You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. A Warning from the Future...I'm pretty sure this is the most obvious crisis in the history of the United States

Dear Fellow Traveler: After a few days and constant revisions (because I’m always paranoid about things that I write at length, I released the Hedge of Tomorrow 2.0 yesterday. This lengthy report covers all the bases of liquidity, momentum, insider activity, public policy, and the assets to purchase as we transition from tight credit conditions to loosening conditions when something does… finally break. At the center of the report, I provided a recap of one of the most obvious crises looming on the horizon for the United States. As I’ve concluded, the current private credit crisis isn’t so much a liquidity event as a preview of a brewing retirement crisis over the next six years. Today, I want to provide an excerpt of the Hedge of Tomorrow 2.0. If you want immediate access, consider joining Money Printer Pro or Postcards from the Edge of the World. An Exerpt from Hedge of Tomorrow “The Retirement Trap”We anticipate a real economic crisis over the next decade, but not in the traditional sense of what we witnessed in 2008 or 2020. While the timing is uncertain, the directional pressure is clear in today’s data. It doesn’t necessarily center around broad-scale equity pricing or the global financial system. Consider that we face a persistent retirement crisis over the next decade. This potential crisis could justify a multi-trillion-dollar balance-sheet expansion. It could be sold to the public to save our parents’ pensions. This isn’t complicated, and you don’t need to squint. Private credit assets have grown between $1.8 trillion and $3 trillion over the last decade. Recent redemption requests have highlighted sector exposure to illiquid lending structures that rely on stable funding conditions. Certain collateralized loan obligations (CLO) equity tranches have seen drawdowns ranging from 30% to 60%. Current default rates are expected to rise from historically low levels. Estimates from groups like Oxford Economics suggest a meaningful share of private credit portfolios face AI-disruption risk. The risk is not default. It’s a redemption meeting illiquid marks and declining portfolio values. Federal Reserve Chairman Jerome Powell has said private credit is contained. But we must take a step back to examine how private credit fits into a broader economic problem. Private credit losses flow directly into the balance sheets of companies holding annuities, life insurance, and pensions. While this doesn’t look like 2008, it can easily produce something problematic. In a note at the end of Q1 2025, Javier Corominas, director of global macro strategy at Oxford Economics, suggested the impact of private credit on retirement. He wrote:

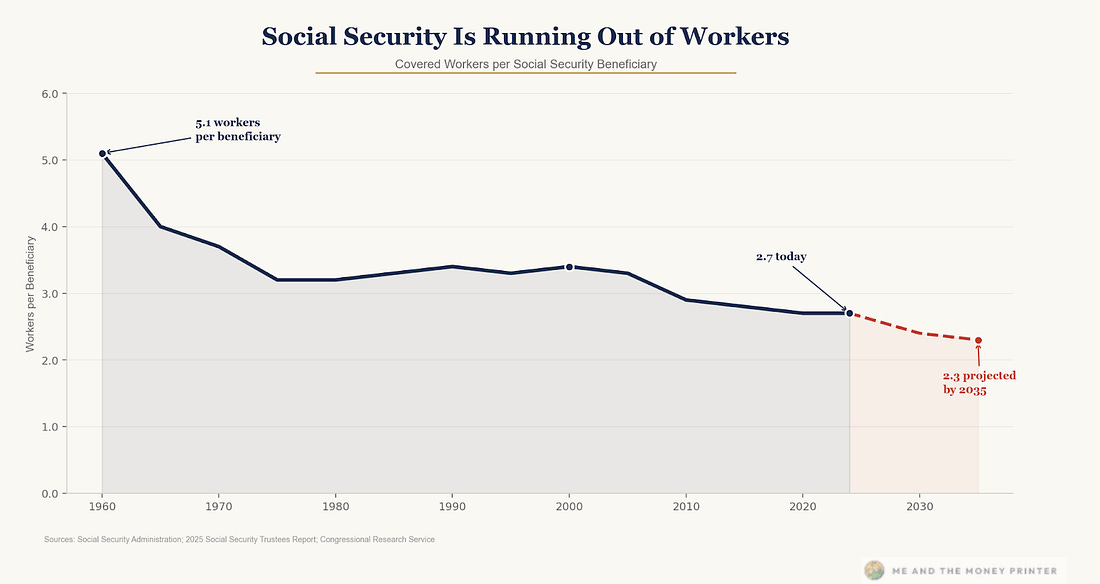

This would, over time, start to affect not just retail investors holding annuities but also broader pension systems already under strain and facing deficits. Municipal pension holes in cities like Chicago and Los Angeles are already straining budgets, and higher taxes to fill existing gaps have fueled voter flight. Combine existing pension holes with duration risk from private credit, and the crisis is obvious. Again, this is just one part of a story that is part of a deeper puzzle. Consider that Social Security is slowly cracking from the other side. The worker-to-beneficiary ratio, once around 5-to-1, is projected to fall to roughly 2.3-to-1 over the next decade, according to the Social Security system’s own studies.

