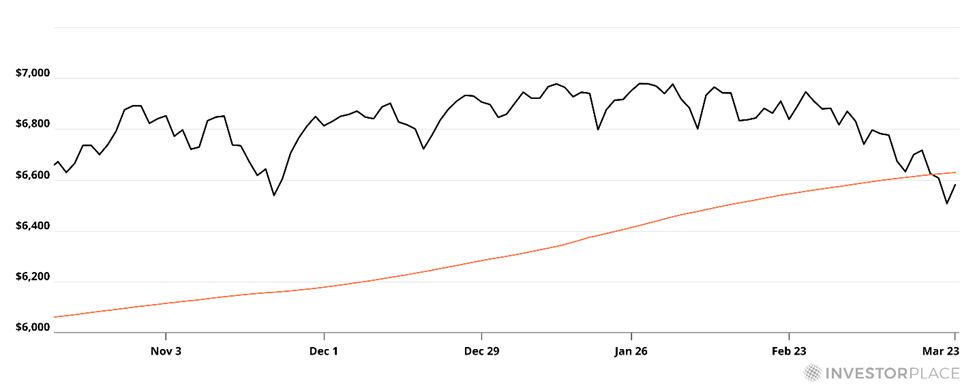

What happens now that we've lost the 200-day moving average… will we have an off ramp in the Middle East… how to invest despite volatility… when lofty valuations aren't so lofty VIEW IN BROWSER Three weeks… That’s our make-or-break window. In yesterday’s Digest, we highlighted two opposing market influences… On one hand, there was the President Trump-inspired relief rally built on shaky geopolitical footing…on the other hand, there was the S&P’s technical damage after it broke below its 200-day moving average (MA). As I write on Tuesday, the S&P is trying to build upon yesterday’s rally, but – at least for the moment – it hasn’t successfully retaken its 200-day MA.

