Since the outbreak of war, gold is down roughly 3.5% – and prices of the best gold stocks are down even more. Why isn’t gold going up?

Let me explain:

First of all, gold rose roughly 180% from its bottom in 2022. A move that massive is not normal. Every repricing event is always followed by a rest.

Some of gold’s sideways price action is nothing more than gold taking a breather after a blistering run in 2024-2025.

Secondly, most people think gold is a crisis hedge that benefits when the world erupts in chaos. This is true – but probably not the way you think…

Yes, you want to own plenty of gold when the world is in chaos – like now.

But the gold price normally doesn’t go vertical when the bombs start falling.

Gold is primarily a slow-moving, long-term play on the decreasing value of paper assets and fiat currencies – aka inflation.

War will certainly accelerate the decline of the dollar’s purchasing power, but this doesn’t show up in the gold price immediately after a war begins.

In fact, the initial reaction to the war in Iran was for the dollar to strengthen.

It’s still seen as a safe-haven asset by most of the world.

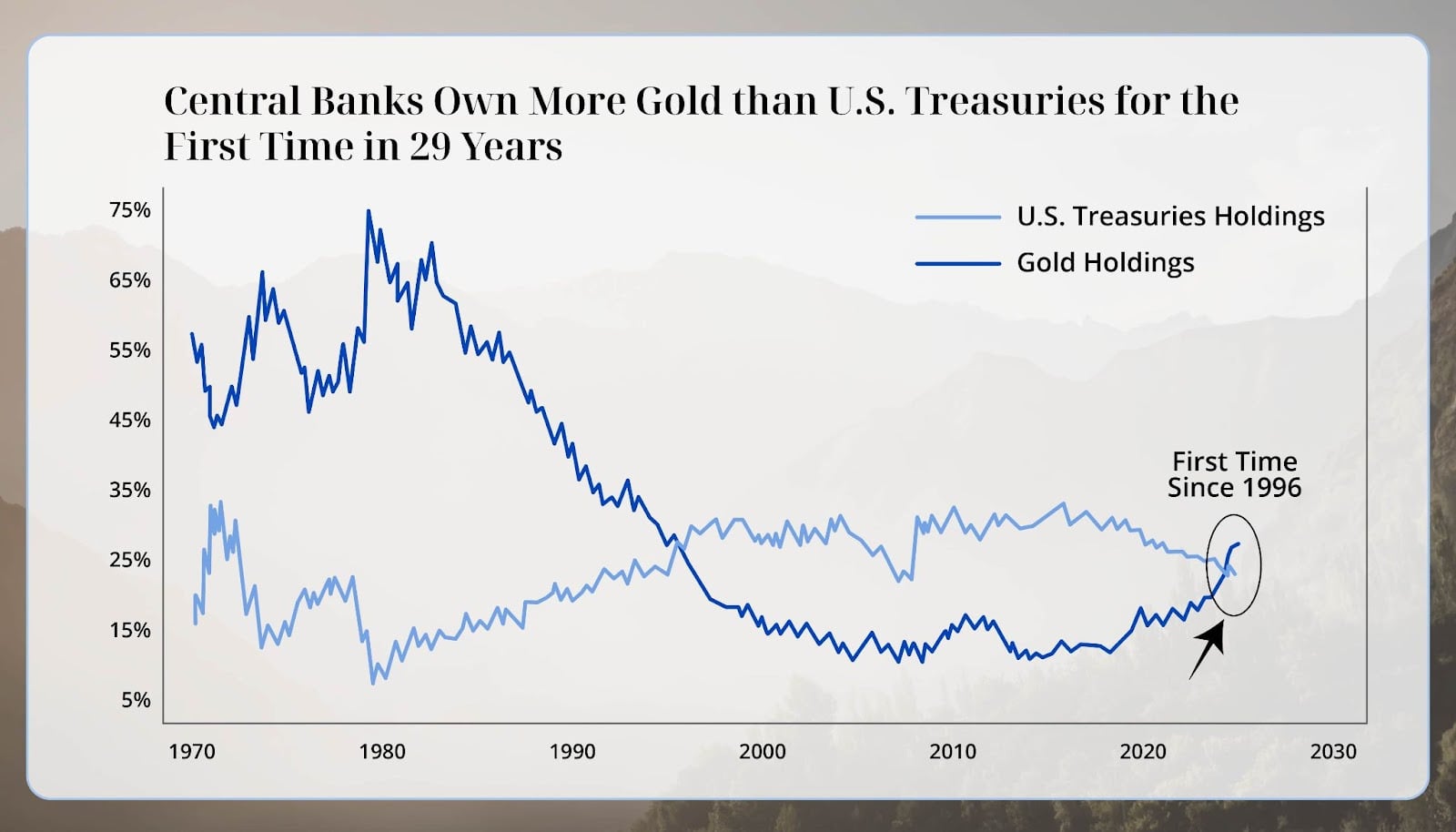

Gold is way under-owned by the average retail investor – even though central banks now hold more gold than US Treasuries for the first time in 30 years.

A big move is yet to come when retail investors finally show up. Not only that…

The dollar will eventually devalue much, much lower. It has to. All the problems that existed before the war are still present – and accelerating.

The direction of travel is still the same: The dollar is losing both value and dominance throughout the world – a trend that will continue for years to come.

As the dollar falls in value and purchasing power, it will make the gold price appear to rise.

Gold is the ultimate hedge against inflation and the policies now running the world.

That’s why you need gold. But I do not recommend buying bullion at today’s prices.

Because the best gold miners are now selling at fire-sale prices thanks to recent volatility from the war in Iran.

Go here to learn about my top four picks for the coming gold mania.

Regards,

Garrett Goggin CFA, CMT

Lead Analyst, Golden Portfolio

Crypto's Crash May Be Over—These 3 Picks Could Rebound Fast

Reported by Dan Schmidt. Article Published: 3/9/2026.

Key Points

- Crypto’s much-hyped 2025 rally fizzled, but recent stabilization is renewing interest in crypto-adjacent equities.