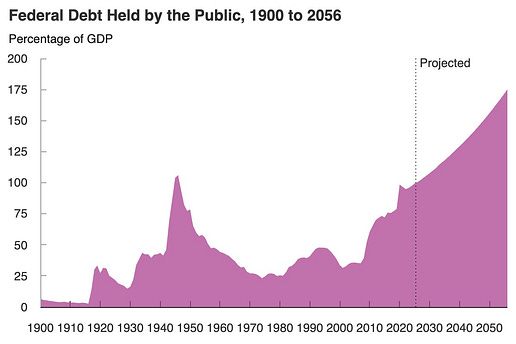

Source: Me and the Money Printer, Social Security Administration Many workers are pessimistic about the future of Social Security, and claiming behavior is beginning to cluster aggressively around the earliest eligibility age of 62, accelerating the very depletion they fear. A recent survey and study by Northwestern Mutual suggests that 27% of Gen X workers and 39% of Boomers will take early benefits despite the 30% haircut on what can be obtained at the official retirement age (67 if born in or after 1960). The top reason for this behavior is concern about the sustainability and expected payouts of the largest retirement payment program in most Americans’ lives. At the same time, AI may accelerate these pressures at the margin by compressing entry-level income growth and shrinking the pipeline of workers paying payroll taxes. Recent data has shown large monthly swings in labor force participation, with hundreds of thousands exiting in a single month. Multiple legs of retirement funding are facing pressure. Savings can erode due to private credit losses. In contrast, income can erode as Social Security is depleted, and tens of millions of Americans discover that both of their retirement backstops are eroding. Congress likely won’t be able to cut benefits because it would be political suicide. While Congress could raise taxes enough to cover the gap, those transfer payments would come from younger constituencies already affected by decades of policy mismanagement. They would act as a further tax on incomes at a time when most people struggle with the cost of living. So, we expect the system to do only what it knows how to do. The system would likely expand the monetary base for now because every alternative is politically or economically worse. This process isn’t linear. Market cycles can go longer than fundamentals justify. Meanwhile, policy responses can delay outcomes without resolving them. Based on prior crises, we imagine that the Treasury could issue new debt, the Fed would buy it, and they would call the effort something new, like the “Retirement Security Facility.” The mechanism is the same as Quantitative Easing, which aims to stabilize the system and achieve outcomes similar to those of similar policies. That said, we could eventually witness the largest balance-sheet expansion in history because the political constituency for retirement security is the most powerful force in democratic politics. Simply put: They vote. I had previously expected the U.S. to use another emergency, such as “climate change,” to expand the Fed’s balance sheet or issue short-term Treasuries in large quantities. Further monetization is expected, and the Congressional Budget Office (CBO) forecasts rising debt. Deficits are expected to run at an annual rate of 5.6% to 6.7% per year from 2027 through 2036.

Source: Congressional Budget Office This crisis is obvious… and one that could dominate Federal Elections in 2028 and 2032, as older voters ask what is so common today: “What are you going to do for me?” In addition, Social Security doesn’t have a pile of money in a vault. It has Treasury bonds, which are IOUs the government wrote to itself. As withdrawals exceed contributions, the system redeems those bonds, meaning the Treasury has to issue new debt to pay retirees. That means every Social Security check is now, functionally, financed by the same strained debt market, repo plumbing, and leveraged hedge-fund basis trades that dominate the financial plumbing of our markets. Should tensions expand, a likely response is some form of monetization and fiscal repression. The Fed’s purchases flood the system with liquidity, asset prices recover on paper, but the entry ticket to the American middle class gets more expensive at exactly the moment when AI is compressing the wages of the generation trying to buy it. The 25-year-old who can’t find an entry-level job because AI has eliminated those roles is now even further from affording a house. The balance sheet expansion required to save their parents’ pensions would only further inflate every asset class above them. Now, this is a scenario, and not a certain outcome. However, these types of situations are debated at the Federal level and are starting to happen in various financial planning discussions across the nation. That is why the Hedge is necessary. And why we believe the obvious defense against future monetary expansion and debt growth is to own “economic chokepoints.” When the Fed is forced to expand the balance sheet again, scarce assets reprice the fastest, and those that sit at bottlenecks collect a toll on every dollar that flows through. Many elements of this scenario are already visible in the data. The question is less whether it unfolds than how. This is a lot to unpack… But I want to talk about how the system really works and why it’s more important than ever to have a plan for its mechanisms… Lyn Alden appeared on Peter McCormack’s podcast last week, and I finally had a chance to watch it last night. I think that if you’ve read Postcards on my extraction arguments and Me and the Money Printer on the mechanics of this system, you’ll find a lot of familiar territory. Lyn just happens to explain the mechanics better than I ever could in a one-hour, must-watch conversation that really breaks down why we feel so behind…

What is critical is that the “Nothing Stops This Train” argument supports the ongoing shifts in mechanics and the private-sector bailouts to public-sector ledgers, and explains how the Cantillon Effect works. In essence, it’s not necessarily evil… but the system is working exactly as it’s designed. And that’s an incredibly important point… Understanding that design and the flows of capital that ensure the plumbing gets unstuck are our “what to do” approach in Hedge of Tomorrow. Enjoy… Stay positive, Garrett Baldwin PS: About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "A Warning from the Future..."

Post a Comment