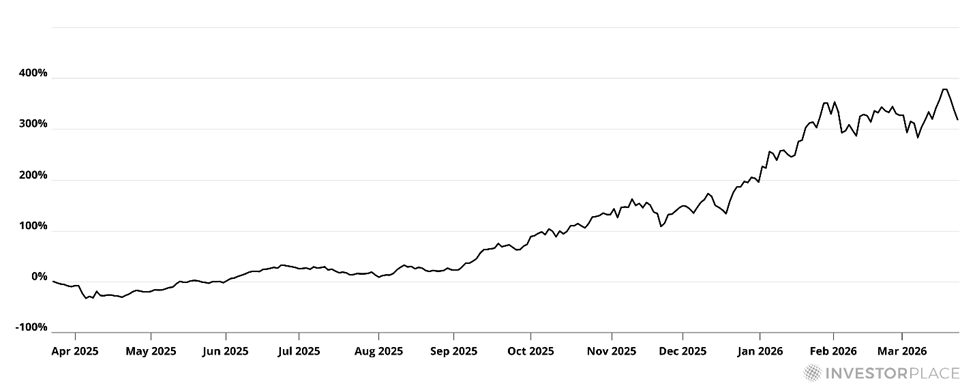

Historically, this moment tends to separate routine shakeouts from something more serious. Let’s go to hypergrowth expert, Luke Lango, from yesterday’s Innovation Investor Daily Notes: The next few weeks are critical… When the market retook its 200-day and then continued the rally over the next 3 weeks and didn’t look back, that almost always led to a really strong 12-month rally for stocks. But when the market…fell back below its 200-day within the next 3 weeks, that almost always led to underperformance… So, the next 2–3 weeks will be crucial. This analysis aligns with the framework we discussed in yesterday’s Digest. The last four weeks have pushed the S&P below its 200-day MA and to a fresh six-month low – two red flags that Editor Brian Hunt identified as fingerprints warning of a potential more serious drawdown. Yesterday’s rebound (and our budding rebound today) didn’t erase that risk – rather, it simply started the three-week countdown that Luke identified. Luke believes the chances are good that the market is leaning the right way, driven by a fast-moving geopolitical shift: Path A — Successful Off-Ramp: 85-90%. The highest confidence we’ve had at any point in this three-week conflict… Here is the signal that matters above all others today: it isn’t just stocks. Every major asset class is simultaneously pricing the same conclusion. That is not sentiment. That is conviction. So, the setup is clear… If a rally holds, builds, and drives the S&P above its 200-day MA over the next few weeks in a V-shaped rally, the recent volatility will likely be remembered as a shakeout as we push higher into summer. If it doesn’t, the technical damage we flagged yesterday will reassert itself and drive us lower. This is the binary we’ll be tracking with you here in the Digest. Now, stepping back, what happens over the next three weeks will tell us a lot about the market’s near-term direction – but it won’t change the market’s ultimate destination. Because regardless of how this 200-day MA drama resolves, one trend continues to dominate the long-term investment landscape… | Recommended Link | | | | Louis Navellier, who spent 47 years on Wall Street, says this is the beginning of the largest wealth transfer in American history. He’s identified the 10 companies poised to capture it — and the ones being destroyed by it. Watch His Urgent Briefing. |  | | AI isn’t just a boom – it’s a wealth transfer History suggests that transformative technologies create enormous value – and much of that value accrues to the companies that build and deploy them, and to the investors who own them. That “Thanks, Captain Obvious” quote comes from BlackRock CEO Larry Fink in his annual letter to shareholders. He went on to highlight a point we’ve made repeatedly in the Digest: There’s a real risk that artificial intelligence could widen wealth inequality if ownership does not broaden alongside it. Fink’s overall message was that if AI is going to reshape the economy – and potentially displace jobs – the best defense isn’t fear…it’s investing in this revolutionary technology. Now, yes – Fink saying “buy stocks” is a bit like a casino owner telling a gambler that the best way to win big is to bet even more… Still, we agree with the overall message. After all, if a technology threatens your income, one of the few moves you have is to align your wealth with that technology. Own the companies. Own the infrastructure. Own the upside. One of the risks today is how much investors are paying for that upside Many of the obvious AI stocks have already been bid up to levels that, historically, underperform over a longer-term timeline. Let’s go to our macro investing expert Eric Fry for more details: Markets are cyclical – always and forever. Share prices oscillate between low valuations and high ones… then back again. Lowly valued stocks, generally speaking, tend to treat investors well, while richly valued ones tend to treat them poorly. The lesson is almost insultingly simple: Buying stocks at low valuations tends to work out better than buying them at high ones. That’s the tension investors face right now. Yes, you want exposure to AI. But no, you don’t want to overpay at the top of a cycle – especially if the next three weeks bring a failed rally. And there’s an even bigger wrinkle emerging beneath the surface… AI isn’t just creating new winners – it’s actively destroying parts of the market. We’re already seeing this play out in software. AI tools are compressing pricing, automating workflows, and threatening entire categories of recurring revenue. Business models that once looked durable are suddenly looking vulnerable. This points toward one fundamental question that investors should ask today when evaluating a stock… Will AI destroy this company’s future cash flows…or accelerate them? The answer is everything. It’s the difference between overpaying for a stock where AI weighs on revenue and intensifies valuation pressure…and owning a business whose earnings are about to accelerate thanks to AI, easing the strain of a sky-high multiple. And this is where Eric’s recent Investment Report issue – highlighting the HALO framework – becomes incredibly useful. Focus on where AI demand is exploding – not eroding To make sure we’re all on the same page, HALO stands for “high-assets, low obsolescence.” Here’s Eric with more: The HALO trade is the straightforward idea that you can protect your wealth through buying assets that cannot be replaced by artificial intelligence. Instead of chasing the most obvious AI winners – many of which are already priced for perfection – you look for businesses tied to physical assets… real-world constraints… and irreplaceable infrastructure. These are areas where AI isn’t replacing businesses – it’s relying on them. One of the clearest examples today is memory. As AI demands shift from software to infrastructure, the memory industry has transitioned from a cyclical commodity into a strategic, capital-intensive asset that is critical to AI hardware. One of the poster children for the memory trade is Micron (MU). Here’s Eric speaking about Micron and our broader point in last Friday’s Digest takeover: Micron’s memory sits at the heart of AI, data centers, and virtually all modern computing systems In a world without enough DRAM, the AI Revolution hits a hard ceiling because it runs out of space to think. No memory means no intelligence. In other words, memory is not a “nice to have.” It’s a critical bottleneck. But what about its valuation? If you keep a pulse on the markets, you might think, “Jeff, Micron is up more than 300% over the last year. Isn’t this exactly what Eric warned about?”

That’s a fair question. On price alone, it does look like a “buy high” situation. But here’s where digging deeper matters… Given Micron’s positioning as a critical HALO stock within the wider AI supply chain, demand for its products – and therefore its earnings – have exploded alongside its stock price. Let’s look at the resulting impact on MU’s valuation. For context, the S&P’s current price-to-earnings ratio is 28. Meanwhile, over the last 10 years, Micron’s price-to-earnings ratio has fluctuated between 13 and 20, with a median of around 15. So, what is MU’s forward price-to-earnings ratio, which includes analysts’ forecasts of 12-month forward earnings? Roughly 7X – 8X. In other words, what appears expensive based on “yesterday’s” earnings and the recent price runup may actually be attractive if MU’s future earnings materialize as forecasted. Eric isn’t our only analyst who has flagged MU recently. Legendary investor Louis Navelleir just sounded off on the memory giant in yesterday’s Growth Investor Flash Alert: Micron is a great buy at this moment. They had spectacular results, but their sales are forecasted to be up over 236%. Last quarter it was 196%. So, the sales growth is just ridiculous, really due to the data centers. Own the bottlenecks, not the hype Zooming out, memory is just one example of how bottlenecks are creating opportunities in HALO stocks. As Eric has been emphasizing, beyond memory, the AI boom is running headfirst into real-world constraints in energy, raw materials, and semiconductor capacity. Each of these pressure points reflects the same underlying dynamic: demand is accelerating far faster than supply can respond. And when that happens, opportunity follows. That’s the bigger takeaway: You don’t have to chase the most obvious AI winners or pay peak valuations for the market’s favorite names. In fact, with the market in a make-or-break period over the next three weeks, this is a time to take fewer risks, not more. But keep your eye out for stocks that AI cannot function without – the areas where demand is inelastic, supply is constrained, and pricing power is building. If the coming weeks bring sale prices, consider establishing positions. For more on these bottleneck stocks, Eric went into far greater detail last week in his FutureProof 2026 event. He walked through the specific pressure points forming across the AI economy and, more importantly, highlighted the companies positioned to benefit. Bringing this back to Fink, that’s really the more actionable version of his message Yes, investors need exposure to AI. But the how matters. It’s not about blindly buying whatever has “AI” attached to it. It’s about owning the parts of the ecosystem where AI is driving demand, strengthening margins, and accelerating future cash flows. That’s how you align your wealth with this technology – and do it without falling into the trap that history has punished time and again: overpaying for the most crowded trades at exactly the wrong time. We’ll keep tracking this here in the Digest. Have a good evening, Jeff Remsburg (Disclaimer: I own MU.) |

0 Response to "The Next Three Weeks Could Determine Your Investing Year"

Post a Comment