- ETF inflows, short-covering dynamics, and a shifting “digital gold” narrative are cited as near-term tailwinds.

- Coinbase, Bit Digital, and a Solana staking ETF offer different ways to gain broad crypto exposure through stocks and funds.

- Special Report: Have $500? Invest in Elon's AI Masterplan

2025 was supposed to be the Year of Crypto: we entered January with Bitcoin at all-time highs and a new, digital asset-friendly administration poised to take office in Washington. While crypto has picked up some regulatory wins over the last 12 months, the raucous rally never materialized.

Bitcoin's high-water mark of $126,000 for 2025 represented only about a 5% gain on the year, and a subsequent winter collapse erased more than half of that value in just a few months. Still, signs that the cryptocurrency decline has stabilized are opening opportunities for investors to buy crypto-adjacent stocks at bargain prices.

What’s Behind the Recent Cryptocurrency Surge

The new lie the U.S. government wants to sell you (Ad)

Decades ago, Washington sold the American public on ditching cash for credit cards to protect us from theft and stop criminals, but instead of stopping crime, it gave the government an unprecedented window into our daily lives—every flight, restaurant, and gallon of gas leaving a permanent data trail. Through a new initiative outlined in Federal Reserve Docket No. OP-1670, known as FedNow, the government is rolling out the ultimate financial tracking web that routes all those fragmented private transactions through a single centralized hub operated by the Federal Reserve itself, giving the federal government real-time 24/7 visibility into virtually every dollar moving through the U.S. economy with the power to flag or freeze your money with a single keystroke.

Get the 4 steps to Fed-proof your savings nowAsking "why" in crypto can be fruitless — sometimes prices move because they move. But after a roughly 50% haircut, many investors will want concrete reasons to re-enter. A few factors have emerged over the past weeks:

- Money Still Flowing Into Bitcoin ETFs - According to CoinDesk, more than $1.4 billion flowed into U.S. Bitcoin ETFs in the last week. Despite the steep decline and fresh geopolitical tensions, that indicates continued demand for cryptocurrency exposure. Institutional inflows often precede spot price moves, so sizable inflows are typically a bullish sign.

- Liquidation Cascades - Crypto markets are especially volatile in part because of the leverage and positioning involved. Many traders had large short positions on assets like Bitcoin, betting on further weakness. When Bitcoin finds a bottom and reverses, those shorts can be forced to cover in quick succession, creating a "liquidation cascade." CoinPedia reports roughly $110 million in short positions were wiped out last week when Bitcoin jumped from $60,000 to $70,000. With sentiment still fragile, additional short squeezes are possible if Bitcoin can hold support near $68,000.

- Digital-Gold Narrative Returns - For much of 2025, Bitcoin and other large tokens tracked risk-on assets, moving in line with the tech sector. That correlation weakened after the outbreak of war in Iran, with cryptocurrencies rallying alongside gold and the U.S. dollar while equities struggled.

3 Stocks to Buy for Broad Cryptocurrency Exposure

You no longer need a wallet or a seed phrase to add crypto exposure to a portfolio. You can buy stocks that move with crypto markets or companies that hold digital assets directly. Below are three names that offer diverse exposure across multiple tokens and strategies.

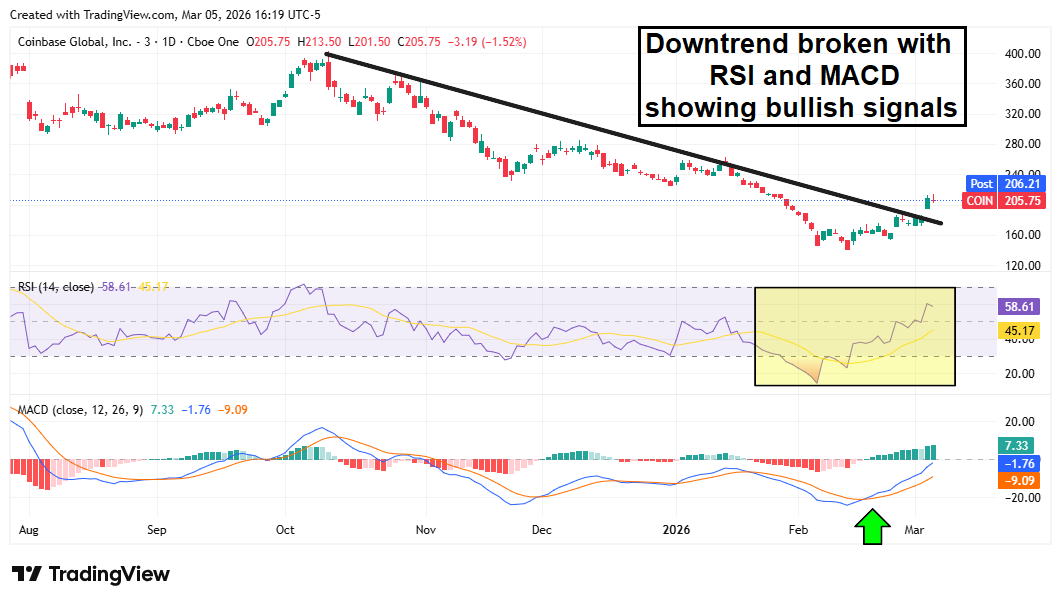

Coinbase Global: Rally Could Trigger a Quick Re-rating

Coinbase Global Inc. (NASDAQ: COIN) has been hit hard since Bitcoin's slide began — not just from investor outflows but from analyst downgrades and lower price targets. Zacks Research moved the stock from Neutral to Strong Sell after Coinbase missed on both top- and bottom-line numbers in Q4 2025. That said, sentiment in crypto can change rapidly, and analysts risk being caught offside if momentum returns.

Goldman Sachs lifted its price target to $270 on March 6, citing improving technicals. COIN shares have broken the downtrend that began last October, and bullish signals from the Moving Average Convergence Divergence (MACD) indicator add weight to the case for a re-rating.

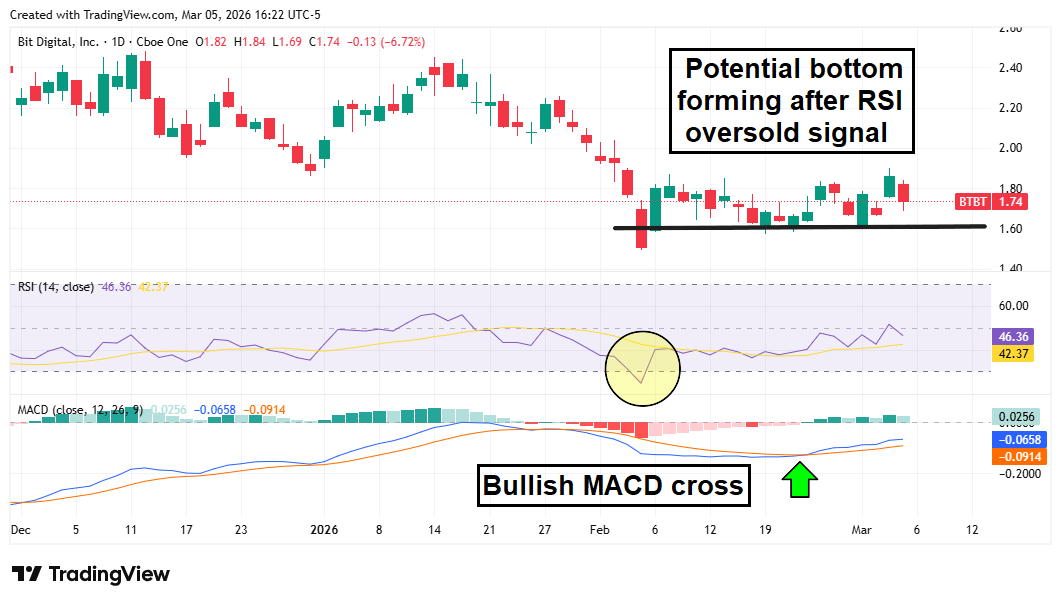

Bit Digital: An Ethereum Treasury With Meaningful Holdings

If you want exposure to the Ethereum ecosystem, consider an Ethereum-treasury company like Bit Digital Inc. (NASDAQ: BTBT), which shifted from Bitcoin mining toward ETH staking. The company reported holding more than 155,000 ETH as of February — reportedly more than Coinbase — and nearly 90% of those holdings are staked to generate yield. Bit Digital also publishes a monthly staking report that details its positions, offering greater transparency than many peers.

BTBT shares consolidated after the February selloff as the RSI reached oversold levels. The oscillator is now trending upward, and a bullish MACD crossover suggests potential for further gains.

Bitwise Solana Staking ETF: Yield Plus SOL Upside

Recently, Solana — not Bitcoin or Ethereum — has been the top performer among major cryptocurrencies. SOL surged in early 2025 after the introduction of the TRUMP token, then fell out of favor, and is now leading the recovery. A straightforward way to gain exposure is the Bitwise Solana Staking ETF (NYSEARCA: BSOL).

BSOL holds SOL tokens and stakes them to earn rewards. The fund targets roughly 6%–8% in annual staking returns, in addition to any price appreciation in SOL. Like BTBT, the ETF appears to be finding a bottom, with bullish momentum emerging on both MACD and RSI indicators.

Wendy's Is Down Sharply—Is the Dividend a Bargain or Value Trap?

Reported by Chris Markoch. Article Published: 3/1/2026.

Key Points

- Wendy’s shares remain under heavy pressure despite a Q4 earnings beat, driven by the company’s worst same-store sales performance in two decades.

- Management is pursuing store closures, menu value initiatives, and the “Project Fresh” overhaul as it navigates a strained lower-income consumer.

- A 7%+ dividend yield may attract income investors, but weak growth guidance and declining free cash flow raise concerns about a value trap.

- Special Report: Have $500? Invest in Elon's AI Masterplan

The Wendy’s Co. (NASDAQ: WEN) delivered a double beat when it reported Q4 2025 earnings on Feb. 13. Still, shareholders lost their appetite for WEN stock, pushing it to a 52-week low of $6.73. Recent headlines have supported a rally, but the stock remains down nearly 51% over the past 12 months and more than 61% over the last five years.

Big numbers worked against the company: Wendy’s posted its worst same-store sales performance in 20 years, a result shareholders could hardly overlook.

The new lie the U.S. government wants to sell you (Ad)

Decades ago, Washington sold the American public on ditching cash for credit cards to protect us from theft and stop criminals, but instead of stopping crime, it gave the government an unprecedented window into our daily lives—every flight, restaurant, and gallon of gas leaving a permanent data trail. Through a new initiative outlined in Federal Reserve Docket No. OP-1670, known as FedNow, the government is rolling out the ultimate financial tracking web that routes all those fragmented private transactions through a single centralized hub operated by the Federal Reserve itself, giving the federal government real-time 24/7 visibility into virtually every dollar moving through the U.S. economy with the power to flag or freeze your money with a single keystroke.

Get the 4 steps to Fed-proof your savings nowHas the stock become so bad it’s good? As with many retail names, value can depend on the observer. One investor who seems optimistic is hedge fund billionaire Nelson Peltz. Peltz has been a major shareholder for more than two decades and has been evaluating ways to enhance shareholder value. An SEC filing suggested one option could be a takeover of the chain.

That said, Wendy’s is already undergoing a transformation (Project Fresh) and plans to close roughly 5%–6% of its locations in 2026. The company has also made moves to make its value menu (i.e., the Biggie Bag) more competitive.

It’s unclear what additional value Peltz might try to unlock. One potential objective could be securing a permanent chief executive officer — the company is currently led by interim CEO Ken Cook. Still, it’s best to evaluate the stock on its current fundamentals.

Turnaround Efforts Face Macro and Consumer Headwinds

Wendy’s beat expectations on both the top and bottom lines, and that was genuinely better-than-expected rather than merely better-than-feared. Even so, the steep same-store sales decline is difficult to ignore.

Interpretation is the challenge. Investor views on the economy vary widely, and outcomes depend on which leg of the so-called “K-shaped” recovery you consider. Lower-income consumers appear particularly pressured; if the debate centers on which $5 value meal offers the most “value,” the constraint may be consumer spending rather than company execution.

Add concerns about GLP-1 weight-loss drugs affecting dining behavior, and it’s reasonable to conclude Wendy’s may be doing as well as possible in a difficult environment. In 2021, WEN traded near $20 — but conditions have changed since then.

Wendy’s is forecasting relatively flat global sales growth, with adjusted earnings per share (EPS) expected in a range of $0.56 to $0.60. That represents about a 32% decline if the company hits the high end of the forecast.

The company is trimming capital expenditures by roughly $10 million to $20 million and expects free cash flow (FCF) to decrease to $190 million from $205 million.

Those projections carry a “more of the same” bias, which is not necessarily a bad approach: 2026 could produce a range of outcomes for the lower leg of the K-shaped recovery.

A Tasty Dividend or Value Trap?

One bright spot for WEN is its dividend.

The payout was cut nearly in half in 2025 but remains at $0.56 per share. With the stock around $7.70 at the time of writing, that implies a yield of about 7.26%.

Whenever a company posts disappointing results and still offers an attractive yield, questions about sustainability arise — especially given the drop in FCF. But the dividend currently costs Wendy’s roughly $106 million annually, a level that appears sustainable even with the projected FCF decline.

Investors would be more comfortable with a payout ratio under 50% (it’s currently about 65.88%), but given the company’s conservative projections there is little evidence the dividend is unsafe today.

Technical Picture Suggests Rally May Be Temporary

Technically, WEN has been in a steady downtrend since March 2025, falling from roughly $16 to current levels near $7.73 and tracking along the lower Bollinger Band for months. Price now sits at the 20-day simple moving average (SMA), about $7.82, which has acted as resistance rather than support throughout the decline.

After the sharp February sell-off and brief bounce, the stock has mean-reverted to the middle Bollinger Band, suggesting the oversold condition was relieved and the bounce was more corrective than a genuine trend reversal.

The moving average convergence/divergence (MACD) supports that view. The MACD line briefly crossed above zero during the bounce but is rolling back over while the signal line remains deeply negative (-0.1239). Resistance near the upper Bollinger Band (around $8.41) remains a significant hurdle; without convincingly reclaiming that level, the path of least resistance still points lower.

to bring you the latest market-moving news.

This message is a sponsored email provided by Golden Portfolio, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

Copyright 2006-2026 MarketBeat Media, LLC dba TickerReport. All rights protected.

345 N Reid Pl. #620, Sioux Falls, South Dakota 57103-7078. U.S.A..

0 Response to "Why isn’t gold rising on war news?"

Post a Comment